A Rollover Individual Retirement Account (IRA) is a mechanism that enables individuals to transfer funds from one retirement account to another without facing immediate tax penalties. It serves as a "holding account," which ensures that assets remain in a tax-advantaged status until an individual decides on their next steps, be it reinvestment or eventual withdrawal. The most common scenarios prompting the creation of a Rollover IRA typically stem from job changes. When someone leaves an employer, they may have accumulated funds in a 401(k) or another employer-sponsored retirement plan. Instead of withdrawing and potentially facing early withdrawal penalties, many opt to roll these funds over into a Rollover IRA. This preserves the tax-advantaged status of the funds and provides more flexibility in investment options. Here's a closer look at the tax dynamics intertwined with Rollover IRAs, starting with the basics of capital gains tax. Capital gains tax is a tax on the profit realized from the sale of a non-inventory asset, like stocks, bonds, or real estate. Essentially, it's a tax on the growth of investments. The duration you hold an asset before selling it determines if the gain is categorized as short-term or long-term. Typically, assets held for a year or less before being sold are considered short-term, and those held for more than a year are viewed as long-term. Each type has its tax rate, with long-term capital gains generally benefiting from a lower rate than short-term gains, promoting longer-term investments. When executing a direct rollover, where funds are moved from one retirement account to another without the funds being given to the account holder, there are typically no immediate tax consequences. The money remains within the retirement account umbrella, ensuring it doesn’t count as a taxable distribution. One of the primary advantages of Rollover IRAs is that they're exempt from capital gains tax during the rollover process. This means that the growth of the investments within the original account is not taxed when transferred to the Rollover IRA. Mishandling a rollover can trigger tax events. For instance, with an indirect rollover, if the funds aren’t deposited into the new retirement account within 60 days, it’s deemed a distribution and becomes subject to taxes and possible penalties. It’s vital to note that with Traditional IRAs, the primary benefit has been the tax-deferred growth, which means you’re paying taxes upon withdrawal. These withdrawals are taxed at your ordinary income tax rate at the time of distribution. Having initially been funded with after-tax dollars, its major feature is the dual tax advantage: not only do investments grow tax-free, but qualified withdrawals during retirement are also entirely tax-free. This benefit hinges on meeting certain criteria, like the account being open for at least five years and the account holder being at least 59 1⁄2 years old during the withdrawal. Effectively managing a tax-free rollover requires meticulous attention to Internal Revenue Service rules and understanding the difference between direct and indirect rollovers. This rule stipulates that when you receive funds from a retirement account for the purpose of rolling them into another account (known as an indirect rollover), you must complete the rollover within 60 days. However, if you exceed this 60-day window, the withdrawn amount is treated as a distribution. This could mean facing both income tax on the amount and, if you're under 59½, an additional 10% early withdrawal penalty. With direct rollovers, funds are transferred directly between financial institutions. Essentially, the money is moved from one retirement account to another without you ever having the funds in your hands. Because of this direct transfer, there are no immediate tax implications, and the funds remain protected under the retirement account umbrella. Indirect rollovers offer more flexibility, as the funds are given to the account holder, who then has the responsibility of depositing them into a new retirement account. But with this flexibility comes the 60-day rule, as discussed earlier. Remember, only one indirect IRA-to-IRA rollover is allowed in a 12-month period, which doesn't apply to direct rollovers. Failure to adhere to rollover rules can have severe financial implications: Taxation on Distributions: If you miss the 60-day window for an indirect rollover or break other rules, the IRS views the amount as a distribution. This means the funds are subject to regular income tax. Early Withdrawal Penalties: If you're under the age of 59½ and don't properly execute the rollover, apart from the regular taxation, you'll also incur a 10% early withdrawal penalty on the distributed amount. Loss of Tax-Advantaged Growth: Retirement accounts offer the advantage of tax-deferred or tax-free growth. Mishandling a rollover can disrupt this benefit, potentially impacting your long-term financial goals. A Rollover IRA proves to be an invaluable tool for preserving and managing retirement funds during critical life transitions. Primarily employed when changing jobs, this mechanism allows seamless transfer of funds, maintaining their tax-advantaged status while offering flexibility in investment choices. The tax implications intertwined with Rollover IRAs, particularly regarding capital gains tax, underscore the importance of strategic planning for optimal financial outcomes. Direct rollovers stand as a tax-efficient choice, preventing immediate tax consequences and safeguarding assets within the retirement account. Furthermore, the distinction between Traditional and Roth Rollover IRAs highlights varying taxation dynamics upon withdrawal, showcasing the necessity of aligning account choices with individual financial strategies. A well-executed Rollover IRA empowers individuals to navigate these transitions with fiscal prudence and pave the way toward a secure financial future.Understanding Rollover IRA

