Rollover IRAs are tools that bridge the gap between employer-sponsored retirement accounts and individual retirement accounts. When individuals leave a job or retire, they often face the decision of what to do with their 401(k) or other retirement funds. Transferring these funds directly into a Rollover IRA avoids immediate taxes and penalties. A Rollover IRA essentially preserves the tax-deferred status of your retirement assets. It's not merely a storage bin for old 401(k)s; it's a powerful vehicle for your retirement. By understanding its intricacies, you position yourself better to harness its advantages and steer clear of pitfalls. Understanding Rollover IRA withdrawal rules is crucial to avoid unexpected taxes and penalties. It not only protects your savings but also aids in formulating a robust retirement strategy, ensuring smoother financial transitions in retirement.

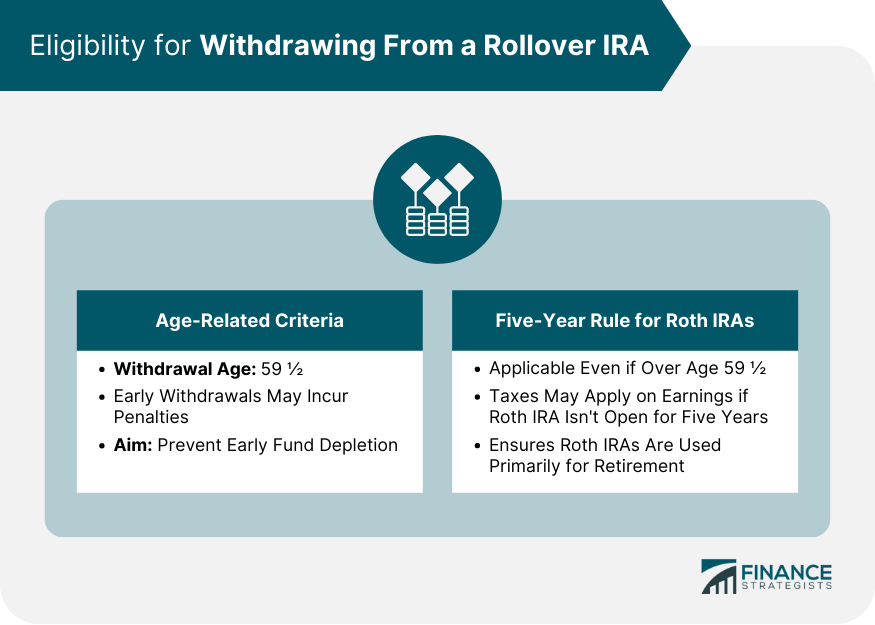

For most IRAs, the magic age number is 59 ½. Prior to this age, withdrawals can incur penalties unless certain exceptions apply. It’s a benchmark set by the IRS to encourage people to save for retirement and not deplete their funds prematurely. Age-based restrictions serve as a deterrent against impulsive decisions that could jeopardize long-term financial health. But remember, just because you've crossed this age threshold doesn't mean it's always the best time to withdraw. It's crucial to evaluate your financial landscape and retirement goals before tapping into these resources. Roth Rollover IRAs come with their own unique rule called the "five-year rule." Even if you’re past the age of 59 ½, if your Roth IRA hasn’t been open for at least five years, you might still face taxes on earnings. This rule aims to incentivize longer-term holding of Roth IRA assets. The concept behind this is simple: the government wants to ensure Roth IRAs serve their primary purpose, retirement savings. By instituting a holding period, it deters short-term, non-retirement use of these accounts. Withdrawals from a Rollover IRA are generally considered taxable income. This means if you pull out funds before the age of 59 ½, not only could you face a penalty, but you’ll also owe income taxes on the amount. This can significantly reduce the net amount you receive and potentially push you into a higher tax bracket. The tax bite can sting, especially if you're unprepared. It's crucial to factor in these tax implications before making any decisions about early withdrawal. While most withdrawals from Rollover IRAs are subject to regular income tax rates, it’s essential to remember that these rates can sometimes be higher than capital gains tax rates. This distinction makes a difference when deciding from which accounts to draw funds in a given year. Being strategic in tapping into different pots of money can save substantial tax dollars over the long run. By effectively managing withdrawals, you can optimize your post-retirement tax situation. Withdrawing from your Rollover IRA before age 59 ½ often comes with a 10% penalty. It's a substantial hit, especially on larger amounts. This penalty is on top of any income taxes you owe, making premature distributions quite costly. However, the story doesn’t end there. Several exceptions can provide relief from this hefty penalty, and knowing them can be a financial lifesaver. Fortunately, the IRS recognizes that life is full of unexpected events. Therefore, several exceptions can waive the 10% penalty, including certain medical expenses, higher education costs, and a first-time home purchase. Each exception has its own set of criteria, so it’s crucial to delve into the details before assuming you qualify. But these allowances provide some flexibility for those facing significant financial challenges. One sophisticated strategy to access your IRA funds early without penalties is the 72(t) rule. This rule allows for substantially equal periodic payments over your life expectancy or the joint life expectancy of you and a beneficiary. It provides a structured way to tap into retirement funds without the typical early withdrawal penalty. This approach requires commitment; once initiated, the payments must continue for five years or until the account holder reaches 59 ½, whichever is longer. It's a tactic that demands careful consideration but offers a valuable avenue for some. One of the unique features of Roth IRAs is the ability to withdraw your contributions (but not the earnings) at