Insurance planning is the process of evaluating and managing risks associated with potential losses and taking appropriate measures to mitigate those risks by selecting suitable insurance policies. The aim of insurance planning is to provide financial protection against potential risks and to ensure that an individual, family, or business has adequate insurance coverage to meet their needs. Insurance planning involves assessing potential risks and determining the appropriate types of insurance coverage to protect against those risks. This can include health insurance, life insurance, disability insurance, auto insurance, property insurance, liability insurance, and other types of insurance policies. Insurance planning follows a systematic risk management process, which includes the following steps: Identify Risks: Recognize potential threats to your financial well-being, such as accidents, illness, or property damage. Evaluate Risks: Assess the likelihood and potential impact of each risk. Select Risk Management Technique: Determine whether to retain, transfer, reduce, or avoid each risk. Implement Technique: Implement the chosen risk management strategy, such as purchasing insurance or implementing safety measures. Monitor and Adjust: Periodically review and update your risk management strategies to ensure continued effectiveness. For a valid insurance policy, the policyholder must have an insurable interest in the subject matter of the insurance. This means that the policyholder stands to suffer a financial loss or other negative consequences if the insured event occurs. Insurance operates on the principle of indemnification, which aims to restore the insured to the same financial position they were in before the insured event occurred. Insurance companies rely on the law of large numbers to spread risk across a large group of policyholders. This allows them to predict the likelihood of claims and set appropriate premium levels. Insurance contracts are based on the principle of utmost good faith, which requires both the insurer and insured to act honestly and disclose all relevant information. Life insurance provides financial protection for the insured's beneficiaries in the event of their death. There are several types of life insurance: Term Life Insurance: Provides coverage for a specified term, usually ranging from 10 to 30 years. Whole Life Insurance: Offers lifetime coverage with a guaranteed death benefit and cash value accumulation. Universal Life Insurance: Provides lifetime coverage with flexible premiums and an adjustable death benefit. Variable Life Insurance: Offers lifetime coverage with a death benefit and cash value tied to investment performance. Health insurance helps cover medical expenses and can be obtained through various sources: Individual Health Insurance: Purchased directly by the insured from an insurance company. Group Health Insurance: Offered by employers or other organizations to their members. Government-Sponsored Health Insurance: Programs like Medicare and Medicaid, which provide coverage for specific groups of people. Property and casualty insurance protects against damage to property and liability claims arising from accidents or other incidents: Homeowners Insurance: Covers damage to your home and its contents, as well as liability for injuries to others on your property. Automobile Insurance: Protects against financial loss due to accidents, theft, or damage to your vehicle. Renters Insurance: Covers damage to personal property and liability for injuries to others while renting a living space. Umbrella Liability Insurance: Provides additional liability coverage beyond the limits of other insurance policies. Disability insurance replaces a portion of your income if you become unable to work due to an illness or injury. Long-term care insurance covers the cost of care for individuals who require assistance with daily living activities due to chronic illness, disability, or cognitive impairment. Various factors influence an individual's insurance needs, including: Income and Expenses: Your current and future income, as well as your regular and potential expenses, play a crucial role in determining the amount of insurance coverage required. Financial Goals and Obligations: Insurance planning should consider your long-term financial goals, such as retirement planning, education funding, and debt repayment. Dependents and Beneficiaries: The number and age of your dependents, as well as their financial needs, impact the amount and type of insurance coverage you require. Current Insurance Coverage: Assessing your existing insurance policies can help identify gaps or overlaps in coverage that need to be addressed. There are several approaches to calculate insurance needs: Human Life Value Approach: Estimates the present value of your future earnings to determine the amount of life insurance coverage needed. Needs-Based Approach: Evaluates the specific financial needs of your dependents and beneficiaries to calculate the required life insurance coverage. Capital Retention Approach: Determines the amount of insurance needed to preserve your existing assets for your beneficiaries, without requiring liquidation. When selecting an insurance policy, consider the following features: Premiums: The cost of insurance, which can be paid monthly, quarterly, or annually. Coverage Limits: The maximum amount the insurance company will pay in the event of a claim. Deductibles: The amount you must pay out-of-pocket before the insurance company begins to cover costs. Exclusions: Specific situations or conditions that are not covered by the insurance policy. It's essential to evaluate the insurance company itself to ensure it can meet your needs: Financial Strength: Assess the insurer's financial stability and ability to pay claims. Reputation: Research the insurer's reputation for customer satisfaction, policy offerings, and pricing. Customer Service: Evaluate the company's responsiveness and accessibility for inquiries and claims handling. Claims Handling: Consider the insurer's claims processing efficiency and fairness. Insurance planning strategies can be categorized into four main types: Risk Retention: Accepting and self-insuring the risk, either because the risk is minimal or the cost of insurance is too high. Risk Transfer: Shifting the risk to an insurance company by purchasing an insurance policy. Risk Reduction: Implementing measures to reduce the likelihood or severity of a loss, such as installing safety features or following a healthy lifestyle. Risk Avoidance: Eliminating the risk entirely by not engaging in activities that may result in a loss. Regularly reviewing and monitoring your insurance coverage is crucial to ensure your financial protection: Regular Review of Insurance Coverage: Assess your insurance needs and coverage at least annually or when significant life changes occur. Updating Insurance Coverage Based on Life Events: Adjust your coverage when events such as marriage, divorce, childbirth, or job change take place. Monitoring Insurance Company Performance: Keep track of your insurance company's financial strength, customer service, and claims handling to ensure continued reliability. Insurance planning is an integral part of overall financial planning. It provides essential protection for your assets, health, and well-being. By understanding the principles of insurance, various types of insurance, and strategies for adequate coverage, you can create a comprehensive insurance plan that safeguards your financial future. Regularly review and update your insurance coverage to ensure continued protection as your needs and circumstances change.What Is Insurance Planning?

