Yes, you can make contributions to a Rollover IRA, similar to how you would with a Traditional or Roth IRA. A Rollover IRA is primarily designed to receive funds from another qualified retirement plan, such as a 401(k) or a 403(b), when you change jobs or retire. These transfers, called "rollovers," maintain the tax-deferred status of your retirement funds, ensuring that you're not immediately taxed on the moved amount. While it's possible to contribute, there are certain considerations to bear in mind. Firstly, the total amount you can contribute to all your IRAs in a year is subject to federal limits, which can change annually. It's also essential to consider the source of your funds; mixing pre-tax and post-tax assets in a single Rollover IRA can complicate things, especially when taking distributions or performing future rollovers. As with all financial decisions, it's crucial to be informed, and consulting with a financial advisor can provide clarity and direction on making the right choices for your retirement planning. When discussing contributions to a Rollover IRA, it's important to delineate between the different kinds of contributions that can be made. The maximum amount you can contribute across all types of IRAs (Traditional, Roth, and Rollover) is $7,500 ($7,000 in 2025). Remember, this is an aggregate limit. Funds transferred from another qualified retirement plan (like a 401(k) or 403(b)) into a Rollover IRA are not confined by these annual limits. This allows you to rollover the full balance from another retirement account, regardless of the amount, without it impinging on your typical annual contribution room. Individuals who are 50 years old and above have the privilege of adding more to their IRAs beyond the standard limit. This is designed to help those nearing retirement age beef up their savings. For 2026, the catch-up contribution is set at $1,100 ($1,000 in 2025). This means that individuals aged 50 and above can contribute a total of $8,600 to their IRAs. If you have assets in a Traditional IRA, you might decide to convert these funds to a Roth IRA. This process involves paying taxes on the pre-tax amount converted. Once in the Roth IRA, the funds can grow tax-free, and qualified distributions are also tax-free. While this isn't a contribution in the traditional sense, it's a movement of funds between account types and is worth noting in the context of Rollover IRAs, especially if you're considering rolling over assets to a Roth Rollover IRA. To make informed decisions, understanding the implications of tax deductions, the nature of your contributions, and proper reporting is essential. Contributions to these accounts can be tax-deductible, meaning they reduce your taxable income for the year you make the contribution. The exact amount you can deduct depends on various factors including your filing status, whether you (or your spouse) are covered by a retirement plan at work, and your modified adjusted gross income (MAGI). Contributions are made with after-tax money, so they are not tax-deductible. However, the advantage is that qualified distributions in retirement are tax-free. These are made before taxes are taken out of your income. In Traditional and Rollover IRAs, they reduce your taxable income for the year, possibly leading to a lower tax bill. When you withdraw the money in retirement, you'll pay ordinary income tax on both the contributions and their earnings. Common in Roth IRAs, these are amounts you've already paid tax on. Since you've paid the taxes upfront, qualified withdrawals from a Roth IRA (both contributions and earnings) are tax-free. Some individuals also make post-tax contributions to Traditional IRAs, especially when they exceed income limits for a deduction; this sets the stage for a potential "backdoor Roth IRA" conversion in the future. Documenting Deductions: If you make tax-deductible contributions to a Traditional or Rollover IRA, you'll need to report these on your tax return to claim the deduction. This is typically done on Form 1040 or 1040A. Form 5498: Your IRA custodian will send you this form, which shows the total contributions made to your