Underwriting occurs when individuals or organizations assume financial risk in exchange for payment. Financial risk is the risk that a company may not generate enough cash flow or revenue to fulfill its financial obligations. Loans, insurance, and investments are common sources of risk. The risk associated with a loan is whether or not it will be repaid and that the borrower does not have a history of loan defaults. Insurance risk includes the potential for an excessive number of policyholders that submit claims at once. In dealing with securities, underwritten investments have a chance to lose money. The underwriters look at everything related to an application, including financial situation and overall health. They typically work for companies that offer mortgages, loans, insurance, and investments. They assist these companies in deciding whether to accept an applicant's contract based on their findings and the associated level of risk. In the financial industry, underwriting is essential since it enables investors to choose profitable investments. Underwriting can be broadly categorized as belonging to the loan, insurance, and securities categories. Loan underwriting involves evaluating the borrower's financial background, income, and credit standing. Lenders assess the financial risk that a borrower has before lending them money. An assurance that the investment can be paid and that the borrower does not frequently let loans default is necessary. Loans that are secured are mortgages. If they default on a secured loan, the borrower pledges collateral to the lender. There are two standard practices among lenders for underwriting, automated and manual. Although a manual approach might be more advantageous for unique circumstances, automatic underwriting is quicker. In this approach, one can speak with an underwriter about the circumstances rather than letting the computer system flag one as an unsuitable borrower. A lender might recognize the need for a manual underwriter if the finances could be more straightforward. Insurance underwriting assesses insurance applications to determine whether to offer insurance and, if so, under what conditions. When assessing risk, age, gender, and medical history are just a few of the rate factors underwriters consider. For instance, smokers and alcoholics rates will probably be more significant than those who are not. Rating variables and determined risk level determine the cost of insurance. The Affordable Care Act (ACA) was enacted more than ten years ago. The ACA abolished patient cost-sharing for high-value preventive care and formalized safeguards for those with prior diseases. Securities underwriting assesses risk and sets prices for particular securities, most often related to an Initial Public Offering (IPO). Underwriting assesses the company's viability and potential for success before going public to ensure that investors, usually an investment bank, have the information needed to make an informed decision. Based on the findings of the underwriting process, the investment bank would buy the securities issued and then sell those in the market. If more than one underwriter is involved in purchasing these securities, it is referred to as an underwriter syndicate. An underwriter syndicate is used when an issue is too big for one firm to handle to aggregate several companies' resources. The underwriting process starts after the applicant submits the documentary requirements. It can take different methods for each type. Here are the major steps of the underwriting process: The underwriter reviews the application and related documents to determine any risk factors involved. For loan underwriting, the borrower’s credit history, financial records, and the value of the loan collateral are assessed. In the case of life insurance applications, age, lifestyle, alcohol, and substance use are important considerations. To value security, underwriters review the company's financial records, cash flow statements, and liabilities. After fully understanding these factors, a proper pricing solution is proposed. The underwriter identifies risk factors and how much it would cost to cover the risks involved. Policy premium is computed based on the likelihood that these risks will happen. Underwriters use different techniques in evaluating risks. With the available information, companies can generate a report that covers the financial, physical, and ethical aspects heightening the risk factors. The underwriter comes up with a professional and unbiased valuation of a property or security and the medical risks in the case of insurance underwriting. Property appraisals are done considering the property's condition, location, and features, compared with the market value. In the case of life insurance, a medical exam is required to assess the medical risks of the applicant. For securities, appraisal considers the fair market value of the underlying asset. After the assessment and appraisal process, a decision to approve, disapprove or label the application as pending has to be made. Approve: A low-risk application usually gets approval. Loan rates and terms, premium amounts, or what price to pay for securities are stipulated. Disapprove: The underwriter disapproves the application when various factors exhibit signs of high risk. Pending: If an underwriter decides to hold the application, they either need more information or the correct information to decide. During the underwriting process, details on the following are required: (1) income, (2) employment status, (3) assets and liabilities, (4) credit history and credit rating, and (5) medical history. Underwriters need