Individual Retirement Accounts (IRAs) stand as a beacon of hope for many aiming for a secure financial future. Serving as tax-advantaged investment vehicles, IRAs allow individuals to set aside funds for retirement, enjoying tax breaks that traditional savings accounts don't offer. These accounts come in various forms, each with its own set of rules and advantages, but all with the overarching goal of nurturing one's nest egg. The idea behind IRAs is not just to save but to invest. This distinction is vital because, unlike a regular savings account where your money may earn minimal interest, IRAs offer a world of investment possibilities. The growth potential of your retirement fund is often directly tied to these investment choices, making it paramount to comprehend the scope of options available. Absolutely, IRAs are not just designed for savings; they're built for investing. Stocks represent one of the many investment opportunities that IRA account holders can explore. By incorporating stocks, you open up your retirement savings to the growth potential of the equities market. But as with any investment, it's essential to tread wisely, doing due diligence before diving in. The process of buying stocks within an IRA is similar to a standard brokerage account. However, the tax implications differ, making IRAs particularly attractive. But before you begin, it's crucial to differentiate between the types of IRAs and their distinct features concerning stock investments. Both Traditional and Roth IRAs allow for stock investments. However, they have different tax structures that can influence an investor's approach. With Traditional IRAs, contributions are tax-deductible, but withdrawals during retirement are taxed. This setup is advantageous for individuals who believe their tax bracket will be lower during retirement than their working years. Roth IRAs operate differently. Contributions are made with post-tax dollars, meaning withdrawals in retirement are tax-free. This approach can be beneficial for those who anticipate a higher tax bracket in their golden years or those who value tax-free growth. Regardless of your choice, both IRA types allow the buying and selling of stocks, albeit with varied tax consequences. When you establish an IRA, especially a self-directed one, it's often done through a brokerage. This brokerage account within the IRA is your gateway to the stock market. Here, you can buy, hold, and sell stocks, just as you would with a standard brokerage account. The prime difference is the tax shield that IRAs provide. Just as with a typical brokerage account, you'd select stocks, place orders, and monitor your portfolio's performance. Brokerage accounts within IRAs also come equipped with research tools and resources, enabling investors to make informed decisions. However, it's pivotal to remember the unique rules and restrictions tied to IRA investments, ensuring compliance and optimizing returns. Selling stocks within an IRA is not only possible but also a strategic move for many investors. The decision to sell might be driven by a desire to lock in profits, cut losses, or rebalance a portfolio. The mechanics of selling are straightforward, but it's the implications of these sales that deserve close attention. The act of selling stocks in an IRA, in itself, does not trigger a taxable event. This is one of the prime benefits of IRAs. Only when you make withdrawals from the account, depending on the IRA type, might you face tax implications. So, effectively, you can realize gains (or losses) on stocks, move funds around within the IRA, and not worry about immediate tax consequences. Once you've decided to sell a stock within your IRA, the process is akin to that in any other brokerage account. You'd place a sell order, specifying the number of shares and the type of order (e.g., market, limit). After the sale is executed, the proceeds remain within the IRA, ready to be reinvested or left as cash. However, here's where the distinctiveness of IRAs comes into play. These proceeds, though now in cash form, still enjoy the IRA's tax-advantaged status. It means you can let this cash sit, invest in other assets, or even buy back into the same stock without tax implications. Though selling within an IRA doesn't immediately incur taxes, other implications may arise based on account actions. For instance, early withdrawals from an IRA before age 59½ usually attract a 10% penalty on top of any taxes due. It's also vital to distinguish between Traditional and Roth IRA withdrawals. While Roth IRAs allow tax-free and penalty-free withdrawals of contributions at any time, earnings are subject to restrictions. For Traditional IRAs, since contributions are made pre-tax, both the principal and earnings are taxed upon withdrawal. Therefore, while the act of selling stocks inside the IRA isn't taxable, the eventual withdrawals can be, depending on timing and the type of IRA in play. One of the principal attractions of IRAs is their tax efficiency. When you sell stocks in a regular brokerage account, capital gains – the profit from the sale – are subject to taxation. However, within an IRA, these gains are either deferred (Traditional IRA) or entirely tax-free (Roth IRA). This tax shield means that your investments can grow unburdened by yearly tax liabilities, offering a significant advantage over regular accounts. Consider this scenario: If you're frequently trading stocks, each sale in a regular account triggers a taxable event. But within an IRA, this isn't the case. You can trade, realize gains, and not fret about capital gains tax for the year. This structure can be incredibly advantageous for active traders or those who wish to compound their gains without immediate tax implications. Stocks offer a potent tool for diversification. While IRAs can house a variety of assets – from bonds to real estate – stocks play a unique role. They can bolster portfolio returns, hedge against inflation, and even provide dividend income. By buying and selling stocks within an IRA, you