any time, tax-free and penalty-free. This flexibility can be a boon in emergencies. Remember, this applies to the amounts you've contributed, not the gains those contributions have earned. While this offers a degree of liquidity, it’s essential to track these amounts accurately to ensure you're not inadvertently withdrawing earnings and thus incurring penalties. The IRS also provides penalty exceptions for specific hardships like unreimbursed medical expenses or health insurance premiums during unemployment. Life events such as disability or being called to active duty may also exempt you from the early withdrawal penalty. It's heartening to know that in times of genuine crisis, there are provisions that might help. However, relying heavily on these exceptions should not become a retirement strategy. These are safety nets, not long-term planning tools. Rollover IRAs function similarly to Traditional IRAs in terms of tax treatment. The main distinction arises if you're dealing with a Roth Rollover IRA, which carries its own set of rules. While Traditional and Rollover IRAs tax withdrawals as ordinary income, Roth IRAs offer tax-free withdrawals after age 59 ½, provided the five-year rule is met. While the basic principles remain consistent across these accounts, nuances can greatly impact your tax situation. Being aware of these subtle differences ensures you're not caught off-guard. Rollover IRAs offer flexibility, especially when transitioning between jobs. These accounts allow you to consolidate multiple retirement accounts, making it easier to manage and strategize withdrawals. Consolidation can lead to clearer financial decision-making and a more cohesive retirement strategy. Moreover, Rollover IRAs often grant access to a broader range of investment options than employer-sponsored plans. This expanded investment palette can cater to a more diverse strategy, potentially optimizing returns and managing risks. Every financial move should be deliberate, especially when it comes to retirement savings. Before withdrawing from a Rollover IRA, weigh the urgency of your financial needs against potential taxes and penalties. Sometimes, it may be more prudent to seek alternative funding sources or cut expenses rather than raiding your retirement nest egg. Retirement funds are meant for the golden years. Before breaching this sanctuary, ensure it's truly the best option for your current and future financial health. The world of Rollover IRAs is intricate. Tax implications, penalties, and various rules can make navigating withdrawals daunting. This is where tax professionals come into play. Their expertise can guide you, ensuring you make informed decisions while minimizing adverse tax consequences. Remember, a brief consultation now could save significant money and heartache in the long run. There's immense value in tapping into expert knowledge, especially when charting complex financial terrains. If faced with financial needs, consider alternatives before withdrawing from your Rollover IRA. Personal loans, home equity lines of credit, or even renegotiating monthly bills can provide temporary relief. Sometimes, adjusting your budget or seeking additional income streams can alleviate financial pressures without compromising retirement savings. While these options come with their own sets of considerations, they may prove less costly in the long run than early IRA withdrawals. Always explore all avenues before making a decision. Withdrawing from a Rollover IRA requires careful consideration, given the intricate tax implications, potential penalties, and overarching strategies involved. A Rollover IRA provides a bridge between employer-sponsored and individual retirement accounts, ensuring continued tax-deferred status. While there are guidelines set by the IRS, like the age threshold of 59 ½ and the "five-year rule" for Roth IRAs, early withdrawals can result in significant costs, both from penalties and taxes. To safeguard one's long-term financial health, it's essential to deliberate on the urgency of needs against the consequences of withdrawing. For those navigating the complex world of Rollover IRAs, seeking advice from tax professionals is invaluable. Additionally, before drawing from your retirement fund, always consider alternative financial solutions. In sum, while you can withdraw from a Rollover IRA, understanding its rules and consequences ensures informed decision-making.Overview of a Rollover IRA