information on income and income sources to assess the applicant's capacity to pay the loan. The standard documents required to verify income are wage and tax statements, pay stubs and recent bank statements. Some of the required documents for self-employed individuals with more than 25% ownership are the partner's share of current income, deduction credits; balance sheets; personal and business tax returns. Underwriters will authenticate the employment history and income by speaking with the employer and reviewing recent documentation. Signed consent is required for them to have access to information about their current position, salary, and work history. For loan underwriting, several metrics are used to determine the likelihood of a borrower repaying a loan. A change in employment status can significantly impact the outcome of an application. The underwriting process includes ordering an appraisal for the home intended for purchase, which is always required for home purchases and may be required when refinancing. The purpose of the appraisal is to protect both buyers from overpaying and lenders from loaning more than what the house is worth. The house serves as collateral for the loan, which means that the investor could recover invested capital if the borrower defaults on the loan. Underwriters will check credit history and bills to see how money is managed. They also need to review documents that outline current debt obligations in the form of car payments, student loans, credit card debt, or other liabilities. Even if monthly payments are made on time, a high debt-to-income ratio (DTI) is a warning sign of impending financial difficulty. Insurance companies use medical underwriting to assess a person's risk before providing them with health coverage. They do this by looking at medical history, lifestyle, and demographics. Based on this information, they can estimate how likely the person will need medical care in the future and set premiums accordingly. The medical records are checked to see if there are pre-existing medical conditions at the time of application. If so, there is a higher risk of covering the applicant. The length of time required to assess the risk profile of an investment varies. Underwriting loans and insurance products are typically relatively simple compared to securities. The underwriter's primary responsibility is processing loans and deciding whether to approve or reject an application. Personal and car loans have straightforward underwriting processes. Most often, these types of loans are underwritten by computers using modeling algorithms. But, there is still human interaction in the process. On the other hand, the underwriting process for home loans can be lengthy, taking up to 45 days from start to finish. The underwriter must verify the borrower's creditworthiness and require appraisals for the property and confirmation of home ownership. The process of obtaining life insurance usually spans two to eight weeks. If the company has questions or is waiting on information from a doctor, it may take even longer. A Full Medical Underwriting (FMU) may be required in some cases. It is an in-depth review of the applicant's medical records. The potential policyholder must disclose their complete medical history, which may include years' worth of information. Investment banks take six to nine months to underwrite securities, which are the most complicated products to assess. They do so by examining a company's accounts, assets, cash flows, and liabilities for discrepancies. When a bank uses this process, it relies on multiple underwriters who can help evaluate risk, plan for, and execute the agreement to underwrite an IPO and sell securities. Taking a few preparatory measures can ensure a smoother underwriting process and avoid potential roadblocks to approval. Prepare Bank Statements: Be sure to have at least 60 days of bank statements ready for underwriters when at the start of the loan application process. If the money to be used is outside the applicant's bank account, depositing it a few months before applying for the loan is recommended. Pay Taxes: Although owing taxes does not necessarily make one ineligible for a loan, it can create obstacles that slow down the process. For example, underwriters usually request tax return transcripts from the IRS to check if a client owes money and if there is a payment plan. Settle Loan Balances: Before starting a loan application, pay existing loan balances in full. If not possible, prove to the underwriter that one has enough assets to pay it. If one is already repaying the balance, give the underwriter at least three months' worth of repayment receipts. Address Possible Red Flags: If something in the financial history could be a red flag, address it upfront with the underwriter. Being open about the current situation can help create a positive experience overall. Risk and value are fundamental to underwriting. The function of the underwriter is critical in reducing or eliminating financial risks related to debts, insurance and securities. For loans, the borrower may not repay the loan or stay caught up on the interest payments. For insurance, premiums must account for the potential of numerous policyholders filing claims simultaneously. When securities are involved, underwriters must be concerned about whether or not the investment will make a profit. It is reasonable to have some form of compensation for the risks taken. Without a risk assessment, all financial transactions are educated guesses. Underwriting is based on a process that benefits both the lender or insurer and the borrower or insured.What Is Underwriting?

