IRA withdrawal rules are designed with the intent to preserve funds for retirement, which is why there are specific guidelines and penalties for early withdrawals. Generally, funds can be withdrawn penalty-free after the age of 59½. However, withdrawals before this age can lead to a 10% federal penalty tax on top of regular income taxes, making early withdrawals a potentially costly decision. The rules also mandate that for Traditional IRAs, holders must start taking required minimum distributions (RMDs) at age 72 (73 if you reach age 72 after Dec. 31, 2022), ensuring that the retirement funds are used for their intended purpose. Understanding these rules is essential for anyone who owns an IRA, as it affects how they plan their retirement and manage their funds. Early withdrawals can disrupt the growth trajectory of these retirement funds and result in a financial setback. Early withdrawal from an IRA is defined as any distribution of funds taken before the account holder reaches 59½ years of age. Such withdrawals are subject to both taxes and penalties, except in specific circumstances outlined by the IRS. This definition is crucial for investors to comprehend, as it sets the stage for a disciplined approach to retirement savings and emphasizes the long-term nature of these investment vehicles. The rationale behind penalizing early withdrawals is to discourage the use of these retirement savings for non-retirement expenses. The government's aim is to secure individuals' financial stability during retirement, and penalties are a tool to maintain the sanctity of these funds for their intended use. The circumstances leading to penalties are primarily centered around the age of the account holder and the reasons for withdrawal. Any non-qualified distribution is typically subject to a 10% penalty. The penalty is a financial disincentive designed to deter individuals from undermining their retirement savings. Exceptions to these penalties are made for specific situations, like purchasing a first home or paying for medical expenses, which are recognized by the IRS as legitimate needs that may require early access to IRA funds. Understanding these circumstances can help individuals navigate their financial options without compromising their retirement savings unnecessarily. Calculating the early withdrawal penalty involves identifying the taxable amount of the distribution and applying a 10% penalty on it. This penalty is in addition to the regular income tax owed on the withdrawal, which can push the account holder into a higher tax bracket, thereby increasing their overall tax liability for the year. To illustrate, if an individual in the 25% tax bracket takes an early distribution of $10,000, they would owe $2,500 in income taxes plus a $1,000 penalty, totaling $3,500 in taxes and penalties. This significant financial impact highlights the importance of planning and caution when considering an early withdrawal from an IRA. Consider the example of a 40-year-old individual who decides to withdraw $20,000 from their IRA to cover unexpected medical bills. Without qualifying for an exception, the individual would face a $2,000 penalty plus income taxes on the full amount, which could reduce the final amount received by nearly a third, depending on their tax bracket. Another scenario might involve a 35-year-old taking an early IRA withdrawal to fund a child's college education. While this decision might seem justified, it comes with a steep financial cost in the form of penalties and taxes, which could be mitigated by exploring other financing options such as education loans or scholarships. These examples serve to illustrate the potentially adverse financial consequences of early IRA withdrawals. The IRS provides a list of exceptions that allow for penalty-free early withdrawals from an IRA. These exceptions include but are not limited to, expenses for higher education, unreimbursed medical expenses, disability, and a first-time home purchase. It is important for IRA holders to familiarize themselves with these exceptions to avoid unnecessary penalties. Each exception is carefully defined by the IRS to prevent abuse and to guide IRA holders in understanding their options. For instance, the first-time homebuyer exception allows an individual to withdraw up to $10,000 without penalties, but it must be used for qualifying home purchase expenses. Each exception to the early withdrawal penalty has its nuances. For example, the higher education expense exception applies to the IRA owner, their spouse, or the children and grandchildren of the owner. The funds can be used for tuition, fees, books, supplies, and sometimes room and board for students enrolled at least half-time. The disability exception requires a physician's confirmation that the condition is total and permanent, preventing gainful activity. This underscores the importance of understanding the details of each exception to ensure compliance and to legitimately access funds when needed. Proper documentation is paramount to qualify for an early withdrawal penalty exception. This documentation varies depending on the exception but typically includes receipts, bills, and sometimes detailed explanations of the circumstances that necessitate the withdrawal. For instance, in the case of medical expenses, one must provide proof that the expenses exceed 7.5% of their adjusted gross income. This can be a complex process, and the burden of proof lies with the taxpayer to validate their claim for an exception. When an individual takes an early withdrawal from their IRA, it's not just the 10% penalty that affects their finances; the distribution also becomes part of their taxable income for the year. This can be particularly burdensome because it could push the individual into a higher tax bracket, increasing their overall tax obligation. The tax implications are immediate, affecting the individual's income tax return for the year of the withdrawal. The money taken out from an IRA is taxed as ordinary income at the account holder's current marginal tax rate. For example, if someone is in the 22% tax bracket and makes an early withdrawal, that money will be taxed at that rate, in addition to any penalties. Reporting early withdrawals on tax filings is a meticulous process. The distribution will be reported on Form 1099-R, which the account custodian sends to both the IRA holder and the IRS. It's crucial for individuals to report this information accurately on their tax return using Form 1040. Failure to report IRA distributions, or reporting them incorrectly, can lead to an audit and additional penalties. It is advisable for IRA holders to seek assistance from tax professionals when reporting early withdrawals to ensure accuracy and compliance with tax laws. There are several strategies an individual can employ to minimize the tax burden of an early IRA withdrawal. If possible, spreading out distributions over multiple years can keep one from moving into a higher tax bracket. Another strategy could be to only take out what is absolutely necessary, reducing the amount of taxable income. Some individuals may also consider converting their Traditional IRA to a Roth IRA, which