An Individual Retirement Account (IRA) rollover refers to the process of moving funds from a retirement account into a traditional IRA or another type of retirement account. This action is typically undertaken to consolidate funds, achieve better investment options, or as a result of life changes like job transition. Rollovers are essential tools in retirement planning, allowing individuals to maintain the tax-advantaged status of their retirement savings. These transfers, when executed properly, can be both tax-free and penalty-free, ensuring that retirement savings continue to grow unhindered. An IRA rollover consolidates multiple retirement accounts from past jobs, offering clearer management, reduced fees, and diverse investment options. This flexibility is essential during major life or financial shifts. When executing an IRA rollover, funds are essentially transferred from one retirement account to another. This transfer can be from a 401(k), 403(b), or another similar plan, into an IRA. It's crucial to ensure this transfer is done in compliance with IRS rules to avoid unintended tax consequences. Different types of rollovers have varying procedures and requirements. These distinctions exist to help individuals navigate the intricate world of retirement savings, but also emphasize the importance of understanding the specifics of each type of transfer. In a direct rollover, funds move directly from one retirement account to another without the account holder ever touching the money. This method is the most straightforward and least prone to errors or tax penalties. The funds retain their tax-advantaged status, and the transaction is typically seamless. The 60-day rollover option allows an individual to receive funds from a retirement account and then redeposit them into another retirement account within 60 days. While this provides more control, it also introduces the risk of missing the 60-day window, leading to potential tax consequences. This type of transfer occurs when the funds are moved between two IRAs held at the same financial institution. It's the simplest of rollovers and is almost administrative in nature. There's no need to worry about the 60-day rule, making it an easy and efficient choice for many. Before initiating a rollover, it's essential to determine if you're eligible. Not all retirement accounts qualify for rollovers, and sometimes there are stipulations depending on employment status or the type of account. Researching and understanding these prerequisites can save potential headaches later on. Eligibility often hinges on factors like the type of retirement plan, your age, and the reason for the rollover. For instance, certain plans may only allow rollovers upon reaching a specific age or after leaving an employer. Choosing the right account type is crucial. Traditional and Roth IRAs have different tax implications and benefits. While a traditional IRA offers tax-deferred growth, a Roth IRA provides tax-free withdrawals in retirement. Depending on your financial situation, age, and retirement goals, one might be more beneficial than the other. It's not just about taxes; factors like withdrawal rules, required minimum distributions, and contribution limits can influence this decision. Analyzing both current needs and future financial scenarios can help in making an informed choice. If you don't already have the desired IRA, the next step is to open one. Financial institutions offer an array of IRA options, each with its set of features, fees, and investment choices. While some prioritize low fees, others might offer exclusive investment options or added services. Opening an account involves filling out paperwork, providing identification, and understanding the terms of the account. It's essential to review all details, especially concerning fees, withdrawal rules, and investment options. Once you're set with your new (or existing) IRA, it's time to initiate the rollover with your current retirement account's custodian. This process might require filling out forms and specifying how you want the transfer to occur (e.g., direct rollover or 60-day rollover). Typically, the distributing custodian will offer guidance on their required steps. However, being proactive and ensuring that all forms are correctly filled out can expedite the process and prevent potential delays. After initiating the rollover, the funds will move from the old account to the new one. The time this takes can vary based on the institutions involved and the type of rollover. Direct rollovers tend to be quicker and more straightforward than 60-day rollovers. During this time, it's wise to monitor the progress, ensuring that funds leave the distributing account and reach the receiving account without hitches. If any discrepancies arise, addressing them promptly is vital. Upon reaching the new account, the funds might be placed in a default investment option or a cash equivalent, awaiting your investment instructions. Based on your risk tolerance, financial goals, and market outlook, you'll need to allocate these funds appropriately. Whether you replicate your previous