Transferring money from an IRA to a 403(b) plan, mainly for public workers and some non-profit employees, is simpler than it seems. This move keeps the tax benefits and can help organize retirement savings better. The motives are diverse and profound. Rolling over an IRA to a 403(b) is usually driven by the desire to consolidate assets, gain access to different investment options, or leverage particular features of the 403(b) framework. From a broader perspective, such a move can simplify the retirement savings landscape for an individual. Fewer accounts often mean less hassle in management, potentially lower fees, and a clearer path to achieving retirement goals.

Beginning the rollover starts with a request. To move assets out of an IRA, the account holder must request a distribution form from their IRA custodian. This document kickstarts the transfer process, signaling the custodian's intent to move funds. However, it's crucial to be clear about the destination. Mistakes or ambiguities can lead to unnecessary taxes or penalties, and careful attention to detail during this phase is paramount. Determining how much to transfer is a significant step. While some might opt for a complete rollover, others might choose partial transfers, depending on their financial strategy or needs. There are nuances to consider, such as potential tax implications or the specific rules of the receiving 403(b) plan. Each decision here forms the foundation for the next steps. Careful deliberation, potentially with the guidance of a financial advisor, can help in making informed choices. Upon deciding the transfer amount, the next move is ensuring the receiving 403(b) plan is ready. Completing the acceptance form of the 403(b) plan indicates to the new custodian about the incoming funds, smoothing the transition. Remember, each institution might have unique requirements or processes. Being diligent and proactive in gathering and submitting all necessary documents can expedite the process and reduce the likelihood of hiccups. The IRS, ever watchful, has set forth specific criteria governing which funds can be rolled over. Not all distributions from an IRA are eligible for a rollover to a 403(b). These regulations ensure the integrity and intention of retirement savings. Staying abreast of these rules is critical. Missteps can result in unexpected tax bills or penalties, undermining the very financial stability one aims to achieve. While flexibility is a hallmark of retirement savings, there are boundaries. The IRS mandates that only one IRA-to-IRA or IRA-to-403(b) rollover can occur in a 12-month period. This rule ensures individuals don't exploit the system, maintaining fairness. Such a restriction might seem stringent, but it's in place to guard against potential misuse. It also nudges individuals to deliberate thoroughly before making transfer decisions. Age doesn't just bring wisdom; it brings RMDs. Once individuals reach a specific age, they're required to withdraw a minimum amount from their retirement accounts annually. Importantly, these distributions are not eligible for rollover. This rule underscores the dual purpose of retirement accounts: to provide for retirement and ensure these funds are eventually distributed and taxed. Strategic planning can help optimize both the timing and amount of these distributions. Tax efficiency is paramount when dealing with retirement funds. There are two main types of rollovers: direct and indirect. In a direct rollover, funds move directly between financial institutions. In contrast, an indirect rollover involves the distribution being paid to the account holder, who then has 60 days to deposit it into the new account. While the latter offers some flexibility, it's fraught with risks. Any misstep or delay beyond 60 days can lead to taxation and potential penalties, eroding hard-earned savings. A pitfall many inadvertently fall into is the withholding trap during an indirect rollover. By default, custodians withhold 20% of the distribution for federal taxes. If the account holder doesn't deposit the full amount (including the withheld 20%) into the 403(b) within 60 days, the withheld portion is considered a taxable distribution. Such nuances highlight the labyrinthine nature of tax laws and the importance of being well-informed or seeking expert guidance during the rollover process. Complexities abound, especially when considering the tax treatment of after-tax contributions in an IRA. When these funds are rolled over to a 403(b), they carry unique tax implications. Generally, the earnings on after-tax contributions are tax-deferred until withdrawal, but the initial contributions are tax-free. This layered treatment underscores the advantage of meticulous record-keeping. Knowing the composition of your retirement funds can lead to more strategic and tax-efficient decisions. A rollover isn't merely a transactional event. It's an opportunity to revisit and potentially recalibrate one's investment strategy. As funds transition to a 403(b), it's crucial to ensure the new asset allocation aligns with the individual's financial