A self-directed Individual Retirement Account (IRA) is a type of retirement account that allows investors greater control over their investment choices compared to traditional IRAs. These accounts permit investments in a broader range of assets, including alternative investments such as real estate, private equity, and precious metals. While both self-directed and traditional IRAs are tax-advantaged retirement accounts, the key difference lies in the available investment options. Traditional IRAs typically limit investment choices to stocks, bonds, and mutual funds. In contrast, self-directed IRAs offer a more extensive array of investment opportunities. A self-directed Traditional IRA functions similarly to a regular Traditional IRA but allows for a wider range of investment options. Contributions are tax-deductible, and taxes are deferred until withdrawals are made during retirement. Self-directed Roth IRAs operate like traditional Roth IRAs, with the primary distinction being the broader investment choices. Contributions are made with after-tax dollars, and qualified withdrawals during retirement are tax-free. A self-directed Simplified Employee Pension (SEP) IRA is designed for self-employed individuals and small business owners. It offers the same investment flexibility as other self-directed IRAs while allowing higher contribution limits. A Savings Incentive Match Plan for Employees (SIMPLE) IRA is another option for small businesses and the self-employed. Self-directed SIMPLE IRAs provide the same investment freedom, with the added benefit of employer contributions. Eligibility for self-directed IRAs depends on the specific account type. Generally, individuals must have earned income and be below certain income thresholds to contribute to a Traditional or Roth IRA. SEP and SIMPLE IRAs have specific requirements for business owners and employees. Contribution limits for self-directed IRAs are the same as their traditional counterparts. For 2026, the limit is $7,500 ($7,000 in 2025) for individuals under age 50 and $8,600 ($8,000 in 2025) for those aged 50 or older. SEP and SIMPLE IRAs have different limits based on income and employer contributions. Individuals aged 50 or older can make additional catch-up contributions to their self-directed IRAs. The catch-up limit for Traditional and Roth IRAs is $1,100 for 2026 ($1,000 in 2025), while the limits for SEP and SIMPLE IRAs vary. Rollovers and transfers can be made between self-directed IRAs and other qualified retirement accounts, subject to specific rules and regulations. Investing in real estate through a self-directed IRA can include rental properties, commercial real estate, and land development projects. Private equity investments involve purchasing shares in privately held companies. This can offer the potential for significant returns but may also entail higher risk. Self-directed IRAs can hold certain types of precious metals, such as gold and silver bullion or coins, as a long-term store of value and hedge against inflation. Private loans, including mortgages and promissory notes, can be made through a self-directed IRA. This strategy can generate income through interest payments. Some self-directed IRAs allow investments in cryptocurrencies, such as Bitcoin and Ethereum. This can offer potential for high returns but may also involve significant volatility and risk. Additional alternative investments for self-directed IRAs include tax lien certificates, limited partnerships, and various other unique assets. Certain transactions are prohibited within a self-directed IRA, such as dealing with disqualified persons (e.g., the account holder, their spouse, or certain family members) or engaging in self-dealing. Income generated from investments in active businesses, such as limited partnerships or an LLC, may be subject to unrelated business taxable income (UBTI) within a self-directed IRA. Traditional, SEP, and SIMPLE self-directed IRAs are subject to required minimum distributions (RMDs) starting at age 72. Roth IRAs do not have RMD requirements. Withdrawals made before age 59½ from a self-directed IRA may be subject to a 10% early withdrawal penalty and additional taxes, depending on the account type and circumstances. Tax implications for self-directed IRAs depend on the specific account type. Traditional and SEP IRAs offer tax-deductible contributions and tax-deferred growth, while Roth and SIMPLE IRAs provide different tax benefits. A custodian is a financial institution responsible for holding and administering the assets within a self-directed IRA. They ensure compliance with IRS rules and regulations. When choosing a self-directed IRA custodian, consider factors such as fees, customer service, investment options, and the institution's reputation and experience in the industry. Different custodians may charge varying fees for account maintenance, transactions, and other services. Compare fees and service offerings when selecting a custodian. Some popular self-directed IRA custodians include Equity Trust, Entrust Group, and Pensco Trust Company. Research and compare multiple custodians before making a decision. Choose a self-directed IRA custodian. Complete the account application and provide the required documentation. Fund the account through contributions, transfers, or rollovers. Select and manage investments in compliance with IRS rules and regulations. Funding a self-directed IRA can be done through regular contributions, transfers from other Individual Retirement Account (IRA), or rollovers from qualified retirement plans. Once the account is funded, choose investments that align with your financial goals and risk tolerance. Regularly monitor and manage investments to optimize performance and maintain diversification. Maintain accurate records of all transactions and provide required reports to the IRS and custodian to ensure compliance. Investing heavily in alternative assets may result in a lack of diversification, increasing the overall risk of the portfolio. Some alternative investments, such as real estate and private equity, may have limited liquidity, making it more difficult to sell or access funds when needed. Investors are responsible for conducting thorough due diligence on all investments within a self-directed IRA to minimize risks and avoid potential scams or fraud. Due to the complex nature of alternative investments, self-directed IRAs can be more susceptible to fraud or scams. Be cautious and conduct thorough research before investing.