can tailor your retirement savings to reflect your financial goals and risk tolerance. Moreover, the universe of stocks is vast. From blue-chip companies to emerging startups, the stock market offers a spectrum of investment opportunities. Whether you're looking for stability, growth, or a mix of both, stocks can be maneuvered to fit your retirement strategy. And with the tax benefits of IRAs, these investments can grow and be adjusted over time without the yearly tax concerns. Asset allocation – the process of dividing your investments among various asset classes – is foundational to portfolio management. Over time, as certain investments outperform others, your original asset allocation might shift. Rebalancing is the act of realigning your portfolio to its intended allocation, and it often involves buying and selling assets. Within an IRA, the act of rebalancing becomes even more significant. Given the long-term nature of retirement savings, periodic rebalancing ensures that your portfolio stays aligned with your retirement goals. And with stocks being such a dynamic asset class, they often play a pivotal role in this process. For instance, if a stock or a set of stocks has had a stellar year, they might now occupy a larger portion of your portfolio than intended. Rebalancing would involve selling some of these outperformers and reallocating the proceeds to other assets. Within an IRA, such transactions can occur without immediate tax ramifications, making the process smoother and potentially more beneficial. Albert Einstein famously quipped that compound interest is the eighth wonder of the world. In the realm of investments, compounding is the process by which an investment earns interest (or returns), and then that interest earns interest of its own in subsequent periods. It's the snowball effect, and over long durations, it can lead to exponential growth. The advantage of buying and selling stocks within an IRA is that the capital gains aren't immediately siphoned off by taxes. Instead, the full amount remains invested, leading to more substantial compounding effects. For instance, if you sell a stock at a profit within your IRA, the entire proceeds (including the gain) can be reinvested. In a taxable account, you'd first have to pay capital gains tax, leaving a smaller amount for reinvestment. Over years, or even decades, this difference can lead to significantly larger retirement savings. The potency of compounding is accentuated when you consider dividend-paying stocks. If these dividends are automatically reinvested to buy more shares (a concept called dividend reinvestment), the growth can be even more pronounced. Given the long-term nature of IRAs, the power of compounding interest, especially from equities, can be a game-changer for retirement savings. Flexibility is at the heart of IRAs when it comes to stock investments. Unlike some employer-sponsored plans, which might have limited investment options, IRAs typically offer a broader range. Within this framework, you can choose individual stocks, allowing you to build a portfolio based on your research, convictions, and investment thesis. Let's say you're bullish about the tech sector's prospects. Within your IRA, you could invest in individual tech stocks, diving deep into companies you believe are poised for growth. On the other hand, if you're more comfortable with broader market exposure, you can opt for exchange-traded funds (ETFs) or mutual funds that track entire sectors or indices. This flexibility isn't just about personal convictions; it's also about risk management. By having the autonomy to pick and choose, you can design a portfolio that aligns with your risk tolerance, time horizon, and financial goals. This tailored approach, combined with the tax advantages of IRAs, can offer a robust strategy for retirement savings. While IRAs offer a plethora of investment opportunities, they're not without limitations. Certain transactions are prohibited within the IRA framework. For instance, you cannot borrow money from your IRA, sell property to it, or engage in other transactions that might benefit you or a disqualified person directly. A "disqualified person" includes the IRA owner, their spouse, ancestors, lineal descendants, and any spouse of a lineal descendant. Engaging in prohibited transactions can lead to severe consequences, including the disqualification of the entire IRA. It means the entire IRA would be considered distributed, leading to taxes and potential penalties. The rules around prohibited transactions ensure that IRAs serve their primary purpose: providing for retirement. They're designed to prevent self-dealing or other actions that could compromise the integrity of the retirement fund. As with all aspects of IRAs, awareness of these rules is paramount. Especially when dealing with stocks or other investments, it's pivotal to operate within the established guidelines. While IRAs generally provide a tax shield for investments, there's an exception to the rule: Unrelated Business Taxable Income (UBTI). If an IRA earns income from a business that isn't related to its primary purpose – like dividends or interest – this income might be subject to UBTI. For stock investors, UBTI often comes into play with certain types of investments like Master Limited Partnerships (MLPs). If an MLP generates income that falls under UBTI and exceeds a specific threshold, the IRA could owe taxes. It's a quirk in the tax code that many are unaware of, but it underscores the importance of understanding the intricacies of IRA investments. Navigating the maze of UBTI can be complex. However, most traditional stock investments, like shares in publicly traded companies, won't generate UBTI concerns. It's when venturing into more unconventional investments that UBTI becomes a potential issue. As always, due diligence and a keen understanding of tax implications are crucial. Traditional IRAs come with a stipulation: Once you reach a certain age (currently 73), you must start taking Required Minimum