allows for tax-free withdrawals, though this strategy involves paying taxes on the converted amount. It's a complex decision that requires careful planning and consideration of one's current and future tax situations. Given the complexities of IRA withdrawals and tax implications, consulting with a tax professional is strongly recommended. These professionals can provide tailored advice, helping individuals understand the consequences of an early withdrawal, explore possible exceptions, and develop strategies to minimize taxes. A tax professional can also assist in navigating the various forms and requirements necessary for reporting the distribution. They can ensure that individuals take advantage of all applicable tax laws, potentially saving them a significant amount in taxes and penalties. Some types of IRA accounts may offer loan options, which can be a viable alternative to an early withdrawal. While Traditional IRAs do not allow loans, other retirement plans like 401(k)s or similar employer-sponsored plans often do. Borrowing from a 401(k) can provide temporary financial relief without the tax penalties associated with early IRA withdrawals. However, these loans must be repaid under the terms of the plan to avoid them being counted as a distribution, complete with taxes and penalties. It's crucial for individuals to understand the specifics of their retirement plan's loan features, including repayment terms and interest rates. While this alternative can alleviate immediate financial strain, it also reduces the earning potential of the retirement account until the loan is repaid. Hardship withdrawals are another potential alternative to avoid early withdrawal penalties. These are permitted under certain circumstances, such as immediate and heavy financial need that includes certain medical expenses, tuition and educational fees, and costs related to the purchase of a principal residence. The IRS sets forth specific criteria that must be met for a hardship withdrawal to be considered. It's imperative to note that while hardship withdrawals from an IRA are not subject to the early withdrawal penalty, they are still subject to income taxes. Exploring other financial instruments and savings options can provide alternatives to using retirement funds for immediate needs. For instance, establishing a regular savings account, investing in taxable investment accounts, or contributing to a Health Savings Account (HSA) can offer more liquidity and accessibility. These alternatives can serve as a buffer to prevent tapping into retirement savings prematurely. They can be especially beneficial for younger individuals who have more time to rebuild their savings or for those who may face unexpected financial needs before retirement. Avoiding early withdrawals from an IRA has a significant long-term impact on retirement savings. The power of compounding interest means that the funds left in the account can grow exponentially over time. An early withdrawal not only reduces the principal balance but also the amount of future earnings that the balance could have generated. It's essential for individuals to consider the long-term ramifications of their financial decisions and to seek out alternatives whenever possible. By avoiding early withdrawals, individuals can ensure that their retirement savings are intact and have the potential to grow to their maximum capacity. Consistent and strategic contributions to an IRA are pivotal for building a robust retirement fund. Financial experts often recommend maximizing annual contributions to benefit from tax deductions and compound growth. For instance, making contributions early in the year can potentially yield more growth than end-of-year contributions due to a longer period of compound interest. Another best practice is to diversify investments within the IRA to mitigate risk. This involves spreading the contributions across various asset classes, such as stocks, bonds, and mutual funds, based on individual risk tolerance and retirement timelines. It's also wise to periodically review and adjust contributions based on changes in income, retirement goals, and financial market conditions. Implementing strategies to avoid early withdrawals can safeguard retirement savings. One effective strategy is to build an emergency fund that covers at least three to six months of living expenses. This fund can act as a financial buffer against unexpected costs without needing to tap into the IRA. Additionally, individuals should consider insuring against large potential financial risks, such as health issues or disability, that could otherwise lead to early withdrawals. Long-term insurance plans, for example, can provide coverage in case of chronic illnesses, thereby protecting retirement savings from being depleted for medical costs. Financial planning and advice are invaluable for navigating the complexities of IRA management. A certified financial planner can offer professional guidance tailored to an individual's unique financial situation and goals. They can help in crafting a comprehensive retirement plan, advising on investment choices, and assisting with tax planning. Regularly consulting with a financial advisor can also keep individuals updated on changes in tax laws and retirement policies that might affect their IRA. The advisor can also help reassess and realign retirement strategies in response to life changes, such as a career move, marriage, or the birth of a child. There is a plethora of tools and resources available to assist individuals in managing their IRAs. Online calculators can help project retirement savings growth and plan contributions. Investment tracking software can monitor IRA performance and help in rebalancing the portfolio as needed. In addition to digital tools, many books and publications offer insights into retirement planning and IRA management. Furthermore, the IRS website provides up-to-date information on contribution limits, withdrawal rules, and tax guidelines related to IRAs. Leveraging these tools and resources can empower individuals to take charge of their retirement planning and make informed decisions about their IRA. Navigating the intricacies of IRAs and understanding the ramifications of early withdrawals are critical components of sound retirement planning. The penalties for early withdrawal from an IRA can have a lasting impact on your financial stability, emphasizing the need for strategic planning and disciplined saving. By familiarizing yourself with the exceptions, tax implications, and alternatives to early withdrawals, you can make informed decisions that secure your financial future. Remember, the journey to a comfortable retirement is marred with potential pitfalls, and the guidance of a financial advisor can be instrumental in avoiding them. Proactive management and regular contributions to your IRA, coupled with expert advice, will help ensure that your golden years are as rewarding as they should be. Seeking professional retirement planning services to build and preserve your nest egg is encouraged, ensuring that when it's time to retire, you can do so with peace of mind and financial security.Overview of IRA Withdrawal Rules