Ensure a well-diversified portfolio by investing in a mix of traditional and alternative assets. This strategy can help manage risk and potentially enhance returns. Conduct thorough research and due diligence on all investment opportunities within a self-directed IRA to minimize risk and make informed decisions. Consult with financial advisors, tax professionals, or attorneys to ensure compliance with regulations and receive guidance on investment strategies tailored to your specific goals and risk tolerance. Monitor changes in laws and regulations related to self-directed IRAs to maintain compliance and adapt investment strategies as needed. Self-directed IRAs offer investors the opportunity to diversify their retirement portfolios with a broader range of investment options, including alternative assets. While these accounts can provide potential for higher returns, they also come with unique risks and challenges. The potential benefits of self-directed IRAs include greater diversification, access to unique investment opportunities, and the potential for higher returns. However, these accounts also involve risks such as lack of diversification, liquidity concerns, and the need for extensive due diligence. Before opening a self-directed IRA, weigh the potential benefits and risks, and consider your investment goals, risk tolerance, and expertise. Consult with professionals, research custodians, and stay informed about regulatory changes to make the most of this unique investment vehicle.What Are Self-Directed IRAs?

Definition and Overview

Differences Between Self-Directed IRAs and Traditional IRAs

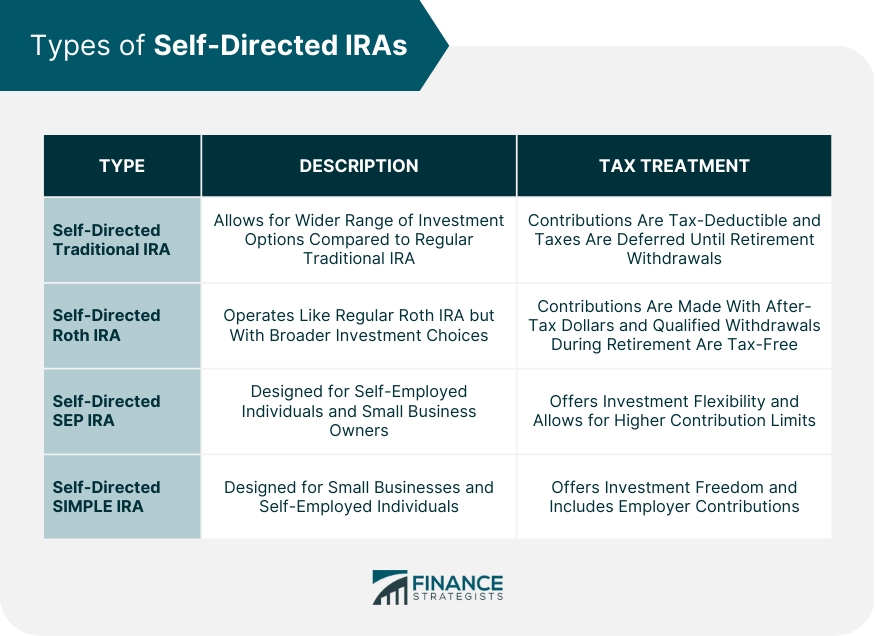

Types of Self-Directed IRAs

Self-Directed Traditional IRA

Self-Directed Roth IRA

Self-Directed SEP IRA

Self-Directed SIMPLE IRA

Eligibility and Contribution Limits

Eligibility Requirements

Annual Contribution Limits

Catch-up Contributions

Rollovers and Transfers

Investment Options for Self-Directed IRAs

Real Estate

Private Equity

Precious Metals

Private Loans

Cryptocurrency

Other Alternative Investments

Rules and Regulations

Prohibited Transactions

Unrelated Business Taxable Income (UBTI)