goals and risk tolerance. Life's dynamism means financial goals evolve. Regular check-ins on asset allocation, especially during significant events like a rollover, can keep one's retirement strategy on the right track. Every financial institution and plan offers a unique suite of investment options. Rolling funds into a 403(b) plan necessitates a deep dive into these options, ensuring they meet the investor's needs and preferences. It's not just about returns. Factors like fees, fund management, and historical performance play pivotal roles in decision-making. An informed choice here can set the stage for years of fruitful growth. Diversification is a cornerstone of investment wisdom. When transitioning funds, it's a prime time to spot any potential gaps or overlaps in asset classes. Such redundancies or omissions can skew the risk profile of the portfolio. Being astute in this phase can lead to a well-rounded and resilient portfolio, poised to weather market volatilities and capitalize on growth opportunities. In a world of instant gratification, rollovers can test patience. Delays often arise from timing mismatches between the sending IRA and receiving 403(b) institutions. While some are quick, others might take their time, leading to anxious waiting periods. Understanding the typical timelines of both institutions can set realistic expectations. Patience, coupled with proactive communication, can mitigate most timing-related anxieties. Bureaucracy's favorite child, paperwork, is often the culprit behind rollover delays. Incomplete or incorrect documentation can halt the process, leading to back-and-forths that consume time and energy. Vigilance is the antidote. Ensuring all documents are meticulously filled, cross-checking details, and maintaining copies can streamline the process, preventing unnecessary hiccups. Silence isn't golden in the world of financial transfers. Active communication with both the sending and receiving institutions can make the difference between a smooth rollover and a protracted ordeal. It's more than just making calls. Seeking regular updates, clarifying doubts promptly, and building rapport with point-of-contact personnel can facilitate a seamless transfer, ensuring funds land safely in their new home. Transitions come with clarity. By rolling over an IRA into a 403(b), individuals merge their scattered retirement assets into a unified platform. This consolidation not only reduces the hassle of managing multiple accounts but also provides a holistic view of one's retirement nest egg. Such clarity amplifies decision-making power. With assets under one umbrella, individuals can better track performance, reassess goals, and make timely adjustments, ultimately bolstering their financial future. Not all retirement plans are created equal. A significant lure of 403(b) plans is their array of investment options, which can often outpace those found in traditional IRAs. By transitioning to a 403(b), individuals may access a broader, or sometimes, more specialized set of investments tailored to their sector. Beyond sheer variety, the quality of options matters. Better fund performances, more advanced financial instruments, or niche investments aligned with one's profession can be game-changers, driving growth and long-term stability. Less is often more, especially in financial management. With an IRA rollover to 403(b), the complexities of juggling multiple accounts melt away, ushering in a streamlined approach to retirement savings. The beauty of simplicity cannot be overstated. A singular account means a single set of statements, one login, one helpline, and one strategy to review. This efficient structure can alleviate stress, save time, and enhance the focus on investment strategies. One of the standout jewels in the rollover crown is tax advantage. By rolling over an IRA into a 403(b), individuals can extend the tax-deferred growth of their savings, only facing taxes upon withdrawal. Tax deferral is more than a delay—it's a growth strategy. By postponing taxes, the invested funds compound over time, potentially leading to significant increases in value. It's a play on time, where every deferred tax dollar works harder, aiming for a richer retirement. Ironically, while 403(b) plans might offer enticing investment options, they can also come with limitations. Unlike the vast universe of IRA investments, 403(b) plans might have a restricted set of choices, potentially hindering diversification or personal preferences. These constraints can sometimes stifle growth or flexibility. Without the desired asset classes or funds, investors might feel pigeonholed, unable to craft their ideal portfolio. Hidden in the fine print, fees and charges can eat into retirement savings. 403(b) plans, especially those with richer offerings, might come with higher administrative fees or specific fund charges compared to traditional IRAs. These costs, though they might seem minor, can compound over time. Over the years, they can significantly erode the value of investments, detracting from the overall returns. Liquidity, the ability to access funds, is crucial. 