The concept of retirement accounts is pivotal in contemporary financial planning. Traditionally, retirement accounts provide an avenue for individuals to set aside funds, often with tax advantages, to support themselves during their golden years. IRAs, or Individual Retirement Accounts, are at the forefront of such financial tools. They've evolved over the years, offering varied structures and benefits to cater to diverse financial needs. Yet, while the primary objective remains constant - ensuring a secure retirement - the means to achieve it have broadened significantly. This broadening has given birth to multiple IRA variants, each with its unique features. While a rollover IRA shelters funds from previous employer plans, a self-directed IRA broadens investment options. Transitioning offers advanced investment strategies but demands an understanding of benefits and complexities. A rollover IRA serves as a reservoir. Typically, when an individual changes jobs, they roll over their previous 401(k) or other employer-sponsored plan into this IRA to keep the tax-deferred status. In essence, it's a continuation of one's retirement journey without the hiccup of cashing out prematurely. In contrast, a self-directed IRA is a type of account that grants the holder more control over investment choices. It goes beyond the usual stocks, bonds, or mutual funds. Think real estate, private companies, or even precious metals. The purpose here is to leverage knowledge in specific sectors and potentially garner greater returns. Rollover IRAs tend to align with conventional investment channels. We're talking about mainstream vehicles: stocks, bonds, CDs, and mutual funds. It's comfortable, and it's familiar. Self-directed IRAs, however, are like wild, uncharted territories. They give investors access to alternative investments. From real estate to tax lien certificates, from cryptocurrency to private business dealings, the range is vast and diverse. The very essence of a rollover IRA is continuity, making it somewhat passive. Once funds are rolled over, they often stay invested in typical market instruments. But for those with an appetite for hands-on management and unique opportunities, self-directed IRAs offer unparalleled flexibility. Investors call the shots, making decisions tailored to their expertise, research, or gut feelings. Every financial endeavor comes with its cost. Rollover IRAs often have straightforward fees, mostly tied to the investment platforms they're on. Think of annual account maintenance fees or investment-specific expenses. Self-directed IRAs, given their expansive nature, can have a more intricate fee structure. Custodian fees, transaction fees, and perhaps even charges specific to alternative investments, like property management fees for real estate, come into play. Both IRA types require custodians, but their roles can differ. For rollover IRAs, custodians primarily serve as administrative overseers. They ensure that tax regulations are met and paperwork is in order. In the realm of self-directed IRAs, custodians wear multiple hats. They still handle administrative tasks but also facilitate access to unconventional investments. It's a partnership where expertise from both the investor and the custodian ensures a well-oiled investment machine. Sometimes change propels growth. Rolling over an IRA, particularly from a conventional to a self-directed type, can stem from several reasons. Perhaps it's the lure of potentially higher returns from alternative investments. Or maybe it's dissatisfaction with current investment choices or simply a desire for a more hands-on investment approach. For others, it might be about consolidating multiple retirement accounts into one place, streamlining finances, and simplifying management. Rolling over brings its bouquet of advantages. Increased control, diversified investment options, and potential tax benefits rank high on the list. For those well-versed in certain sectors, a self-directed IRA can unlock significant growth. However, the path isn't strewn with roses alone. The risks of alternative investments are real. Additionally, the responsibility of due diligence rests heavily on the investor. And while self-direction brings freedom, it also demands time, effort, and sometimes, a higher tolerance for volatility. Timing is often the linchpin of successful financial decisions. Rolling over to a self-directed IRA makes perfect sense for those keen on diversifying beyond traditional markets, especially if they possess expertise in alternative sectors. Moreover, if an investor finds themselves constrained by their current IRA's limited choices, seeking the expansive horizon of a self-directed IRA can be wise. On the other hand, those comfortable with their current returns, or those who prefer a more hands-off approach, might find little appeal in the transition. A custodian's role is paramount in the world of self-directed IRAs. The ideal custodian offers a blend of comprehensive services, transparent fee structures, and robust support. They act as facilitators, ensuring smooth transactions and adherence to regulations. When choosing, it's wise to consider their expertise in desired investment sectors, their reputation, and perhaps even their technological infrastructure for ease of management. The actual process of rolling over starts with notifying the current custodian about the intent to move funds. Next, an account with the chosen self-directed IRA custodian gets opened. It's essential to specify that the funds are a "rollover" to ensure they retain their tax-advantaged status. While the process might seem linear, it's crucial to be meticulous with paperwork and timelines to avoid potential tax pitfalls. Transferring funds should ideally be a direct custodian-to-custodian affair. This ensures the money doesn't touch the hands of the investor, thereby safeguarding its tax-deferred status. If dealing with assets, their valuation becomes crucial. The transferred value should reflect the asset's fair market value. Given the delicate nature of this step, many