investments or craft a new strategy, ensure your choices align with your long-term retirement objectives. If in doubt, seeking the counsel of a financial advisor might be beneficial. Rollovers, while typically non-taxable events, still need reporting on tax returns. This step is crucial to ensure the IRS knows that the funds weren't a taxable distribution. Properly reporting prevents unnecessary queries or penalties later on. When tax season rolls around, both the distributing and receiving accounts will send out tax forms detailing the rollover. These documents will guide you (or your tax professional) in accurately recording the transaction on your return. The 60-day window in a 60-day rollover is stringent. If you overshoot this period, the funds are treated as a distribution, not a rollover. This misstep can result in taxes and potential penalties, especially if you're younger than 59.5 years old. To avoid this, be diligent about marking deadlines, setting reminders, or even opting for direct rollovers which aren't bound by this rule. Retirement accounts can house both pre-tax and post-tax contributions. Mixing them without comprehension can complicate your tax situation. For example, moving pre-tax 401(k) funds into a post-tax Roth IRA triggers a taxable event. The key is always to keep pre-tax and post-tax monies separate. When in doubt about the nature of your contributions, consult with a tax professional or delve deeper into account statements. Financial transactions often come with fees. From maintenance and trading fees to potential early withdrawal penalties, one needs to be cognizant of any charges linked with the rollover. Sometimes, these costs can dent the benefits of a rollover. Thus, having a clear understanding of all associated fees, both in the relinquishing and the receiving account, ensures you're making a financially sound decision. The primary advantage of a rollover is the continuation of tax-advantaged growth. Funds in retirement accounts grow free from yearly taxes, only getting taxed upon withdrawal (or not at all in Roth accounts). Transferring them through a rollover ensures this boon remains uninterrupted. This tax treatment can significantly bolster the growth of retirement savings over time. Without the yearly drag of taxes, compounded growth can work its magic, leading to a more substantial nest egg. As life progresses, individuals might accumulate numerous retirement accounts from different employers. Each of these accounts could have its fee structures, investment options, and rules. Consolidating them via rollovers can simplify financial management, creating a clearer retirement picture. Not only does consolidation reduce the headache of tracking multiple accounts, but it can also reduce fees, as managing one account is often cheaper than maintaining several smaller ones. Employer-sponsored plans often limit investment options, restricting account holders to a selected list of funds. Rolling over to an IRA typically opens the door to a broader universe of investment opportunities, including individual stocks, bonds, and niche funds. This flexibility can be vital for those looking to diversify their portfolios or tap into specific market opportunities. Whether seeking to hedge risks, target particular sectors, or achieve other specific investment objectives, an IRA often offers more avenues to do so. In some scenarios, rolling over can help individuals avoid early withdrawal penalties. For instance, leaving a job between age 55 and 59.5 can allow for penalty-free withdrawals from a 401(k) but not from an IRA. In such situations, rolling over may not be the best option. Understanding the nuances of early withdrawal rules, both in the distributing and receiving accounts, can help in making informed choices, ensuring maximum financial benefit. While the 60-day rollover provides control, it also brings risks. Missing this deadline is more than a minor inconvenience; it can trigger a taxable event and potential penalties. For those under 59.5, this could mean both income taxes and a 10% penalty on the amount. Understanding the gravity of this rule and the implications of missing the deadline can guide individuals in either adhering strictly or opting for the safer direct rollover. When funds are distributed from a retirement plan for a rollover, the plan might withhold 20% for federal taxes. If you're executing a 60-day rollover, you'd need to replace this withheld amount out of pocket to rollover the full balance and avoid taxes. This withholding can catch individuals off-guard, creating unforeseen financial strain. Opting for direct rollovers, where there's typically no withholding, can avert this issue. The IRS limits the number of 60-day rollovers one can execute in a 12-month period. Exceeding this limit can result in extra distributions becoming taxable and potentially penalized. This rule underscores the importance of strategic planning when considering multiple rollovers. Direct rollovers and same trustee transfers, fortunately, aren't bound by this rule. Hence, they can be more convenient for those looking to execute several