Types of Underwriting

Loan Underwriting

Insurance Underwriting

Securities Underwriting

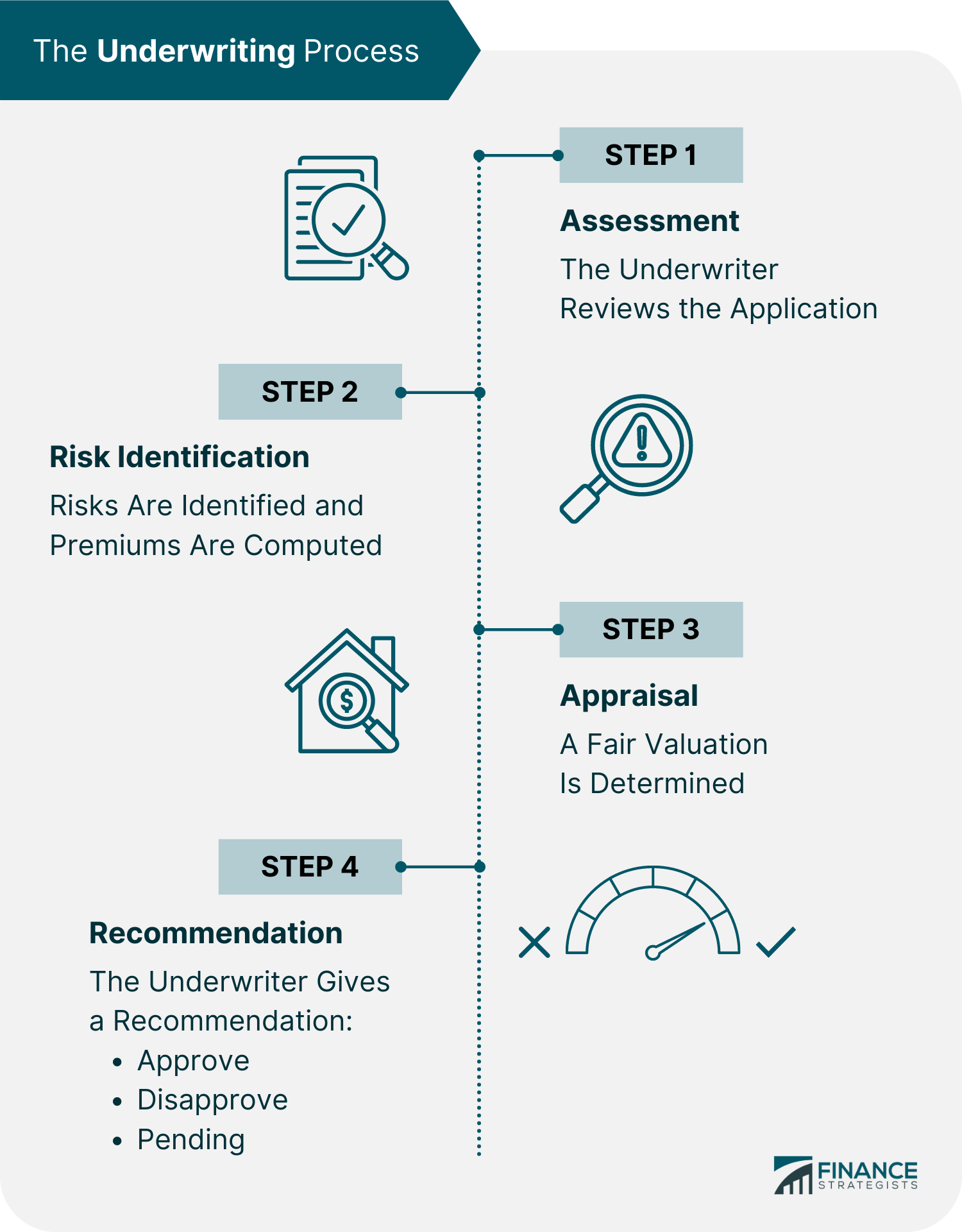

The Underwriting Process

Step 1: Assessment

Step 2: Risk Identification

Step 3: Appraisal

Step 4: Recommendation

Information Needed in Underwriting

Income

Employment Status

Assets and Liabilities

Credit History & Credit Rating

Medical History

How Long Does Underwriting Take?