investors prefer involving financial professionals to navigate smoothly. The IRS has its watchful eyes on all IRA transactions, and for a good reason. These accounts come with tax advantages, and the government wants to ensure no foul play. It's essential to stay updated with any contribution limits, prohibited transactions, and the nuances of distributions. Being non-compliant isn't just about facing penalties. It can jeopardize the tax-advantaged status of the entire IRA, which can be a costly affair. A direct rollover, where funds move from one custodian to another without the investor touching them, usually remains tax-free. The key here is to ensure it's labeled correctly and the process is swift. The IRS allows one indirect rollover (where funds temporarily come to the investor) per year, but it must be completed within 60 days to avoid taxes. Such provisions ensure individuals don't misuse the tax benefits while still offering a bit of flexibility. Sometimes, the maze of IRA regulations can lead investors to unintended tax consequences. For instance, engaging in prohibited transactions or violating the one-rollover-per-year rule can result in taxes and penalties. Moreover, if assets within a self-directed IRA generate income, like rental income from a property, Unrelated Business Income Tax might apply. The best shield against such pitfalls is knowledge. Regularly reviewing IRS guidelines and perhaps consulting with tax professionals can be invaluable. RMDs are the minimum amounts IRA holders must withdraw annually once they reach a certain age. The exact amount is calculated based on the account's end-of-year balance and life expectancy. Rolling over to a self-directed IRA doesn't exempt one from RMDs. However, calculating RMDs for alternative investments, like real estate or private equity, can be complex. Here, periodic asset valuation becomes crucial to ensure compliance and avoid penalties. Every investor has a unique strategy sculpted by their goals, risk tolerance, and market perceptions. Transitioning to a self-directed IRA should be a conscious alignment with this strategy. It's about asking the hard questions. Does this move support my long-term objectives? Am I equipped to delve into alternative investments? It's less about the allure of potential returns and more about the congruence with one's financial journey. Liquidity denotes how quickly assets can be converted to cash. Some investments in a self-directed IRA, like real estate, can be relatively illiquid. Thus, if there's a foreseeable need for quick funds in the near future, diving deep into such investments might not be prudent. Furthermore, the investment horizon matters. Those closer to retirement might opt for a different asset mix compared to younger investors, balancing growth prospects with liquidity needs. With great power comes great responsibility. The vast investment landscape of self-directed IRAs also hosts varied risks. Some sectors, like real estate, might face market downturns, while others, like certain startups, might carry inherent business risks. Understanding these, assessing their likelihood, and having contingency plans become pivotal. It's not about avoiding risks but navigating them with eyes wide open. Self-directed IRAs aren't for the faint-hearted. They demand a level of financial savvy, especially when delving into alternative sectors. While everyone starts somewhere, a basic foundation in investment principles can be a strong asset. Experience, too, plays its part. Those who've dabbled in real estate or have run businesses might find certain investment channels more intuitive and promising. A static portfolio can be a stagnant one. Regular reviews ensure that investments align with changing financial goals, market scenarios, and risk appetite. Whether it's rebalancing asset allocation, liquidating underperformers, or doubling down on winners, periodic adjustments keep the portfolio vibrant and aligned with objectives. It's akin to pruning a garden. While the plants (investments) do their thing, timely interventions ensure optimal growth. The IRS isn't ambiguous here. Certain transactions are off-limits within a self-directed IRA. For instance, buying a vacation home for personal use using IRA funds is a no-go. Similarly, lending IRA funds to a family member or dealing with disqualified persons can trigger penalties. Awareness is the first line of defense. Knowing what's prohibited ensures the integrity of the IRA's tax-advantaged status. Reiterating the importance of expert advice, every investment decision can benefit from a second pair of eyes. Especially in the realm of alternative investments, nuances can be many. Whether it's the legal implications of a private equity deal or the market trajectory of a particular commodity, expert opinions can offer clarity. Seeking advice isn't an admission of ignorance; it's a testament to the investor's commitment to informed decisions. Rollover IRAs and self-directed IRAs are pivotal tools in modern financial planning, offering unique ways to prepare for retirement. The former acts as a continuation of one's retirement journey, ensuring tax-deferred benefits from previous employment plans, while the latter provides an expansive investment landscape, granting investors autonomy in diversifying their portfolios. Transitioning between the two entails not just the allure of broader investment choices but demands comprehension of the complexities involved, including potential tax implications and adherence to IRS regulations. Key considerations before making such a transition include aligning the move with one's long-term financial goals, understanding liquidity needs, and assessing inherent risks in investment options. Furthermore, leveraging expertise, staying updated on IRS guidelines, and regular portfolio reviews are paramount in managing self-directed IRA investments effectively. Overall, while both IRAs have their merits, transitioning should be a well-thought-out decision tailored to individual financial situations and goals.Overview of Retirement Accounts