Tax Implications of a Rollover IRA

Capital Gains Tax Basics

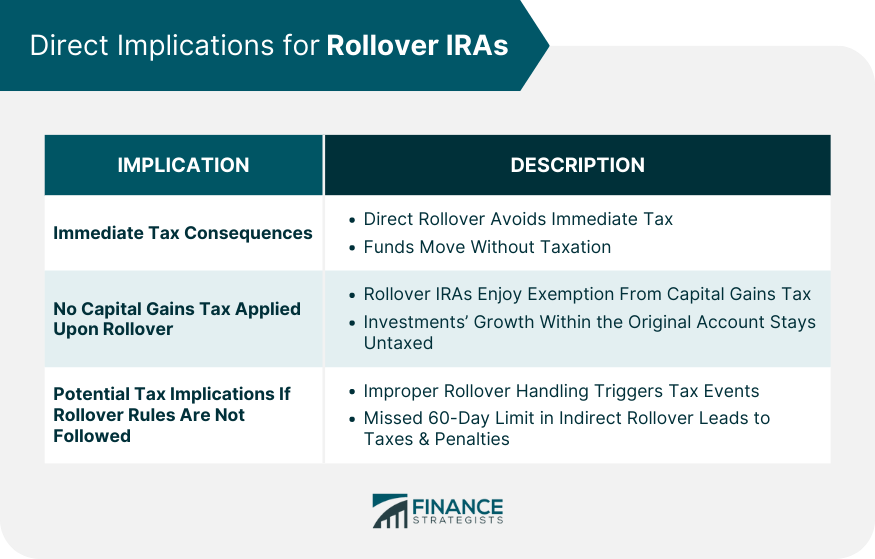

Direct Implications for Rollover IRAs

Immediate Tax Consequences

No Capital Gains Tax Applied Upon Rollover

Potential Tax Implications If Rollover Rules Are Not Followed

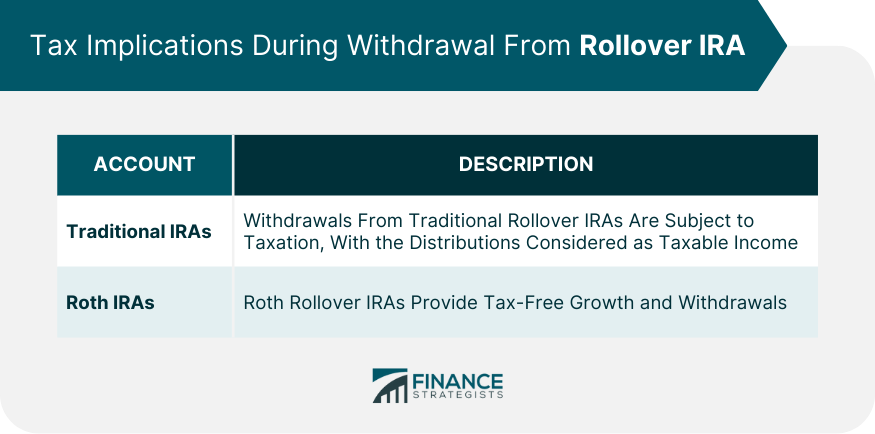

Tax Implications During Withdrawal From Rollover IRA

Traditional IRAs

Roth IRAs

Procedure for a Tax-Free Rollover

60-Day Rule

Direct vs Indirect Rollovers

Direct Rollovers

Indirect Rollovers

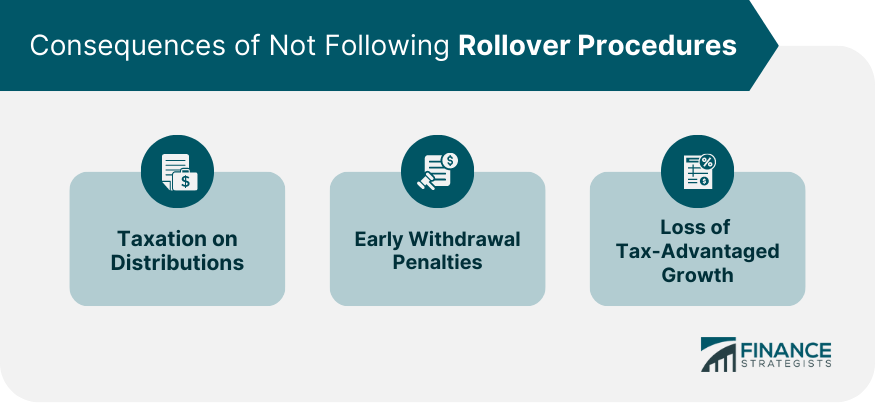

Consequences of Not Following Rollover Procedures

Conclusion

Capital Gains Tax on Rollover IRA FAQs

Capital Gains Tax on a Rollover IRA refers to the tax imposed on the profit realized from the sale of assets within the IRA account. It applies when you sell assets like stocks, bonds, or real estate within the Rollover IRA, and the gain is subject to taxation.

No, Capital Gains Tax is not applied during a Rollover IRA transfer. When you move funds from one retirement account to another through a direct rollover, the growth of investments within the original account remains untaxed during the transfer.

Capital Gains Tax rates for Rollover IRAs depend on the duration of asset ownership. Gains from assets held for over a year are generally taxed at a lower long-term rate, while those held for a year or less face a higher short-term rate.

While you can't completely avoid Capital Gains Tax within a Rollover IRA, careful planning can minimize its impact. Holding assets for more than a year can qualify for lower tax rates, and utilizing tax-efficient investment strategies can help manage the tax burden.

No, different types of assets within a Rollover IRA can have varying Capital Gains Tax rates. The tax rate depends on the asset's holding period – assets held for longer periods usually receive favorable tax treatment compared to short-term holdings.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.