403(b) plans, while advantageous in many ways, can sometimes impose stricter withdrawal restrictions than IRAs. These can range from age-related constraints to penalties for early withdrawals. Such limitations can pose challenges, especially in unexpected financial emergencies. It underscores the importance of understanding the fine print and planning withdrawals strategically. With greater power comes greater responsibility, and in the realm of 403(b)s, this translates to intricate record-keeping. Given the myriad rules, potential loans against the account, and specific employer-related nuances, managing a 403(b) can be a detailed affair. Accuracy in this domain is paramount. Errors or oversights can lead to unexpected tax implications or compliance issues, emphasizing the need for diligence. Life's ebb and flow can lead to shifts in professional paths. A change in employment, especially transitioning to sectors that predominantly offer 403(b) plans, can make an IRA rollover a viable option. Such transitions can be both exciting and daunting. While new roles or sectors offer growth, they also require recalibration of financial strategies, making rollovers an integral part of the process. A mosaic of retirement accounts can be a logistical challenge. For those juggling multiple IRAs, 401(k)s, or other retirement savings, the allure of consolidation under a 403(b) banner becomes palpable. Such a move is not merely about ease but about power. A consolidated view amplifies understanding, streamlines strategy, and can lead to better financial outcomes. Some sectors, like non-profit or education, are intrinsically linked with 403(b) plans. As professionals transition into these areas, rolling over their existing IRA becomes a strategic move, aligning their savings with the sector's predominant financial vehicle. Beyond alignment, this transition can also offer specialized investment options or benefits tailored to these sectors, enhancing the value proposition. Sometimes, the pull of a 403(b) is purely financial. The desire to tap into specific investment options, unavailable in traditional IRAs, can drive the rollover decision. Whether it's a high-performing fund, a niche investment related to one's profession, or a unique financial instrument, the quest for better returns can make a 403(b) rollover a tantalizing prospect. Navigating the maze of financial decisions can be daunting. Here's where financial advisors, with their expertise and experience, shine. When considering a rollover, their insights can be invaluable, helping make informed decisions. An adept advisor can illuminate the pros and cons, tailor strategies, and guide individuals through the process, ensuring the rollover aligns with long-term financial goals. In the financial realm, details matter. Every document, every clause, every term has implications. Hence, diving deep into the fine print before initiating a rollover is essential. Such understanding can unveil hidden charges, highlight restrictions, or even reveal benefits, ensuring individuals make a move with eyes wide open, primed for success. The distinction between direct and indirect rollovers is more than semantics—it's about tax implications. Direct rollovers, where funds move seamlessly between institutions without passing through the individual's hands, are usually the preferred route. Opting for direct transfers not only simplifies the process but also avoids potential tax withholdings or penalties. It's a smoother, more efficient path to transitioning funds. Trust, but verify. Once the rollover ball is set rolling, monitoring the transfer becomes paramount. Tracking the movement, ensuring timely execution, and verifying the receipt of funds can avert potential glitches. In the digital age, most institutions offer online tracking, making it easier for individuals to keep a watchful eye. This vigilance ensures that hard-earned retirement savings transition without a hitch, setting the stage for future growth. Navigating the process of an IRA rollover to a 403(b) is a strategic move many consider to optimize their retirement assets. For public workers and some non-profit employees, this transition offers numerous benefits like consolidating retirement assets, accessing potentially superior investment options, simplifying account management, and extending tax deferrals. However, it doesn't come without its pitfalls. Challenges such as limitations on investment choices, fees, withdrawal restrictions, and record-keeping complexities can arise. Key to a successful rollover is understanding the intricate rules, such as IRS limitations, frequency restrictions, and tax implications. Ensuring continuity in investment strategy, recognizing asset gaps, and addressing potential delays are crucial. Consulting with financial advisors, understanding the details, and monitoring the process are paramount. Thus, while an IRA rollover to a 403(b) can streamline one's retirement savings journey, it's a decision that demands thorough understanding and meticulous planning.Understanding IRA Rollover to 403(b)