transactions within a year. One of the most common triggers for considering a rollover is a career change. When transitioning between jobs or stepping into retirement, individuals often find themselves with employer-sponsored plans that may no longer suit their needs. Rolling these funds into an IRA can provide continuity and better control over retirement assets. Additionally, retirement can also prompt individuals to reevaluate their financial landscape, simplifying and consolidating accounts to streamline management and reduce fees. The investment landscape is vast and ever-evolving. Sometimes, existing retirement accounts might not offer the best or most diverse choices, especially in employer-sponsored plans with a limited selection. A rollover to an IRA can unlock a myriad of investment possibilities, allowing individuals to tailor their portfolios to their precise needs. Whether seeking specific sector funds, individual stocks, or bonds, an IRA can offer a broader palette, enhancing diversification and potential returns. Over the years, individuals can accumulate multiple IRAs from various sources. Each account could come with its fee structure, investment choices, and rules. Merging these accounts can simplify financial life, reduce fees, and offer a clearer view of the retirement picture. Having one consolidated account can make management easier, from reallocating assets to taking required minimum distributions. Plus, a consolidated view can provide a better grasp of overall risk and exposure. A Roth conversion is a specific type of rollover where funds from a traditional IRA are moved to a Roth IRA. This action has tax implications, as the transferred amount becomes taxable in the year of conversion. However, the subsequent benefits of tax-free withdrawals and no required minimum distributions from the Roth can make it an enticing option for some. The decision to convert should be made after careful consideration of current tax rates, expected future rates, and individual retirement goals. A Roth conversion can offer significant long-term advantages but is not a one-size-fits-all solution. The rules governing IRA rollovers are intricate, each with its set of requirements and implications. From 60-day windows to potential withholding taxes, understanding these rules is paramount for a smooth, error-free transition. By arming oneself with this knowledge, many common pitfalls can be avoided. This education not only ensures tax and penalty-free transfers but also imbues confidence in the decision-making process. Direct rollovers stand as the zenith in the world of rollovers. By moving funds directly between institutions, they bypass many pitfalls like potential withholding taxes or the stringent 60-day rule. Such transfers offer a seamless experience, ensuring the uninterrupted growth of retirement savings. While 60-day rollovers provide more control over funds for a brief period, direct rollovers offer peace of mind and simplicity. Given their straightforward nature, they're often the recommended route for most individuals. Once a rollover is in motion, vigilance is key. Monitoring the transition ensures that funds exit the original account and enter the new one seamlessly. Early detection of discrepancies or issues can prevent potential headaches and delays. Moreover, once funds reach the new account, it's essential to allocate them according to one's investment strategy. Leaving them uninvested can mean missed market opportunities and potential growth. When in doubt, seeking expert guidance can be invaluable. Financial advisors offer a wealth of experience and knowledge, helping navigate the maze of rollover rules and options. From tax implications to investment strategies, their counsel can ensure optimal decisions aligned with individual retirement goals. Whether you're uncertain about the rollover type, the potential tax implications, or the investment choices in the new account, an advisor can shed light, offering clarity and peace of mind. An IRA rollover offers a strategic avenue for individuals to transfer funds from one retirement account to another, primarily aiming to consolidate funds, attain better investment options, or navigate job transitions. The process is integral to retirement planning as it maintains the tax-advantaged status of retirement savings. Yet, executing this process requires a keen understanding of specific rollover types, each with its distinct procedures, potential tax implications, and inherent risks. Direct rollovers, for instance, are lauded for their straightforwardness, minimizing the risk of tax penalties. On the other hand, the 60-day rollover, while offering control, demands adherence to a strict deadline. Additionally, individuals need to be wary of common missteps, such as mixing pre-tax and post-tax funds or overlooking associated fees. With career changes, seeking diversified investments, or consolidating multiple IRA accounts acting as key triggers, a successful rollover strategy, supplemented with expert financial advice, can significantly optimize one's retirement financial landscape.What Is an IRA Rollover?

