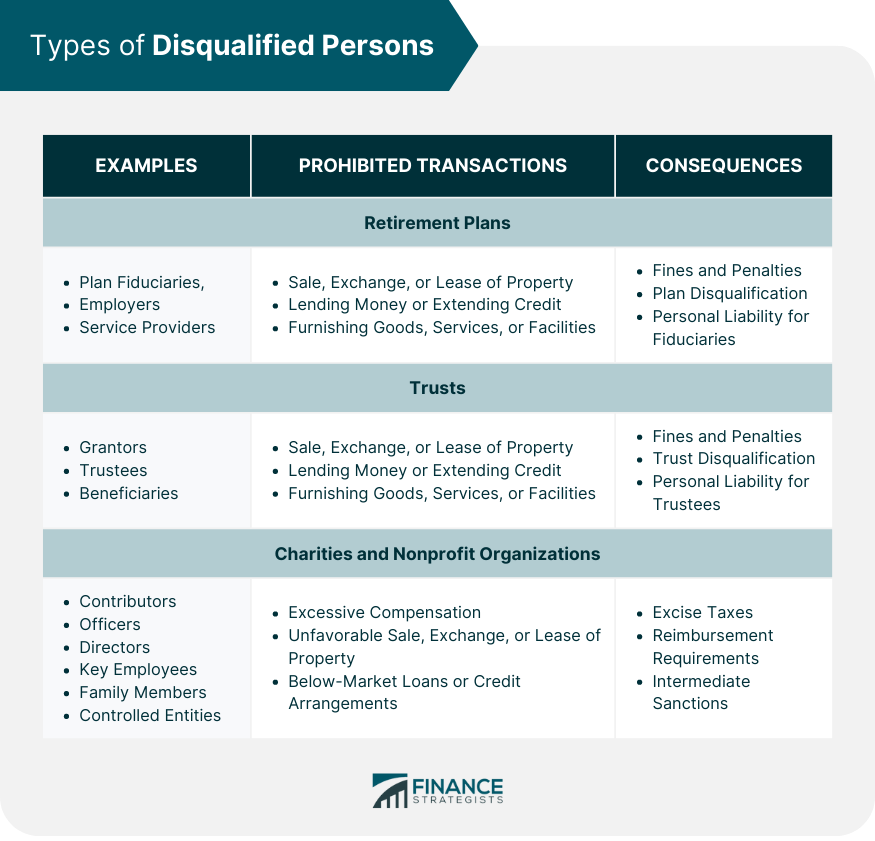

"Disqualified persons" is a term used in the context of the Internal Revenue Code (IRC) to refer to certain individuals and entities that are prohibited from engaging in certain transactions with certain types of tax-exempt organizations, such as private foundations and individual retirement accounts (IRAs). These persons typically include individuals or entities that have a close relationship with an organization or have the ability to exert influence over its decisions. This can include, but is not limited to, the organization's officers, directors, trustees, and key employees, as well as their family members and business entities they control. The concept of "disqualified persons" is primarily relevant to the rules governing prohibited transactions and self-dealing, which are designed to prevent conflicts of interest and abuse of tax-exempt status. These rules generally prohibit disqualified persons from engaging in certain transactions with the organization, such as selling or exchanging property, lending money or extending credit, or furnishing goods, services, or facilities. In retirement plans, disqualified persons are individuals or entities with significant influence or control over the plan. Examples of disqualified persons in retirement plans include: Plan Fiduciaries: Individuals responsible for managing the plan or its assets, such as plan administrators, trustees, and investment managers. Employers and Employee Organizations: Sponsoring organizations and those responsible for establishing or maintaining the plan. Service Providers to the Plan: Entities providing services to the plan, such as record keepers, consultants, and investment advisors. Prohibited transactions are dealings between a retirement plan and a disqualified person that the Internal Revenue Code specifically forbids. Examples of prohibited transactions include: Sale, exchange, or lease of property between the plan and a disqualified person. Lending money or extending credit between the plan and a disqualified person. Furnishing goods, services, or facilities between the plan and a disqualified person. Engaging in prohibited transactions with disqualified persons can lead to severe consequences, including: Fines and Penalties: Both the disqualified person and the retirement plan may face excise taxes. Disqualification of Retirement Plans: The plan may lose its tax-exempt status, resulting in adverse tax consequences for the plan and its participants. Personal Liability for Fiduciaries: Fiduciaries may be held personally liable for any losses incurred by the plan due to prohibited transactions. Disqualified persons in the context of trusts include individuals or entities with substantial influence or control over the trust. Examples of disqualified persons in trusts include: Grantors: The individual or entity that establishes the trust. Trustees: The individual or entity responsible for managing the trust and its assets. Beneficiaries: Individuals or entities designated to receive the benefits of the trust. Prohibited transactions in trusts involve dealings between the trust and a disqualified person violating specific Internal Revenue Code provisions. Examples of prohibited transactions include: Sale, exchange, or lease of property between the trust and a disqualified person. Lending money or extending credit between the trust and a disqualified person. Furnishing goods, services, or facilities between the trust and a disqualified person. Engaging in prohibited transactions with disqualified persons in trusts can result in significant consequences, such as: Fines and Penalties: Both the disqualified person and the trust may face excise taxes. Trust Disqualification: The trust may lose its tax-exempt status, leading to adverse tax consequences for it and its beneficiaries. Personal Liability for Trustees: Trustees may be held personally liable for any losses incurred by the trust due to prohibited transactions. In the context of charities and nonprofit organizations, disqualified persons are individuals or entities with substantial influence over the organization. Examples of disqualified persons in charities and nonprofits include: Substantial Contributors: Donors who have made significant financial contributions to the organization. Officers, Directors, and Key Employees: Individuals responsible for the organization's management, governance, and operations. Family Members of Disqualified Persons: Spouses, children, parents, and siblings of disqualified persons, as well as their spouses. Controlled Entities: Businesses or organizations where a disqualified person holds a significant ownership or controlling interest. Excess benefit transactions involve dealings between a charity or nonprofit organization and a disqualified person, resulting in the disqualified person receiving an economic benefit that exceeds the value of the goods or services provided to the organization. Examples of excess benefit transactions include: Excessive compensation paid to