IRA for the year. Roth IRA Reporting: Even though Roth IRA contributions aren't deductible, it's still essential to report them. This establishes the basis for potential non-taxable distributions in the future. Being mindful of the pitfalls and seeking guidance from financial professionals can aid in a smoother and more beneficial management of Rollover IRAs. Over-Contribution: If you deposit more than the allowed amount across your IRAs, you could face a 6% excess contribution penalty on the over-contributed amount each year until the error is rectified. Mixing Pre-Tax and Post-Tax Assets: Combining funds that haven't been taxed with post-tax funds in a single Rollover IRA can make future tax calculations challenging. Required Minimum Distributions (RMDs): If your Rollover IRA contains pre-tax money, you must start taking RMDs when you turn 73. Neglecting this can result in a penalty, which can be 50% of the amount you were supposed to withdraw. Improper Rollover Execution: When rolling over funds from an employer-sponsored plan to an IRA, it's advisable to perform a "direct" or "trustee-to-trustee" transfer. Overlooking Beneficiary Designations: Neglecting this can lead to unintended distribution of assets upon your death, potentially resulting in unfavorable tax consequences for your heirs and bypassing your estate planning intentions. While Rollover IRAs offer numerous advantages, it's essential to consider the individual features of your existing retirement accounts before initiating a rollover. One of the primary advantages of a Rollover IRA is the ability to consolidate various retirement accounts into one. This is especially beneficial for individuals who have switched jobs multiple times and have accumulated different employer-sponsored retirement accounts. By rolling these into one IRA, it streamlines management, reduces paperwork, and provides a clearer picture of total retirement savings. Rollover IRAs, especially those held at major brokerage firms, often offer a wider range of investment options compared to typical employer-sponsored plans. This flexibility allows individuals to diversify their portfolio more effectively, choose specific investments that align with their risk tolerance and financial goals, and potentially reduce costs. Funds in a Rollover IRA continue to grow tax-deferred, similar to the benefits in most employer-sponsored plans. This means you won't pay taxes on dividends, interest, or capital gains until you start taking distributions, allowing your money to compound and grow more efficiently over time. With a Rollover IRA, once you reach the age where RMDs are mandated, you might have more strategic flexibility in terms of which accounts to withdraw from first. This can be beneficial for tax planning and extending the longevity of your retirement assets. In many states, IRAs offer protection from creditors in the event of bankruptcy. While the level of protection can vary based on state laws and the specific circumstances, having funds in a Rollover IRA can provide an added layer of financial security. Contributing to a Rollover IRA presents a valuable opportunity for effective retirement planning. This versatile retirement account accommodates both rollover contributions from other qualified retirement plans and regular contributions, offering individuals options for growing their savings. Annual contribution limits apply to traditional IRAs, Roth IRAs, and Rollover IRAs, with rollovers having no annual cap. Tax implications differ based on contribution type, pre-tax or post-tax nature, and reporting requirements. To avoid potential pitfalls, such as excess contributions and improper rollovers, seeking professional advice is crucial. The advantages of a Rollover IRA encompass streamlined account consolidation, diverse investment choices, tax-deferred growth potential, strategic withdrawal flexibility, and creditor protection in certain cases. By understanding the implications and leveraging benefits, individuals can effectively navigate their retirement journey with a Rollover IRA as a cornerstone of their financial strategy.Can You Make a Contribution to a Rollover IRA?

