IRAs, or Individual Retirement Accounts, offer a structured way to save for retirement with potential tax benefits. Traditional IRAs provide a tax deduction when you contribute, but you'll pay taxes on withdrawals in retirement. Roth IRAs, on the other hand, involve contributions with after-tax money, but your future withdrawals could be tax-free. With a traditional IRA, the immediate tax break can be beneficial, especially if you expect to be in a lower tax bracket in retirement. A Roth IRA offers the allure of tax-free money in retirement, especially valuable if you predict higher future tax rates or a higher personal income bracket. A traditional IRA offers immediate tax deductions, potentially reducing current taxable income, but taxes withdrawals in retirement. In contrast, Roth IRAs lack upfront tax breaks but provide tax-free withdrawals later on. Both have limitations, such as contribution income limits and, for traditional IRAs, mandatory minimum distributions (RMDs). Rollovers require impeccable timing. Convert too early or too late, and you could find yourself paying more in taxes than necessary. The ideal scenario involves rolling over when you're in a lower tax bracket than you anticipate in retirement, thus maximizing the tax benefits of the Roth. If life was as predictable as the sun's rise, this decision would be easy. But with fluctuating incomes, evolving tax laws, and personal financial changes, pinpointing the optimal time for a rollover can be as complex as threading a needle during an earthquake. There's a tax bill that comes knocking when you rollover from a traditional IRA to a Roth. Since traditional IRA contributions are pre-tax, converting means settling the score with the taxman. The conversion amount is added to your income for that year, potentially pushing you into a higher tax bracket. While it might sound daunting, it's a strategic move. You're essentially betting that the tax you pay now will be less than the tax you'd pay in the future on withdrawals. This gamble, however, isn't for the faint-hearted, as it requires a deep understanding of tax brackets and a speculative eye on the future. Your present tax bracket is a fundamental element in the rollover equation. If you're currently nestled in a lower tax bracket but foresee a jump in future income, a rollover could save substantial tax dollars down the road. However, if the opposite holds true and higher earnings now might plummet in retirement, sticking with a traditional IRA might be wise. Predicting future tax brackets is akin to predicting the weather three decades from now. Economic shifts, personal financial changes, and legislative tax reforms can all play a role. The key is to be informed, consult with a tax expert, and make the best-educated guess possible. What does your financial landscape look like in retirement? Do you anticipate a lavish lifestyle fueled by multiple income sources? Or perhaps a quieter, modest existence? If you expect to have higher income in retirement (from pensions, part-time work, or other investments), a Roth might be the shield against hefty tax bills on withdrawals. On the other hand, if retirement looks lean, with a limited income, the immediate tax relief provided by a traditional IRA might be more appealing. Your projected retirement income should be a considerable chunk of your decision matrix. The crystal ball of tax law is murky at best. Yet, speculating on its future can influence your rollover decision. If you believe tax rates will soar in the future, it makes the Roth IRA's tax-free withdrawals even more tantalizing. Conversely, if you're of the belief that tax rates will remain stagnant or drop, the allure of the Roth diminishes. It's a game of prediction, one that even the experts grapple with. While nobody has a definitive answer, staying abreast of current financial news and potential tax reforms can offer clues to the puzzle. Time can be a friend or foe. If retirement looms large, just around the corner, you may have less time to recover from the tax hit of a rollover. Conversely, if retirement is a distant speck on the horizon, the compound growth in a Roth IRA could offset any immediate tax implications. The more time you have until retirement, the longer your investments can grow tax-free in a Roth. Yet, if you're closer to retirement, evaluating the short-term tax consequences versus the potential benefits becomes paramount. Before embarking on a rollover journey, ensure you're eligible. Not all traditional IRAs can be converted to Roth IRAs, and certain criteria must be met. For instance, if you're married and file separately, certain income restrictions might apply. Knowledge is power. Familiarizing yourself with the IRS guidelines ensures a smooth transition. Consulting with a financial adviser or tax expert can also shed light on any nuances and help you navigate the eligibility maze. Just as you'd meticulously select a home to live in, the choice of where to house your Roth IRA is crucial. Different institutions offer varied investment options, fee structures, and customer service experiences. It's vital to compare and contrast, ensuring your chosen institution aligns with your financial goals and preferences. A seasoned financial adviser can be worth their weight in gold. Not only can they provide guidance on the best institutions, but they can also offer personalized advice tailored to your unique financial situation. Once you've pinpointed the perfect institution, it's time to set the ball rolling. Opening a Roth IRA account is typically a straightforward process. Most institutions provide online platforms where you can set up an account in a matter of minutes. Ensure you have all necessary documentation on hand, such as social security numbers, employment details, and bank account information. Once the account is active, you're one step closer to executing the rollover. The mechanics of transferring funds from a traditional IRA to a Roth is known as a "conversion." This can be accomplished via a direct trustee-to-trustee transfer, where funds move seamlessly between institutions, or a 60-day rollover, where you receive a check and then deposit it into the Roth account within the stipulated time frame. While the process might sound simple, it's essential to ensure all steps are followed to the letter. Any missteps, like missing the 60-day deadline, can lead to taxes and penalties. No financial move goes unnoticed by the IRS. Once the rollover is complete, it's imperative to report it. Typically, the financial institution handling the rollover will send you a Form 1099-R detailing the distribution from the traditional IRA. When filing taxes, this amount must be declared as income. Additionally, you'll need to fill out Form 8606, which details non-deductible contributions to IRAs. This form helps track the taxable portion of your distributions in retirement. Like paying the piper, there's an immediate tax cost associated with a rollover. Since you're moving from a tax-deferred