Loans

Life Insurance

Securities

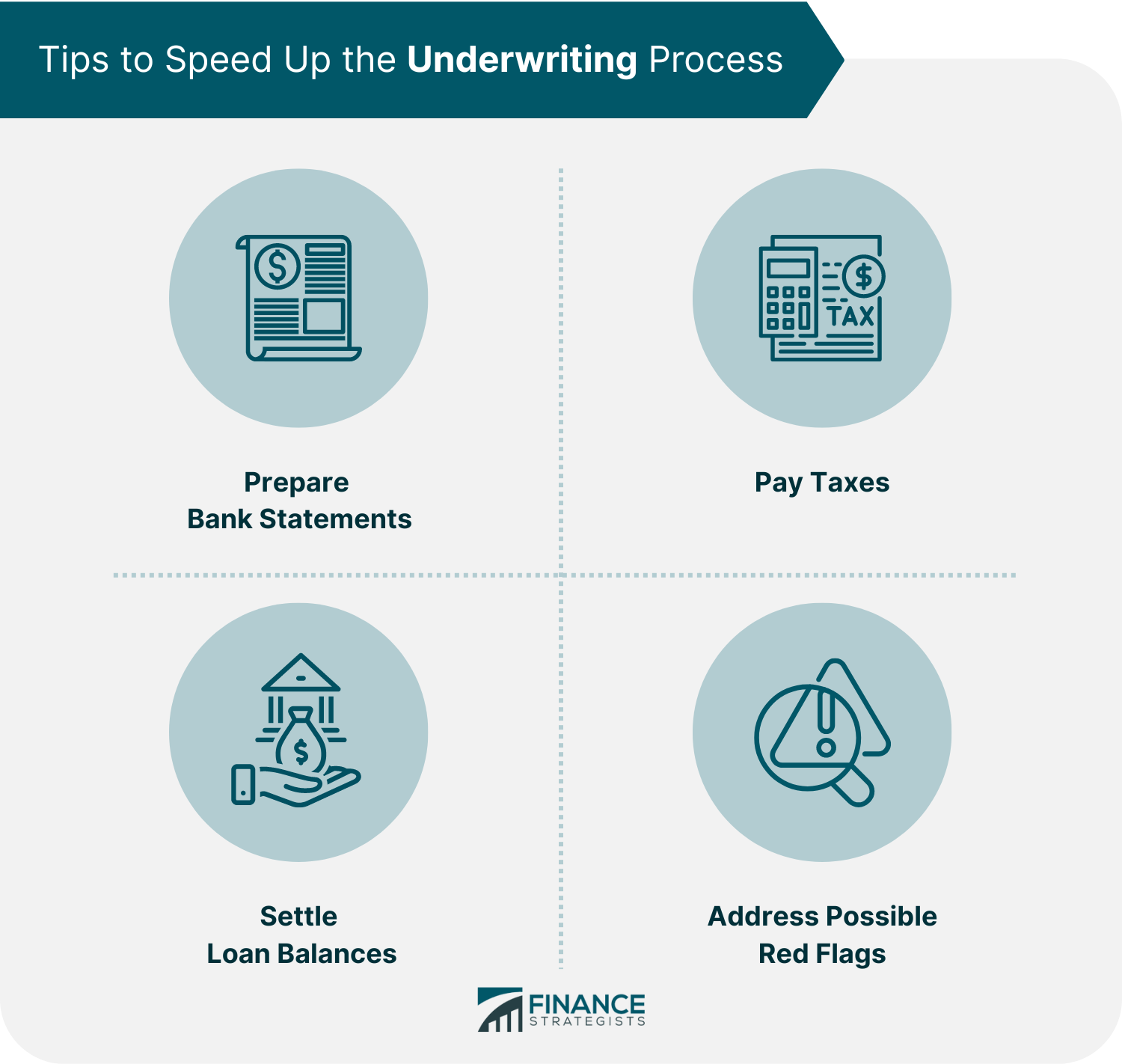

Tips to Speed Up The Underwriting Process

Final Thoughts

Underwriting FAQs

The amount of time required for underwriting varies depending on the investment product. Personal, mortgage and insurance loans take up to 45 days to accomplish. Due to the complexity of the securities underwriting process, it takes six to nine months to complete.

Underwriting is the evaluation process that individuals or organizations undertake before taking on financial risk in exchange for a fee. This typically involves loaning money, investing, or insuring against loss.

The types of underwriting are loans for the release of loan and mortgage applications, insurance for the issuance of policies, and securities for valuing companies going public.

The underwriter will look at credit history, financial records, and the value of the loan collateral. Before issuing an insurance policy, insurance underwriting verifies eligibility for coverage by investigating medical risks. A medical exam and the results of laboratory tests may be required. The financial risks of a firm going public are thoroughly analyzed in the case of securities.

Underwriting could fail for a variety of reasons, such as red flags on credit report, high outstanding debts, not enough money for a downpayment, or damage to the property. If any of these are detected by underwriters, they will likely disapprove the transaction.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.