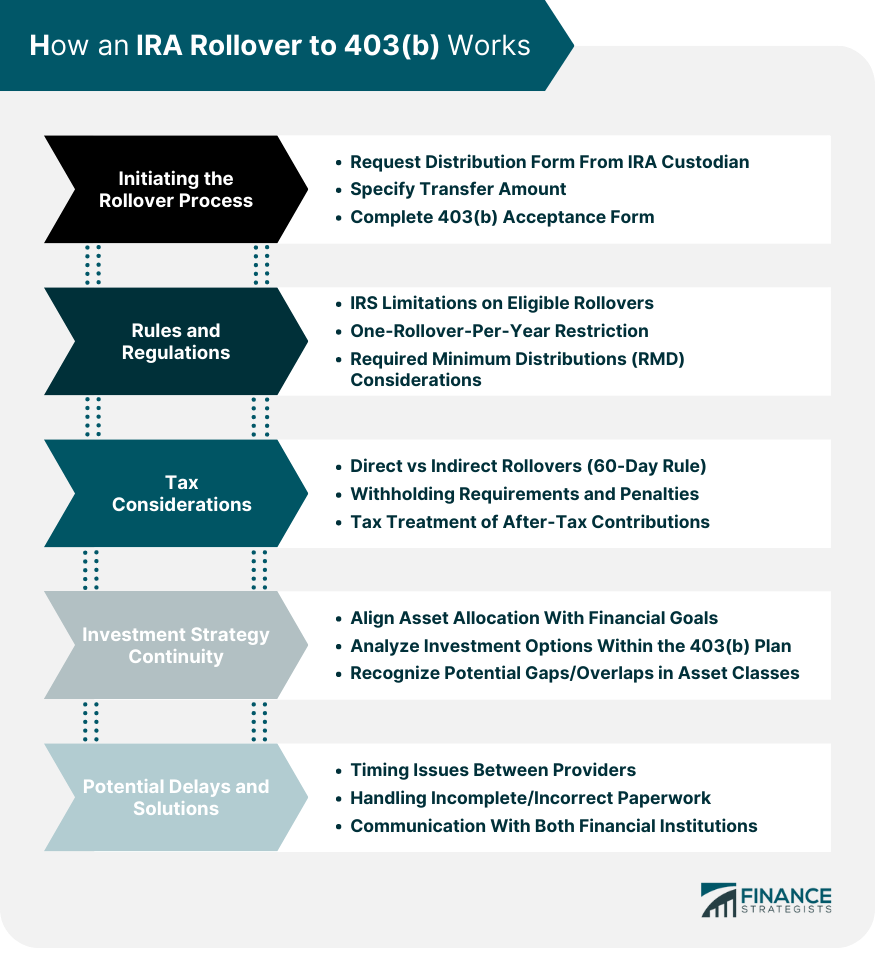

How an IRA Rollover to 403(b) Works

Initiating the Rollover Process

Request a Distribution Form From IRA Custodian

Specify the Transfer Amount

Complete the 403(b) Plan’s Acceptance Form

Rules and Regulations to Note

IRS Limitations on Eligible Rollovers

Frequency Restrictions (One-Rollover-Per-Year Rule)

Required Minimum Distributions (RMD) Considerations

Tax Considerations

Direct vs Indirect Rollovers: The 60-day Rule

Withholding Requirements and Penalties

Tax Treatment of After-Tax Contributions

Ensuring Continuity in Investment Strategy

Align Asset Allocation With Financial Goals

Analyze the Investment Options Within the 403(b) Plan

Recognize Potential Gaps or Overlaps in Asset Classes

Potential Delays and Solutions

Timing Issues Between the IRA and 403(b) Providers

Handling Incomplete or Incorrect Paperwork

Communicating With Both Financial Institutions to Ensure Seamless Transfer

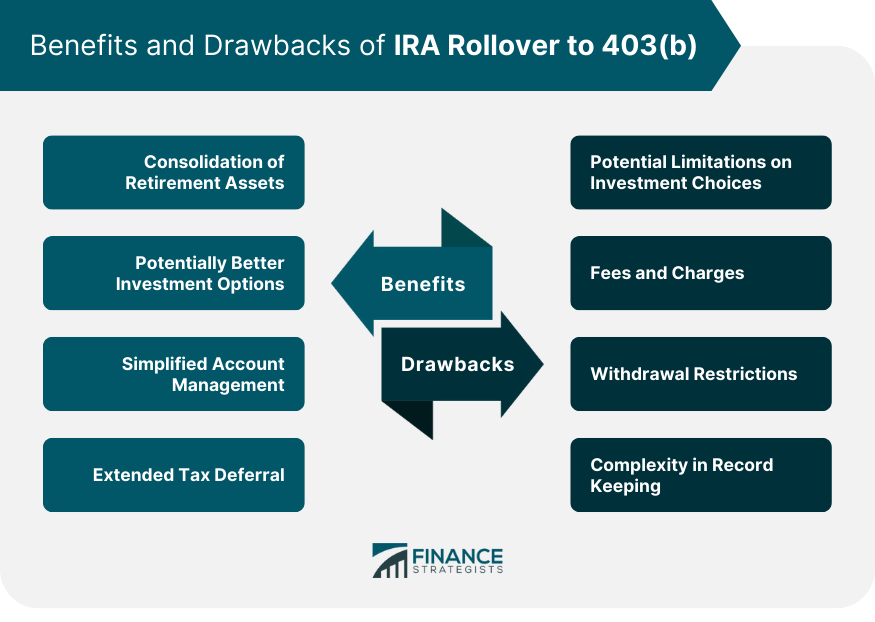

Benefits of IRA Rollover to 403(b)