Distributions (RMDs). These RMDs are calculated based on your life expectancy and the total value of your IRA. Notably, Roth IRAs do not have RMDs during the account owner's life. While the concept of RMDs might seem straightforward, the mechanics can complicate stock investments. If a significant portion of your IRA is tied up in stocks, you might need to sell some of these holdings to meet your RMDs, especially if you wish to avoid tapping into other assets. This scenario can be particularly challenging during market downturns when selling might lock in losses. However, with careful planning, the impact of RMDs on stock holdings can be mitigated. Strategies might include maintaining a diverse asset mix, regularly rebalancing your portfolio, or holding dividend-paying stocks that generate cash flow. The key is to be proactive, understanding the implications of RMDs well in advance of the mandatory distribution age. The autonomy of managing an IRA can be a double-edged sword. On the one hand, the flexibility to choose your investments is empowering. On the flip side, without the guidance of professional advisory services, there's potential for missteps. It's worth noting that not all IRAs come devoid of advisory services. Many brokerage firms offer some level of guidance, whether through online tools, robo-advisors, or human financial advisors. However, if you're managing your IRA independently, you're charting your own course. The world of stocks is vast and can be complex. From understanding company fundamentals to deciphering market trends and macroeconomic indicators, stock investment requires due diligence. The absence of professional advice means that the onus of research, analysis, and decision-making falls squarely on the individual. For those who are passionate about investing and commit the time to understand the nuances, this self-directed approach can be rewarding. However, for others, the challenges might outweigh the benefits. It's essential to assess your comfort level, knowledge, and the time you can dedicate to managing your IRA before diving deep into stock investments. Liquidity refers to the ease with which an asset can be converted into cash without significantly affecting its price. Stocks, especially those of large publicly traded companies, are typically considered liquid assets. However, during volatile market conditions or in bear markets, selling stocks to raise cash can lead to significant losses. This liquidity concern becomes amplified within the context of an IRA. Suppose you're in a situation where you need to withdraw funds from your IRA, whether to meet RMDs or for other reasons. In that case, a bear market can force you into selling stocks at depressed prices. Such scenarios can erode the value of your retirement savings, especially if withdrawals are substantial or frequent. One way to mitigate these liquidity concerns is to maintain a diverse portfolio, ensuring that not all assets are tied up in stocks. Keeping a mix of bonds, cash, or other less volatile assets can provide a cushion during downturns. While stocks offer the allure of higher returns, understanding their liquidity risks, especially within the confines of an IRA, is crucial for informed decision-making. 401(k) plans, often sponsored by employers, are another popular retirement savings vehicle. Much like IRAs, 401(k)s offer tax advantages and the ability to invest in a variety of assets, including stocks. However, the scope and flexibility differ. Unlike IRAs, which typically offer a broader range of investment options, 401(k)s might have a curated list of funds or stocks to choose from. This limitation isn't necessarily a downside, as it can simplify decision-making for participants. On the other hand, for those looking for specific stock picks or niche investments, a 401(k) might feel restrictive. The tax treatment of 401(k)s and IRAs also varies, especially when considering Roth versions. While both vehicles allow for tax-deferred growth, the nuances of contributions and withdrawals differ. For those considering stock investments, understanding these nuances can be pivotal in optimizing returns and minimizing tax liabilities. While Traditional and Roth IRAs cater primarily to individuals, SEP (Simplified Employee Pension) IRAs and SIMPLE (Savings Incentive Match Plan for Employees) IRAs are designed for small businesses and the self-employed. Both SEP and SIMPLE IRAs allow for stock investments, but there are distinctions in contribution limits, withdrawal rules, and tax treatments. SEP IRAs, for instance, are funded by employer contributions only, and they can have significantly higher contribution limits compared to Traditional or Roth IRAs. This increased limit can be a boon for stock investors, allowing for more substantial investments in equities. SIMPLE IRAs, on the other hand, allow for both employer and employee contributions, with different contribution limits and matching rules. For small business owners or self-employed individuals looking to invest in stocks, understanding the nuances of SEP and SIMPLE IRAs can offer tailored strategies. While the core principles of stock investment remain the same, the mechanics of these specialized IRAs can influence decision-making. Outside the realm of retirement accounts lie standard brokerage accounts. These accounts offer the most flexibility when it comes to stock investments. You can buy, sell, and hold stocks without the constraints of contribution limits, withdrawal penalties, or RMDs. However, this flexibility comes at a tax cost. Unlike IRAs or 401(k)s, capital gains in non-retirement brokerage accounts are subject to taxation in the year they're realized. Whether you sell a stock at a profit or receive dividends, these earnings are taxable. This immediate tax implication can influence investment strategies, especially when considering the timing of buys and sells. For those who prioritize flexibility and are comfortable navigating the tax implications, non-retirement brokerage accounts offer a direct route