Early Withdrawal Penalties of IRAs

Definition of Early Withdrawal

Circumstances Leading to Penalties

Calculation of the Penalty

Examples of Early Withdrawal Scenarios

Exceptions to Early Withdrawal Penalties of IRAs

List of Qualifying Exceptions

Detailed Explanation of Each Exception

Documentation and Proof Requirements

Tax Implications of Early Withdrawals in IRAs

Income Tax on Early Withdrawals

Reporting Early Withdrawals in Tax Filings

Strategies to Minimize Tax Liabilities

Consultation With Tax Professionals

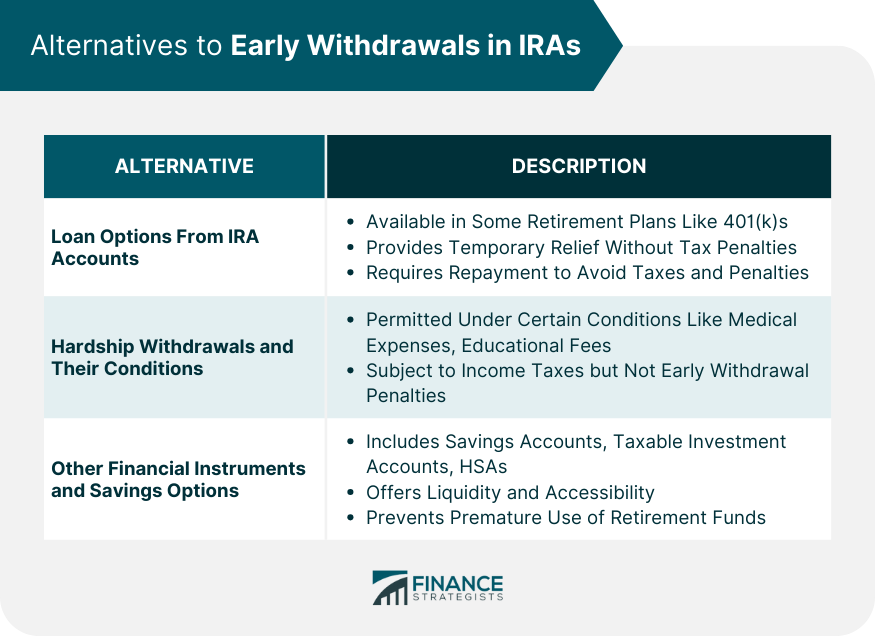

Alternatives to Early Withdrawals in IRAs

Loan Options From IRA Accounts

Hardship Withdrawals and Their Conditions

Other Financial Instruments and Savings Options

Long-Term Impact of Avoiding Early Withdrawal

Planning and Managing Your IRA to Avoid Early Withdrawal Penalties

Best Practices for IRA Contributions

Strategies for Avoiding Early Withdrawals

Importance of Financial Planning and Advising

Tools and Resources for IRA Management

Final Thoughts

Penalty on Early Withdrawal of IRA FAQs

The penalty for an early IRA withdrawal is typically a 10% federal tax on the amount withdrawn if you are under the age of 59½.

Yes, you can avoid the penalty if you qualify for exceptions such as disability, higher education expenses, or a first-time home purchase.

Early withdrawals are added to your taxable income, potentially pushing you into a higher tax bracket and increasing your tax liability.

Yes, alternatives include taking a loan from a 401(k), hardship withdrawals under specific conditions, or utilizing other savings options.

Retirement planning services can provide expert advice on IRA contributions, tax implications, and strategies to avoid unnecessary early withdrawals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.