Consolidation of Retirement Assets

Potentially Better Investment Options

Simplified Account Management

Extended Tax Deferral

Drawbacks of IRA Rollover to 403(b)

Potential Limitations on Investment Choices

Fees and Charges

Withdrawal Restrictions

Complexity in Record Keeping

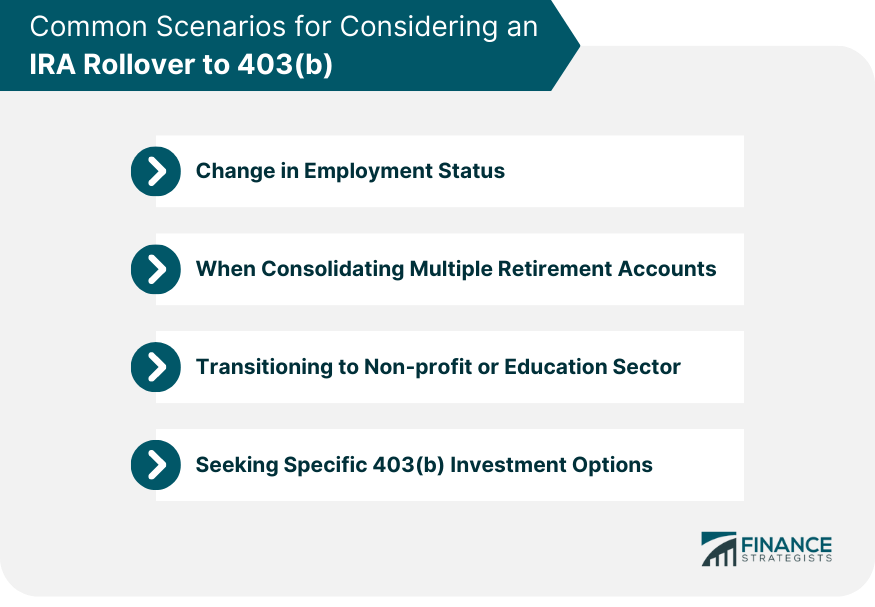

Common Scenarios for Considering an IRA Rollover to 403(b)

Change in Employment Status

When Consolidating Multiple Retirement Accounts

Transitioning to Non-profit or Education Sector

Seeking Specific 403(b) Investment Options

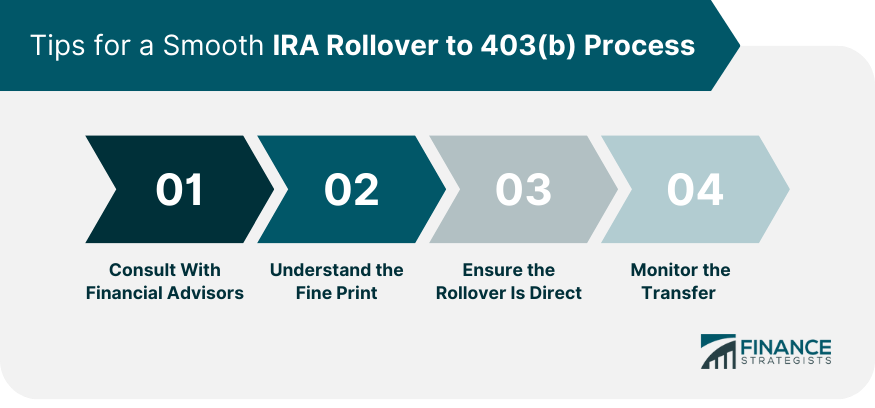

Tips for a Smooth IRA Rollover to 403(b) Process

Consult With Financial Advisors

Understand the Fine Print

Ensure the Rollover Is Direct

Monitor the Transfer

Bottom Line

IRA Rollover to 403(b) FAQs

It's a process where funds from an IRA are moved to a 403(b) plan, offering consolidation and potentially better investment options.

Yes, rolling over can extend the tax-deferred growth of your savings, with taxes only due upon withdrawal.

Potential issues include investment limitations, higher fees, withdrawal restrictions, and complexities in record-keeping.

Reasons include changing employment, consolidating multiple accounts, transitioning to the non-profit sector, or seeking specific 403(b) investments.

Consult financial advisors, understand all terms, ensure a direct rollover, and closely monitor the transfer for any discrepancies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.