to stock investments. However, for long-term, tax-optimized growth, IRAs and other retirement vehicles might hold the edge. The bedrock of any investment strategy is understanding your risk tolerance. It's a measure of how comfortable you are with volatility and potential losses. Given that retirement savings are meant for long-term goals, aligning your stock investments with your risk tolerance is pivotal. For some, a retirement portfolio might be heavily weighted towards equities, leveraging the potential for higher returns. For others, a more conservative approach, blending stocks with bonds or other stable assets, might be more palatable. Assessing risk isn't just about personal comfort; it's also about financial goals, time horizons, and other assets. It's worth noting that risk tolerance can evolve. As you approach retirement, a shift towards more stable assets might be prudent. Regularly reassessing your risk profile and adjusting your IRA stock investments accordingly can ensure that your retirement savings stay on track. While the age-old investment adage is to "buy and hold," the reality is more nuanced, especially within the confines of an IRA. Timing plays a role, not in the sense of market timing but considering personal factors like age and retirement horizons. For younger individuals, a longer runway until retirement might justify a more aggressive stance on stocks. This longer timeline can allow for recovery from potential market downturns. Conversely, as one nears retirement, the strategy might pivot towards preservation of capital, leading to more measured stock investments or sales. Market conditions, while unpredictable, can also influence decisions. In bullish markets, taking profits or rebalancing might be prudent. In downturns, considering the long-term nature of retirement savings, holding onto stocks or even buying more at depressed prices might align with certain strategies. Diversification is a cornerstone of investment strategy. When it comes to stock investments within an IRA, diversification can be achieved not just by holding different stocks but by ensuring exposure across various sectors. The rationale is simple: different sectors respond differently to economic conditions. While tech stocks might soar during certain market phases, utilities or consumer staples might hold ground during downturns. Spreading investments across sectors can provide a layer of protection against systemic market risks. By regularly assessing sector exposure and aligning it with broader economic trends and personal convictions, one can optimize the potential for growth and risk management. Dividend-paying stocks offer a unique proposition for IRAs. They provide not just the potential for price appreciation but also a steady stream of income in the form of dividends. Within the tax-advantaged environment of an IRA, these dividends can be reinvested without immediate tax liabilities, leading to compounded growth. For those nearing retirement or in retirement, dividend stocks can also offer a source of income without selling the underlying asset. This dual benefit – growth and income – can make dividend stocks a compelling choice for certain IRA strategies. However, it's essential to vet dividend stocks carefully. A high dividend yield might be enticing, but it's crucial to assess the company's fundamentals and the sustainability of these dividends. Ensuring that the company has a track record of stable dividend payments and the financial health to continue these payouts is pivotal. As mentioned earlier, rebalancing is a foundational strategy for IRA management. Given the dynamic nature of stocks, they often play a central role in rebalancing decisions. Regularly assessing your asset allocation, understanding deviations from intended targets, and realigning your portfolio can ensure that your retirement savings stay on course. The frequency of rebalancing can vary based on personal preferences and market conditions. Some might opt for annual rebalancing, while others might adjust their portfolios quarterly or even monthly. Regardless of the frequency, the goal remains the same: to ensure that your asset allocation aligns with your retirement goals and risk tolerance. As discussed earlier, RMDs are a reality for Traditional IRA holders past a certain age. For those with significant stock holdings, planning for these RMDs is crucial. It's not just about ensuring liquidity; it's also about optimizing the timing of stock sales. One strategy might involve maintaining a diverse asset mix, ensuring that stocks aren't the sole source for RMD withdrawals. Another approach might be to time stock sales during bullish market phases, banking the proceeds for future RMDs. For those with dividend-paying stocks, these dividends can be a source of funds for RMDs, potentially avoiding the need for stock sales. Ultimately, the key is to be proactive. Understanding RMD amounts well in advance, assessing the liquidity of your portfolio, and having a game plan can mitigate the potential impact of these mandatory distributions. IRAs provide a potent blend of tax advantages and investment flexibility, making them an invaluable tool for those planning for retirement. Yes, you can both buy and sell stocks within an IRA, harnessing the growth potential of the equities market while enjoying unique tax benefits. The selling of stocks within an IRA doesn't immediately trigger taxes, which sets it apart from standard brokerage accounts. However, while IRAs offer significant benefits, they also come with their own set of rules, especially concerning withdrawals and tax implications. When juxtaposed with other retirement vehicles like 401(k) plans or non-retirement brokerage accounts, IRAs stand out for their blend of investment diversity and tax efficiencies. Whether one opts for a Traditional, Roth, SEP, or SIMPLE IRA, understanding the nuances of each can empower investors to optimize their retirement savings and investment strategies.Overview of Individual Retirement Accounts (IRAs)