Key Differences Between a Rollover IRA and a Self-Directed IRA

Definition and Purpose

Range of Investment Options

Flexibility and Control Over Investments

Costs and Fee Structures

Role and Necessity of Custodians

Understanding the Rollover From IRA to Self-Directed IRA

Reasons for Rolling Over an IRA

Potential Benefits and Drawbacks of a Rollover

When a Rollover Makes Sense

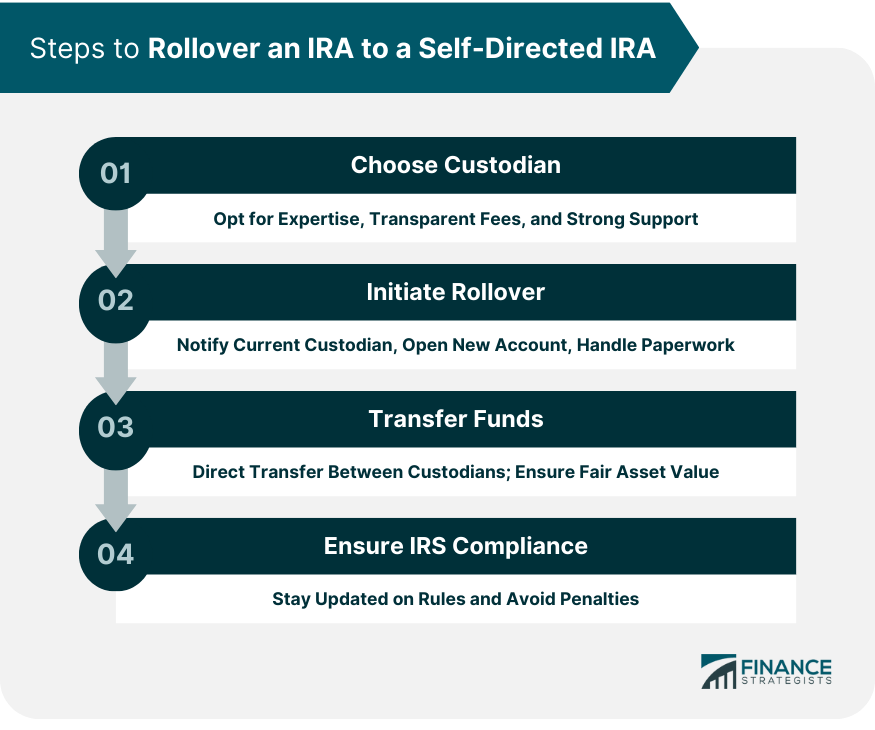

Steps to Rollover an IRA to a Self-Directed IRA

Choose the Right Self-Directed IRA Custodian

Initiate the Rollover Process

Transfer Funds and Assets

Ensure Compliance With IRS Rules and Regulations

Potential Tax Implications of IRA to Self-Directed IRA

Tax-Free Rollovers: How and When

Unintended Tax Consequences and How to Avoid Them

Impact on Required Minimum Distributions (RMDs)

Factors to Consider Before Making the Rollover From an IRA to a Self-Directed IRA

Evaluate Your Investment Strategy

Consider Liquidity Needs and Time Horizon

Understand Potential Risks

Review Level of Financial Acumen and Experience

Managing Your Self-Directed IRA Investments

Regularly Reviewing and Adjusting Your Portfolio

Understanding Prohibited Transactions

Seeking Expertise in Investment Decisions

Bottom Line

Rollover IRA to Self-Directed IRA FAQs

A Rollover IRA serves to continue the tax-deferred status of funds from previous employer plans, while a Self-Directed IRA offers broader, alternative investment choices.

It offers increased control, a wider range of investment options, potential tax benefits, and the opportunity to diversify beyond traditional markets.

Yes, direct rollovers are typically tax-free, but mistakes or non-compliance can lead to unintended tax consequences. Always ensure you follow IRS guidelines.

Rollover IRAs focus on conventional investments like stocks and bonds, while Self-Directed IRAs encompass alternative assets such as real estate or private equity.

Yes, given their expansive investment choices, Self-Directed IRAs demand a more hands-on approach and a deeper understanding of diverse sectors.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.