Required Minimum Distributions (RMDs)

Early Withdrawal Penalties

Tax Implications and Benefits

Choosing a Self-Directed IRA Custodian

Role of a Custodian

Factors to Consider When Selecting a Custodian

Comparing Fees and Services

Commonly Used Custodians

Setting up a Self-Directed IRA

Steps to Establish a Self-Directed IRA

Funding the Account

Selecting and Managing Investments

Recordkeeping and Reporting

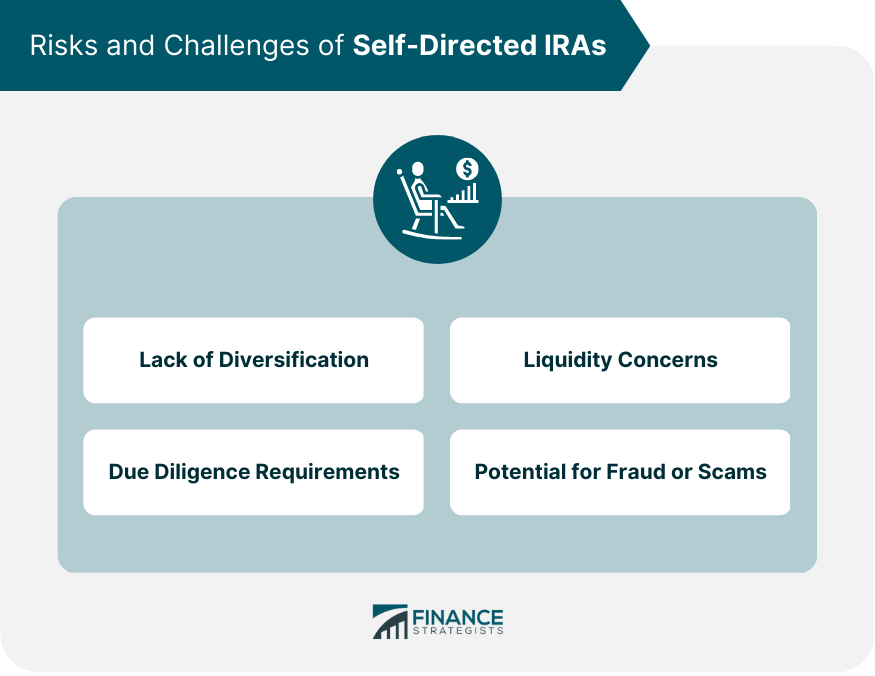

Risks and Challenges

Lack of Diversification

Liquidity Concerns

Due Diligence Requirements

Potential for Fraud or Scams

Strategies for Success

Diversifying Investments

Research and Due Diligence

Seeking Professional Advice

Staying Up to Date With Regulatory Changes

Conclusion

Self-Directed IRAs FAQs

A Self-Directed IRA is an individual retirement account that allows investors to direct their investments into a wide range of alternative assets such as real estate, private equity, precious metals, and cryptocurrency. Unlike traditional IRAs, SDIRAs provide greater flexibility and control over investment decisions.

Anyone who is eligible to open a traditional IRA can open a Self-Directed IRA. This includes individuals who are under the age of 70.5 and have earned income. However, it is important to note that not all IRA custodians offer SDIRAs, so it is important to research and choose a custodian that specializes in SDIRAs.

The benefits of investing in a Self-Directed IRA include greater control over investment decisions, the ability to invest in a wider range of assets, potential for higher returns, and tax advantages. Additionally, SDIRAs can provide a hedge against inflation and market volatility.

The risks associated with investing in an SDIRA include lack of diversification, lack of liquidity, and the potential for fraud or scams. Additionally, SDIRAs require a higher level of due diligence and expertise to ensure that investments are in compliance with IRS regulations.

The IRS rules and regulations governing Self-Directed IRAs are the same as those governing traditional IRAs. However, SDIRAs require a higher level of due diligence and expertise to ensure that investments are in compliance with IRS regulations. It is important to consult with a qualified tax professional before making any investment decisions in an SDIRA.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.