Understanding the Flexibility of IRAs

Can You Buy Stocks in an IRA?

Traditional IRA vs Roth IRA: Are There Differences?

Brokerage Accounts Within IRAs: Mechanism for Stock Purchase

Can You Sell Stocks in an IRA?

Selling Mechanics Within the IRA Framework

Implications of Selling: Taxes, Penalties, and More

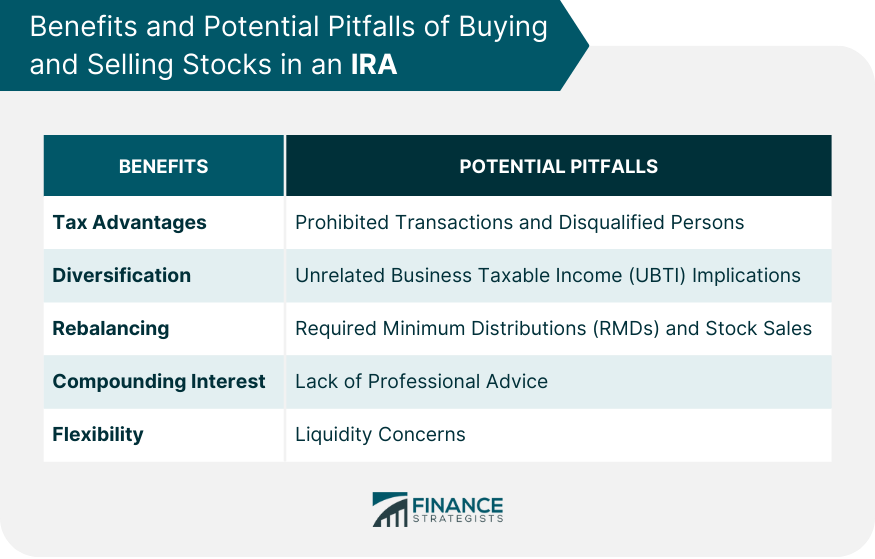

Benefits of Buying and Selling Stocks in an IRA

Tax Advantages

Diversification

Rebalancing

Compounding Interest

Flexibility

Potential Pitfalls and Limitations of Buying and Selling Stocks in an IRA

Prohibited Transactions and Disqualified Persons

Unrelated Business Taxable Income (UBTI) Implications

Required Minimum Distributions (RMDs) and Stock Sales

Lack of Professional Advice

Liquidity Concerns

Comparison to Other Retirement Vehicles

401(k) Plans

SEP IRAs and SIMPLE IRAs

Non-Retirement Brokerage Accounts

Strategies for Optimizing Stock Investments in an IRA

Assess Risk Tolerance for Retirement

Consider Timing Stock Buys and Sells

Diversify Across Industries

Utilize Dividend Stocks

Regularly Conduct Rebalancing to Stay on Target

Plan for Required Distributions

Bottom Line

Can You Buy and Sell Stocks in an IRA? FAQs

Stocks in IRAs offer potential growth, tax-deferred earnings, and compound interest, optimizing retirement savings.

RMDs necessitate withdrawals from IRAs after a certain age. Proper planning can prevent selling stocks at suboptimal times to meet these requirements.

In volatile or bear markets, converting stocks to cash might lead to significant losses, especially if forced to sell during downturns.

Dividend stocks offer both potential price appreciation and a steady income stream. Within IRAs, dividends can grow tax-deferred when reinvested.

Regular rebalancing ensures that your portfolio aligns with retirement goals and risk tolerance, especially amidst the dynamic nature of stocks.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.