Fannie Mae, officially the Federal National Mortgage Association (FNMA), is a government-sponsored enterprise (GSE) and a publicly traded company created by Congress to provide liquidity and stability to the housing market. Fannie Mae does not provide direct financing to consumers. Instead, it primarily purchases mortgages from lenders through its securitization process, which converts individual loans into securities that can be sold on the secondary mortgage market. It also offers other services like refinancing options and loan modification to help make homeownership more affordable for consumers with different income levels and credit histories. Fannie Mae was established in 1938 as part of President Franklin D. Roosevelt’s New Deal legislation when Congress authorized the federal government to purchase mortgages from lenders so that they could make additional loans accessible to homebuyers throughout the U.S. Fannie Mae created a secondary mortgage market, allowing lenders to increase the availability of home financing options. In 1968, it was publicly traded on the New York Stock Exchange (NYSE) and, by 1970, had become the largest source of mortgages in the U.S. In 2008, due to financial distress caused by the subprime mortgage crisis, its capital stock plummeted and was delisted from the NYSE. Fannie Mae was then put into conservatorship under the control of the Federal Housing Finance Agency (FHFA). Today, Fannie Mae continues with its mandate by buying home loans and mortgages, providing counseling services, and operating programs like HomePath. Fannie Mae works with lenders to purchase mortgage loans they have originated and then packages them into securities or collections of mortgages, which are sold on the secondary market to investors. In effect, Fannie Mae transfers lending risks from banks, mortgage lenders, and credit unions onto itself. This provides liquidity for lenders so they can continue providing home loans to new borrowers, as well as helping existing homeowners refinance their existing mortgages. HomePath is a program that helps buyers purchase foreclosed properties at attractive prices as an alternative to traditional financing. HomePath offers buyers incentives such as waived appraisal fees and mortgage insurance, as low as 3% down payment requirements, flexible mortgage terms and closing costs, and the ability to finance up to 95% of the home's purchase price. Fannie Mae's counseling services help potential home buyers make informed decisions about their financing options. It also offers free online courses on budgeting and money management to help families achieve long-term financial stability. It works with counselors to help individuals facing foreclosure or other financial issues. Counselors provide information such as forbearance plans and loan modifications. It also partners with a select group of organizations to provide additional assistance for low-income or first-time homebuyers. These programs include down payment assistance, lower interest rates on mortgages, extended repayment terms, and other incentives. Borrowers must meet minimum credit requirements to be eligible for Fannie Mae-backed mortgages. For a single-home primary residence, Fannie Mae mortgage programs require a minimum credit score of 620 for fixed-rate loans and 640 for adjustable-rate mortgages. However, some loan programs allow credit scores below 620 with additional requirements such as increased down payment amounts or higher interest rates. In general, borrowers will need to put down at least 5% of the purchase price or appraised value of the home to qualify for a loan though some Fannie Mae programs can require as low as a 3% down payment. This amount can be made up of cash from the borrower's own funds or other sources such as gifts from family members, government grants, employer assistance programs, and low-cost loans. Borrowers must have at least two months of mortgage payments in savings when applying to purchase or refinance through Fannie Mae. This serves as a buffer against any unexpected financial hardships that may arise after closing the loan, such as job loss or medical bills. A higher down payment can help lower cash reserve requirements because it reduces monthly payments and proves that you have the financial capacity to save money. Fannie Mae accepts a maximum of 36% ratio between total monthly income to total debt. A 45% DTI ratio can sometimes be considered depending on a borrower's credit score and reserve requirements. In addition, some Fannie Mae mortgages require that payments not exceed 28% of the borrower's gross monthly income. This requirement is referred to as the front-end ratio. Aside from HomePath, Fannie Mae also offers HomeReady, Standard 97% Loan-To-Value (LTV), HomeStyle Renovation, Standard Manufactured Housing, MH Advantage, and the Refi Plus/Home Affordable Refinance Program (HARP). This program allows borrowers to make a 3% down payment on a home purchase or refinance transaction. Borrowers can use a flexible source of cash for both the down payment and the closing charges. The total annual qualifying income for a HomeReady mortgage can be at most 80% of the AMI for the property's area. It requires borrowers to obtain mortgage insurance, adding a charge to monthly payments. Such insurance is reasonable and, in some cases, can be waived. This program offers a fixed-rate conventional mortgage with a 3% down payment requirement. Fannie Mae provides financing up to 97% of the loan amount to first-time homebuyers who exceed the income limits. Additionally, Fannie Mae offers lower interest rates and reduced Private Mortgage Insurance (PMI) costs compared to other programs. Homeownership is made more accessible and affordable for those without sufficient funds for a down payment. The HomeStyle Renovation Mortgage Program allows borrowers to finance both the purchase or refinance of a home and its renovation costs into one mortgage loan. You can use the existing equity in your home to finance renovation costs or purchase a property that needs renovation work. This program is designed to help borrowers purchase or refinance manufactured homes and the land on which they sit. The program allows for a loan amount of up to 95% LTV and provides financing for single-, double-, and triple-wide manufactured homes. Mortgage loans under this program should be for an owner-occupied or second home, and not be an investment property. The MH Advantage Mortgage Program is designed to help qualified borrowers purchase or refinance manufactured homes on permanent foundations. It also allows for a higher LTV (up to 97%) and a waived 0.5% loan level. They are also limited to owner-occupied or second homes and cannot be applied to investment properties. The Refi Plus/HARP Program helps current Fannie Mae loan holders refinance their mortgages even if they have little to no home equity. This program offers easier qualification criteria allowing homeowners to take advantage of lower interest rates and shorter loan terms. Under this program, Fannie Mae waives credit score requirements. It is only allowed for fixed-rate mortgages. Freddie Mac, formally known as the Federal Home Loan Mortgage Corporation (FHLC), is a GSE established in 1970. Like Fannie Mae, Freddie Mac helps increase the liquidity of mortgages by purchasing them from lenders and selling them as securities on the open market. They both compete in the secondary mortgage market to provide more affordable and accessible mortgages to qualified borrowers. Fannie Mae is larger, so it has a greater impact on the market than Freddie Mac. They differ in terms of mortgage sourcing. Fannie Mae usually buys mortgages from large commercial banks, while Freddie Mac typically buys mortgages from smaller lenders and credit unions. Fannie Mae is an integral part of the U.S. housing market. It provides mortgage programs that make homeownership more accessible and affordable for those who meet their qualification requirements. Its programs extend beyond home purchases and include refinancing or renovating properties. Like Fannie Mae, Freddie Mac helps increase the liquidity of mortgages and provides more affordable mortgages. Fannie Mae has a more extensive reach than Freddie Mac, primarily due to its funding source. Consult a qualified mortgage loan broker to learn more about Fannie Mae's programs and how they can help you get the financing you need.What Is Fannie Mae?