account to a post-tax account, the IRS will want its share. The amount you convert will be added to your taxable income for the year, which could elevate your tax bill significantly. It's essential to be prepared for this upfront cost. Some individuals choose to spread out conversions over several years to mitigate the tax hit, a strategy known as "laddering." After the conversion, the funds within the Roth IRA grow tax-free. However, when you initially convert, you're setting the clock for the five-year rule (more on that later). This rule ensures that you don't withdraw earnings from the converted amount without penalty before a five-year period. Understanding the nuances of how the converted amount is treated, both in terms of growth and withdrawals, can influence how you manage and utilize your Roth IRA in the subsequent years. While the tax implication of a rollover might seem daunting, there are strategies to minimize the burden. For instance, executing rollovers in years when you have significant tax deductions, like hefty medical expenses or business losses, can offset the added income from the conversion. Furthermore, spreading the rollover over multiple years, known as "laddering," can ensure you don't jump into a higher tax bracket. Engaging a tax expert can help you navigate these waters and employ strategies that lessen the tax sting. Arguably, the crown jewel of the Roth IRA is its tax-free withdrawals in retirement. Imagine a river of income in your golden years, untouched by the grasping hands of taxes. While you pay taxes upfront on contributions, the long-term benefits, especially if you anticipate being in a higher tax bracket in retirement, can be substantial. The opposite is true for traditional IRAs. The immediate tax break might feel like a win today, but it's merely a deferral. When retirement comes calling, so does the tax bill on each withdrawal, potentially eroding the value of your savings. One of the major perks of a Roth IRA is the absence of required minimum distributions (RMDs). Unlike traditional IRAs, which mandate withdrawals starting at age 73, a Roth IRA lets your investments grow as long as you like. This flexibility is a gift, allowing for strategic withdrawals and potentially passing on a more substantial inheritance. For retirees who don't necessarily need their IRA money to live on, a Roth IRA provides an opportunity for prolonged tax-free growth, an invaluable tool in financial planning. When legacy planning comes into play, the Roth IRA shines brightly. Beneficiaries of Roth IRAs inherit the account tax-free, a boon for those looking to pass on wealth without the tax burdens. While they're required to take distributions, the money comes to them tax-free, preserving the value of your legacy. On the contrary, beneficiaries of traditional IRAs inherit not just the money, but also the tax implications, which can diminish the inheritance's value. When thinking long-term, especially about the financial well-being of loved ones, Roth IRAs offer a distinct advantage. Age is just a number, especially when it comes to Roth IRAs. Unlike traditional IRAs, which cut off contributions past the age of 70½, Roth IRAs have no age restrictions. As long as you have earned income, you can contribute. For older individuals who are still working or those who've embarked on second careers, this can be a significant benefit, allowing for additional tax-free growth. Continuing to contribute to your retirement savings, especially in a vehicle like the Roth IRA, can bolster your financial security, ensuring you have a robust nest egg to tap into when needed. Life is unpredictable. Emergencies arise, opportunities present themselves, and sometimes, accessing funds becomes crucial. With a Roth IRA, you can withdraw contributions (not earnings) anytime, tax, and penalty-free. This flexibility is unmatched in the retirement account realm and provides a safety net for unforeseen financial needs. While it's always advisable to let retirement funds grow undisturbed, knowing that you can access your contributions in dire circumstances offers peace of mind. Perhaps the most egregious blunder is not fully understanding or accounting for the tax implications of a rollover. An uninformed conversion can lead to an unexpectedly high tax bill, causing financial strain. Before converting, it's pivotal to estimate the tax cost, potentially using tax software or consulting with a tax professional. The five-year rule is a bit of a curveball in the Roth IRA game. Even if you're of age to make qualified distributions, if you haven't met the five-year holding requirement for the converted amount, penalties might apply to the earnings. Ensuring you're aware of this stipulation and tracking the holding period of your conversions is critical. Federal taxes often steal the limelight, but state taxes can play a pivotal role in the conversion equation. Some states offer tax breaks for retirement distributions, while others might tax retirement income heavily. Being oblivious to state tax implications can lead to unforeseen costs, disrupting your financial planning. Math errors, incorrect assumptions about tax brackets, or misunderstanding the nuances of tax laws can lead to a miscalculation of the tax burden associated with a rollover. This blunder can be costly, leading to budgetary disruptions or potential penalties. To safeguard against this, it's beneficial to run the numbers multiple times, use reliable tax software, and, if possible, get a second opinion from a tax expert. If you're employing the 60-day rollover method, where you receive the funds and then deposit them into the Roth IRA, precision is crucial. Missing this window, even by a day, can lead to the entire amount being considered a distribution, attracting taxes and penalties. Staying vigilant, marking calendars, setting reminders, and, if possible, opting for the direct trustee-to-trustee transfer can prevent this costly oversight. In determining the right time to rollover a traditional IRA to a Roth IRA, the decision hinges on factors like your current and expected future tax brackets, anticipated changes in tax laws, expected retirement income, and the time left until retirement. Both IRA types come with their pros and cons; while traditional IRAs offer immediate tax deductions, Roth IRAs promise tax-free withdrawals in retirement. Timing a rollover correctly can optimize tax benefits, but predicting the ideal moment is complex, given the uncertainties around income fluctuations, changing tax laws, and individual financial trajectories. Converting from a traditional to a Roth IRA has upfront tax costs, with the potential of pushing you to a higher tax bracket for that year. Nonetheless, such a move is strategic, premised on the belief that present tax rates might be lower than future ones. For a well-informed decision, consultation with tax and financial experts is essential, coupled with a keen understanding of both IRA structures.Overview of Traditional IRA and Roth IRA