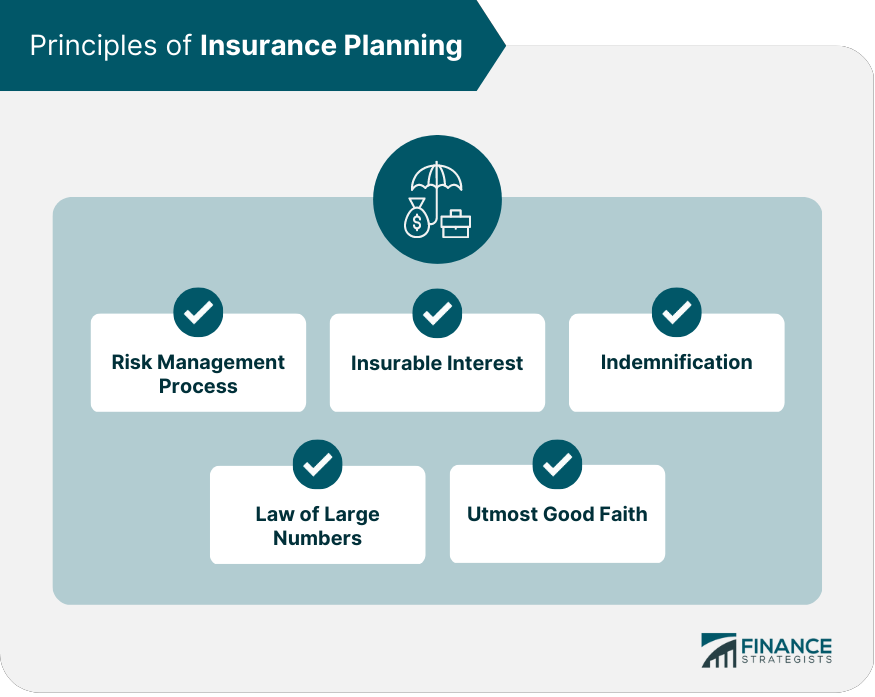

Principles of Insurance Planning

Risk Management Process

Insurable Interest

Indemnification

Law of Large Numbers

Utmost Good Faith

Types of Insurance

Life Insurance

Health Insurance

Property and Casualty Insurance

Disability Insurance

Long-Term Care Insurance

Insurance Needs Analysis

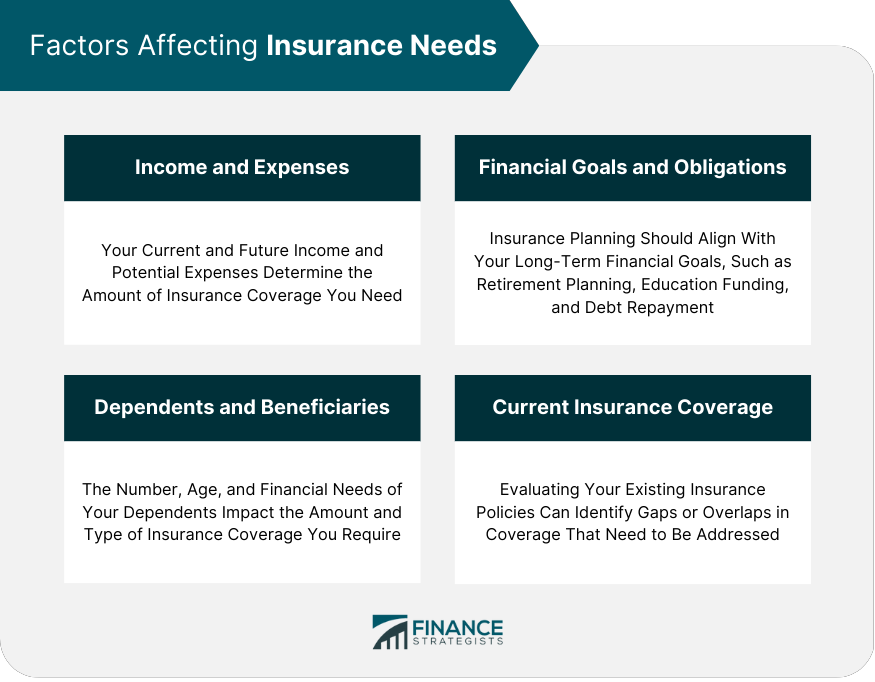

Factors Affecting Insurance Needs

Methods for Calculating Insurance Needs

Insurance Product Selection

Policy Features

Insurance Company Evaluation

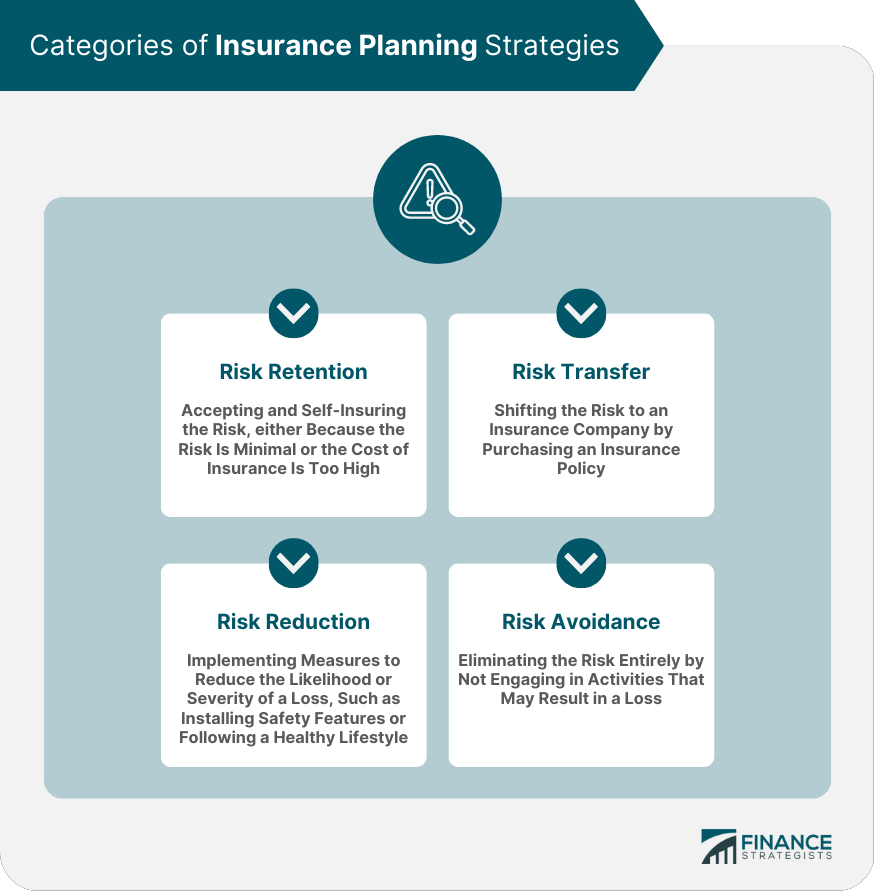

Insurance Planning Strategies

Review and Monitoring of Insurance Plans

Conclusion

Insurance Planning FAQs

Insurance planning is the process of evaluating and managing risks associated with potential losses and taking appropriate measures to mitigate those risks by selecting suitable insurance policies.

Insurance planning is important because it helps protect individuals, families, and businesses against unexpected financial losses due to events such as accidents, illness, and damage to property. Proper insurance planning can provide peace of mind and financial security.

When doing insurance planning, some key factors to consider include an individual's or business's assets, liabilities, income, family situation, and potential risks. Additionally, the types of insurance policies available, their coverage limits, deductibles, and premiums should also be considered.

Insurance planning should be reviewed regularly, at least once a year or whenever there is a significant life event such as marriage, having children, buying a home, or starting a business. This is necessary to ensure that insurance coverage is adequate and up-to-date to protect against potential risks.

While individuals can do their own insurance planning, it is recommended to consult an insurance professional who can help assess risks, provide guidance on suitable policies, and ensure that the coverage is adequate and appropriate. An insurance professional can also help identify potential gaps in coverage and offer solutions to mitigate risks.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.