Understanding the IRA Rollover Process

Basics of Transferring Funds

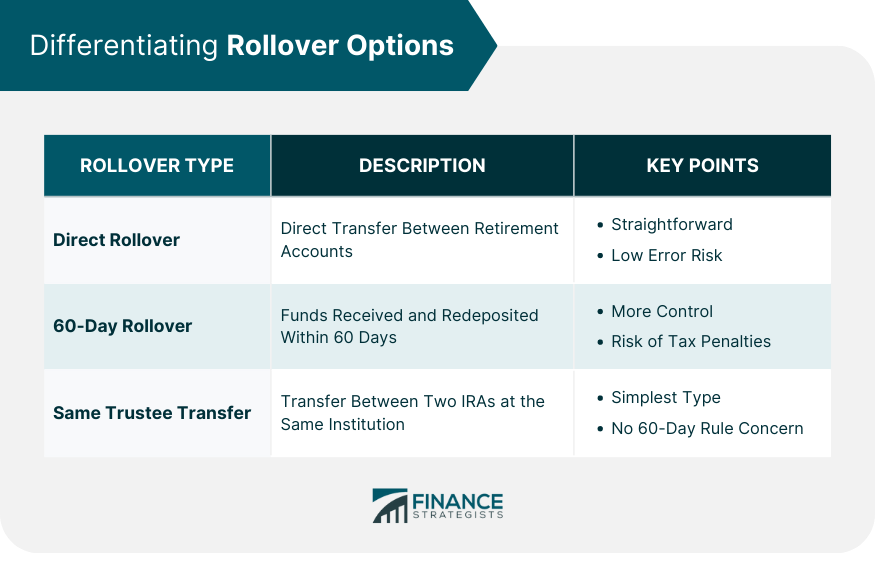

Differentiating Rollover Options

Direct Rollover

60-Day Rollover

Same Trustee Transfer

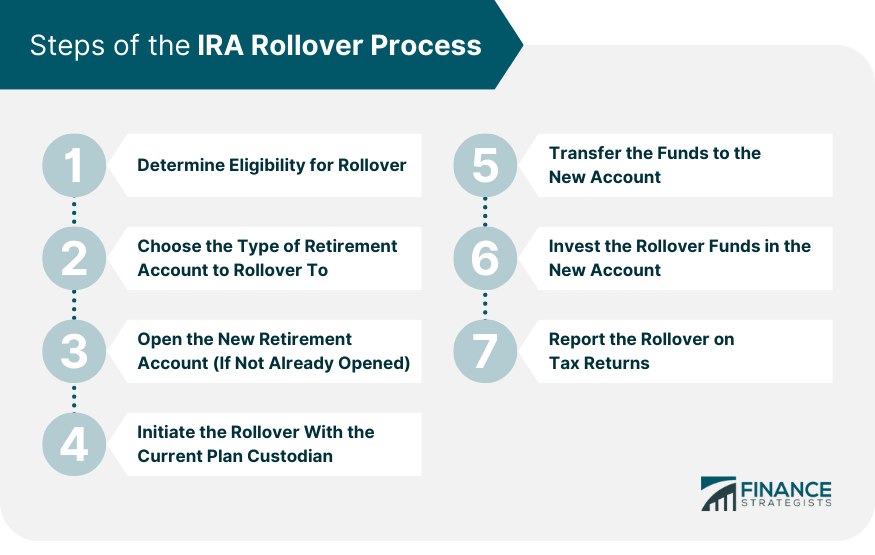

Steps of the IRA Rollover Process

Determine Eligibility for Rollover

Choose the Type of Retirement Account to Rollover To

Open the New Retirement Account (If Not Already Opened)