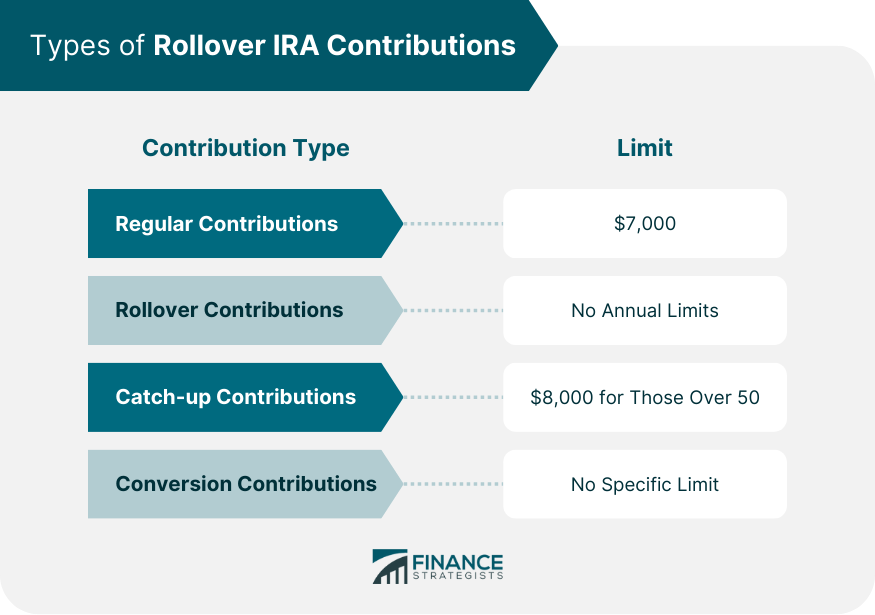

Types of Rollover IRA Contributions

Regular Contributions

Rollover Contributions

Catch-up Contributions

Conversion Contributions

Tax Implications

Tax Deductions for Contributions

Traditional and Rollover IRAs

Roth IRAs

Pre-Tax and Post-Tax Contributions

Pre-Tax Contributions

Post-Tax Contributions

Reporting Contributions on Annual Tax Returns

While you don't submit this form with your tax return, it's a crucial document for your records and ensures that your contributions align with what the custodian reported to the Internal Revenue Service.Potential Pitfalls and Mistakes

This mixture can complicate matters when taking distributions or if considering a conversion to a Roth IRA.

If you take possession of the funds (indirect rollover) and don't deposit them into the Rollover IRA within 60 days, the distribution can be considered taxable, and you might also incur a 10% early withdrawal penalty if you're under 59½.

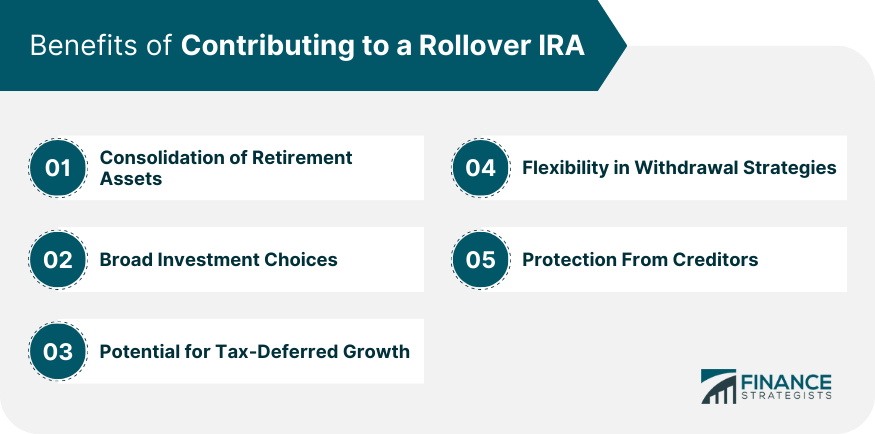

Benefits of Rollover IRA Contribution

Consolidation of Retirement Assets

Broad Investment Choices

Potential for Tax-Deferred Growth

Flexibility in Withdrawal Strategies

Protection From Creditors

Conclusion

Can You Make a Contribution to a Rollover IRA? FAQs

A Rollover IRA is a retirement account designed to receive funds from qualified plans like 401(k)s or 403(b)s when changing jobs or retiring. It maintains tax-deferred status for transferred funds.

You can contribute through rollovers from other retirement plans or regular contributions, subject to annual limits. Rollover contributions aren't restricted by these limits.

Contributions can be tax-deductible in Traditional and Rollover IRAs, reducing taxable income. Roth IRAs use after-tax contributions, with tax-free withdrawals in retirement.

Avoid over-contributing beyond annual limits, mixing pre-tax and post-tax assets, missing required minimum distributions (RMDs), and improper rollover execution.

Rollover IRAs offer consolidation of retirement accounts, diverse investment choices, tax-deferred growth, withdrawal flexibility, and potential creditor protection, enhancing your retirement planning strategy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.