History of Fannie Mae

What Fannie Mae Does

Buys Home Loans and Mortgages

Operates HomePath

Provides Counseling Services

Fannie Mae Qualification Requirements

Credit Score

Down Payment

Cash Reserves

Debt-To-Income (DTI) Ratio

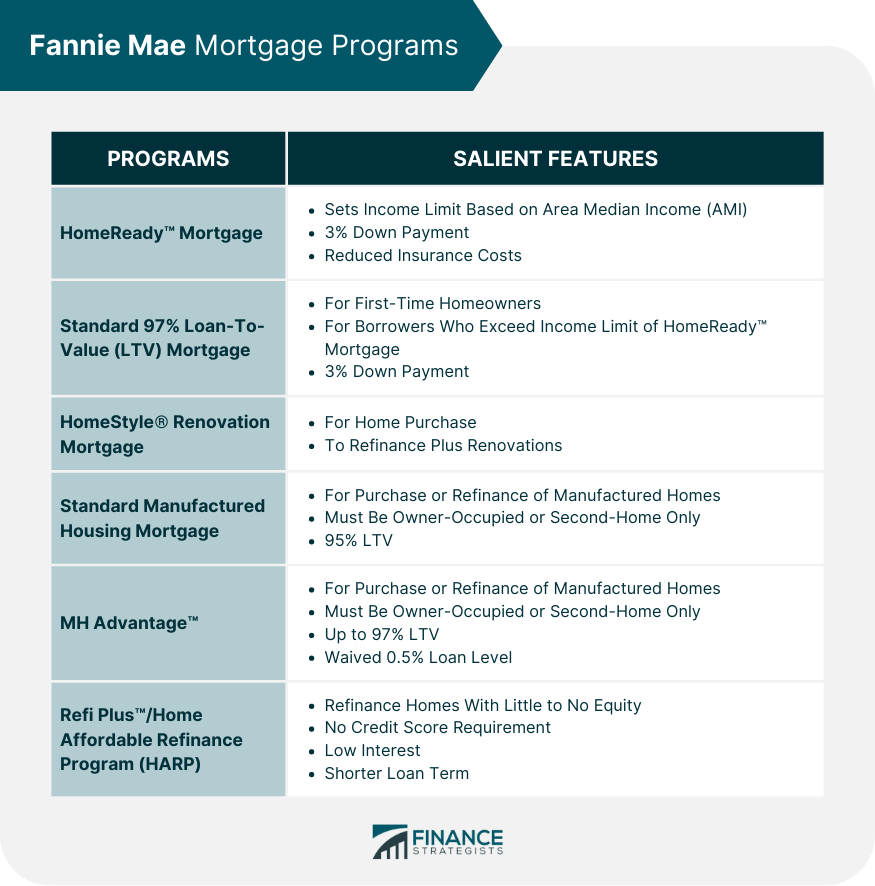

Fannie Mae Mortgage Programs

HomeReady Mortgage

Standard 97% LTV Mortgage

HomeStyle Renovation Mortgage

Standard Manufactured Housing Mortgage

MH Advantage

Refi Plus/HARP

Fannie Mae vs Freddie Mac

Final Thoughts

Fannie Mae FAQs

Fannie Mae loans offer several benefits to borrowers. These include lower down payments (as low as 3%), fixed-rate and adjustable-rate mortgages, more lenient eligibility requirements, and access to special loan programs such as HomeReady and HomeStyle mortgages.

Without Fannie Mae, the availability and affordability of mortgages for many people would be drastically reduced. Fannie Mae serves as a secondary market for mortgage loans, providing lenders with more liquidity to lend without having to keep mortgage loans on their books. Without this secondary market, borrowers could have difficulty finding mortgages from traditional lenders, leading to higher interest rates or less favorable loan terms.

Fannie Mae and Freddie Mac are government-sponsored enterprises (GSE) tasked with helping increase access to mortgages by providing liquidity in the housing market. They differ mainly in where they source their mortgages: Fannie Mae from large commercial banks and Freddie Mac from smaller community banks and credit unions.

To qualify for a Fannie Mae loan, borrowers must meet specific criteria, including a good credit score, demonstrating enough income to cover the mortgage payments, a competitive debt-to-income (DTI) ratio, and having sufficient funds for a down payment (if applicable).

During the financial crisis of 2008, Fannie Mae was delisted from the New York Stock Exchange (NYSE) and taken over by the federal government as part of a bailout package. Since then, it has been under conservatorship and is managed by the Federal Housing Finance Agency (FHFA). Despite this, Fannie Mae continues to provide liquidity in the housing market and access to mortgages for many borrowers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.