Initiate the Rollover With the Current Plan Custodian

Transfer the Funds to the New Account

Invest the Rollover Funds in the New Account

Report the Rollover on Tax Returns

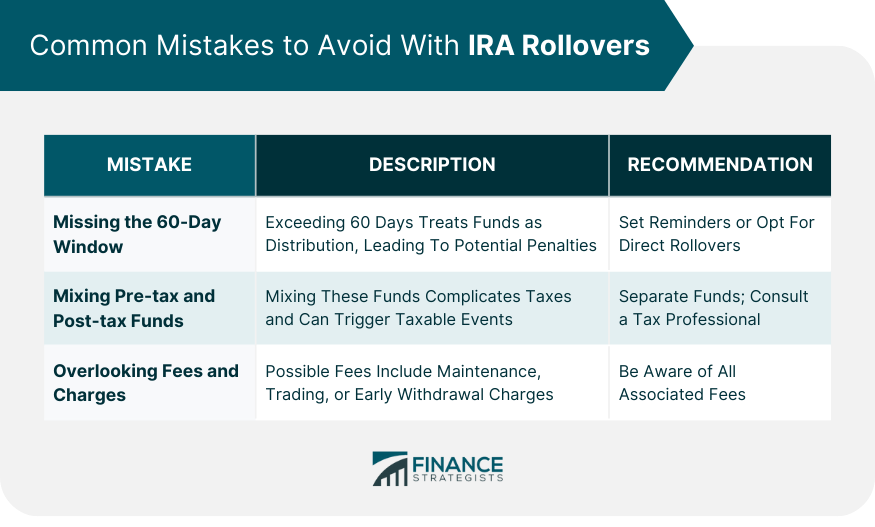

Common Mistakes to Avoid With IRA Rollovers

Missing the 60-Day Window

Mixing Pre-Tax and Post-Tax Funds

Overlooking Fees and Charges

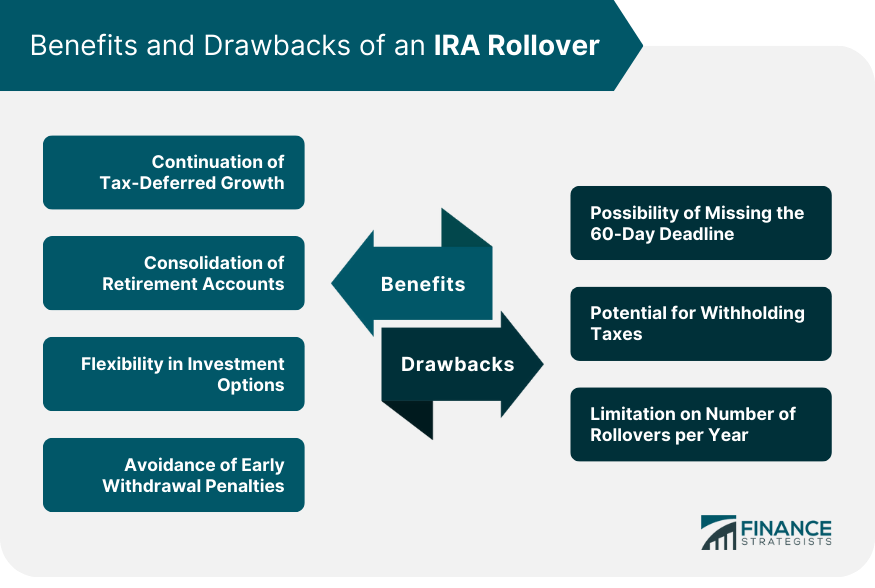

Benefits of an IRA Rollover

Continuation of Tax-Deferred Growth

Consolidation of Retirement Accounts

Flexibility in Investment Options

Avoidance of Early Withdrawal Penalties

Drawbacks of an IRA Rollover

Possibility of Missing the 60-Day Deadline

Potential for Withholding Taxes

Limitation on Number of Rollovers per Year

When to Consider an IRA Rollover

Changing Jobs or Retiring

Seeking Better Investment Choices

Consolidating Multiple IRA Accounts

Converting a Traditional IRA to a Roth IRA

Tips for a Smooth IRA Rollover Process

Ensure Understanding of the Rollover Rules

Engage in Direct Rollovers When Possible

Monitor the Transaction

Consult a Financial Advisor

Final Thoughts

IRA Rollover FAQs

An IRA rollover is a process where funds from one retirement account are transferred to another without tax penalties.

Changing jobs or retiring often leaves individuals with employer-sponsored plans that may not suit their current needs, making an IRA rollover a beneficial option.

An IRA rollover often provides access to a broader range of investment opportunities compared to limited options in employer-sponsored plans.

Common mistakes include missing the 60-day window, mixing pre-tax and post-tax funds, and overlooking fees and charges.

Consolidation simplifies financial management, provides a clearer retirement picture, and may reduce fees associated with maintaining multiple accounts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.