officers, directors, or key employees. Sale, exchange, or lease of property between the organization and a disqualified person at an unfavorable price. Loans or credit arrangements with disqualified persons at below-market interest rates. Engaging in excess benefit transactions with disqualified persons can lead to severe consequences for charities and nonprofit organizations, such as: Excise Taxes: Both the disqualified person and the organization's management may be subject to excise taxes. Reimbursement Requirements: The disqualified person may be required to return the excess benefit to the organization. Intermediate Sanctions: The Internal Revenue Service (IRS) may impose penalties on the organization, its management, or the disqualified person, including fines, suspension of tax-exempt status, or revocation of tax-exempt status. To effectively manage disqualified persons and minimize the risk of prohibited transactions or excess benefit transactions, organizations should implement strategies to identify disqualified persons in various contexts. These strategies may include: Regularly reviewing the organization's governing documents and policies. Examining relationships between the organization and its donors, officers, directors, and key employees. Assessing the organization's transactions and financial relationships for potential conflicts of interest. Organizations can implement best practices to prevent prohibited transactions or excess benefit transactions, such as: Implementing Internal Controls and Policies: Establish and enforce policies to prevent conflicts of interest, review financial transactions, and ensure compliance with relevant regulations. Regularly Reviewing Transactions: Conduct periodic reviews of the organization's financial transactions to promptly identify and address potential issues. Seeking Professional Advice: Consult with legal, tax, and financial professionals to ensure the organization adheres to relevant laws and regulations. Disqualified persons are individuals or entities prohibited from engaging in certain transactions with tax-exempt organizations, including retirement plans, trusts, and charitable organizations. These individuals and entities typically have a close relationship with the organization or the ability to influence its decisions. The rules governing prohibited transactions and self-dealing are designed to prevent conflicts of interest and abuse of tax-exempt status. The consequences of engaging in prohibited transactions with disqualified persons can be severe, including fines and penalties, disqualification of retirement plans or trusts, personal liability for fiduciaries or trustees, and excise taxes. Organizations can implement strategies to identify disqualified persons and prevent prohibited transactions or excess benefit transactions by regularly reviewing governing documents and policies, assessing transactions and financial relationships, implementing internal controls and policies, and seeking professional advice. It is essential for organizations to be aware of disqualified persons and to manage their relationships with them to ensure compliance with relevant regulations and prevent adverse consequences. By implementing best practices and strategies to identify and manage disqualified persons, organizations can maintain their tax-exempt status and avoid penalties and liabilities.What Are Disqualified Persons?

Disqualified Persons in Retirement Plans

Definition and Examples

Prohibited Transactions

Consequences

Disqualified Persons in Trusts

Definition and Examples

Prohibited Transactions

Consequences

Disqualified Persons in Charities and Nonprofit Organizations

Definition and Examples

Excess Benefit Transactions

Consequences

Identifying and Managing Disqualified Persons

Strategies to Identify Disqualified Persons

Best Practices to Prevent Prohibited Transactions or Excess Benefit Transactions

Conclusion

Disqualified Persons FAQs

Disqualified Persons are individuals or entities with significant influence or control over a non-profit organization, including board members, officers, substantial contributors, and their family members.

Identifying Disqualified Persons is crucial to prevent self-dealing transactions, which can result in excise taxes and penalties for both the Disqualified Persons and the private foundation.

Disqualified Persons can jeopardize a non-profit's tax-exempt status if they engage in excess benefit transactions or self-dealing, leading to penalties and potential loss of the organization's tax-exempt status.

Yes, there are exceptions for certain transactions that may involve Disqualified Persons, such as providing goods or services at fair market value without personal gain, as long as they don't violate the self-dealing rules.

Yes, Disqualified Persons can be removed or replaced following proper procedures in the organization's bylaws and ensuring that the change does not result in any conflicts of interest or self-dealing activities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.