Eligibility for Withdrawing From a Rollover IRA

Age-Related Criteria

Five-Year Rule for Roth IRAs

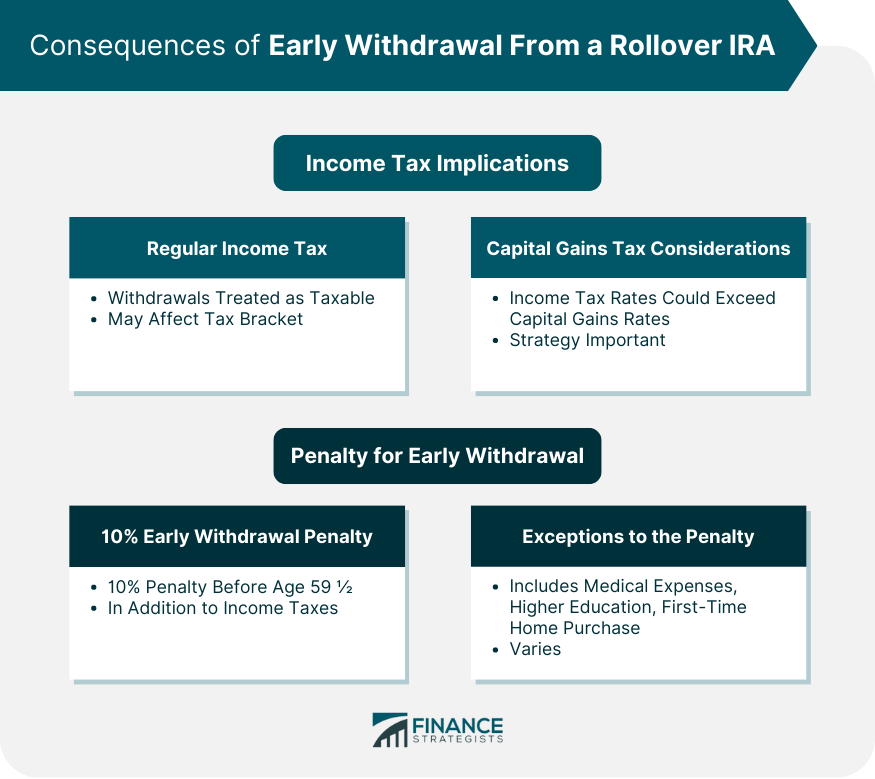

Consequences of Early Withdrawal From a Rollover IRA

Income Tax Implications

Regular Income Tax

Capital Gains Tax Considerations

Penalty for Early Withdrawal

10% Early Withdrawal Penalty

Exceptions to the Penalty

Strategies to Avoid Penalties

Utilize the 72(t) Rule for Substantially Equal Periodic Payments

Withdraw Only Contributions From a Roth Rollover IRA

Exceptions Related to Specific Hardships or Life Events

Rollover IRA vs Traditional and Roth IRA Withdrawal Rules

Comparison of Withdrawal Rules

Benefits of a Rollover IRA in Relation to Withdrawals

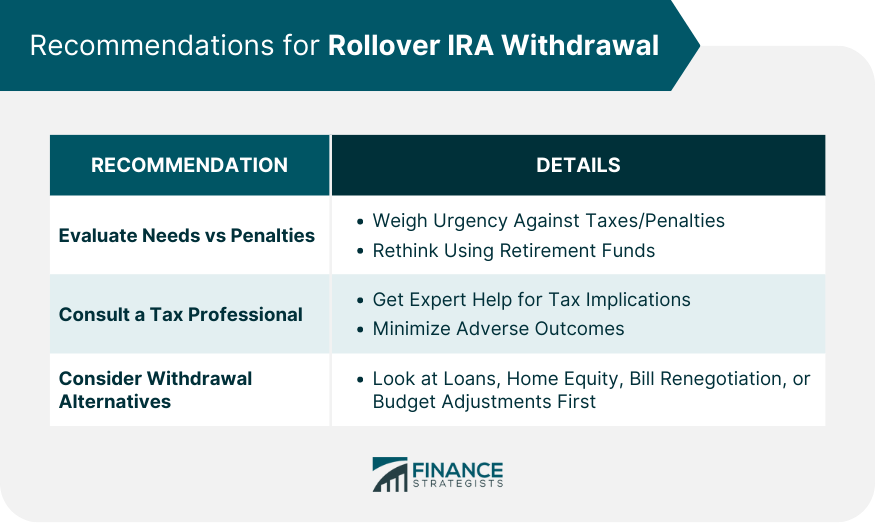

Recommendations for Rollover IRA Withdrawal

Evaluate Financial Needs vs Potential Penalties

Consult With a Tax Professional

Consider Alternatives to Withdrawal

Bottom Line

Can You Withdraw From a Rollover IRA? FAQs

A Rollover IRA is an account where you transfer funds from an employer-sponsored retirement plan, preserving their tax-deferred status.

Typically, you can withdraw without penalties after age 59 ½, but exceptions apply.

Early withdrawals are subject to regular income tax and may incur a 10% penalty unless specific exceptions are met.

Even after age 59 ½, Roth IRA withdrawals might face taxes on earnings if the account hasn't been open for at least five years.

Yes, methods include the 72(t) rule, withdrawing Roth IRA contributions, and leveraging penalty exceptions for hardships or specific life events.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.