Determining the Right Time to Rollover to a Roth IRA

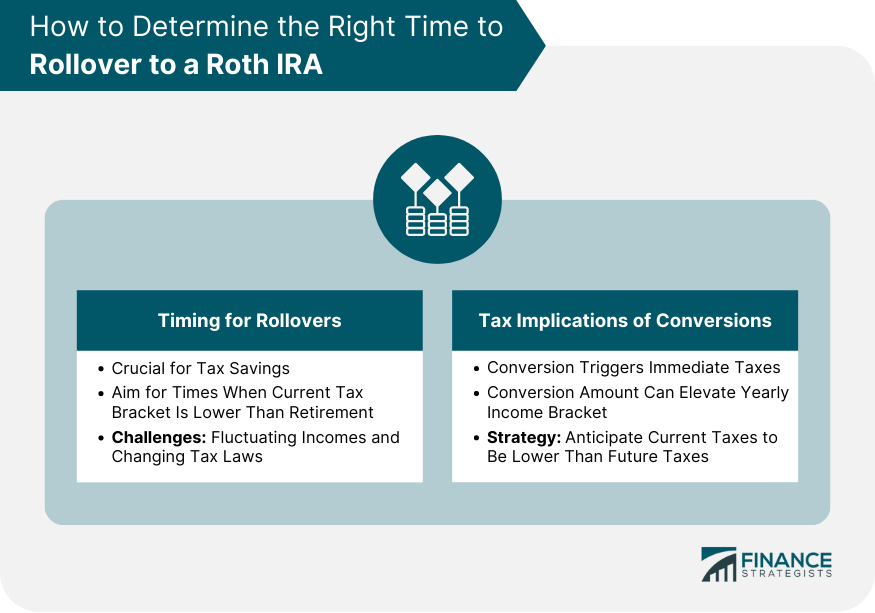

Importance of Timing in Rollovers

Tax Implications of Conversions

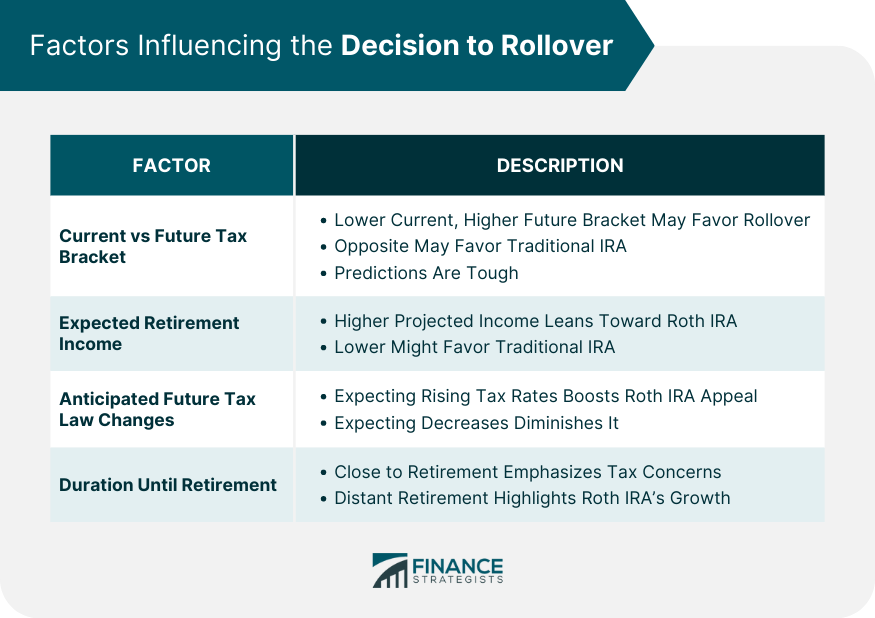

Factors Influencing the Decision to Rollover

Current Tax Bracket vs Expected Future Tax Bracket

Expected Retirement Income

Anticipated Future Tax Law Changes

Duration Until Retirement

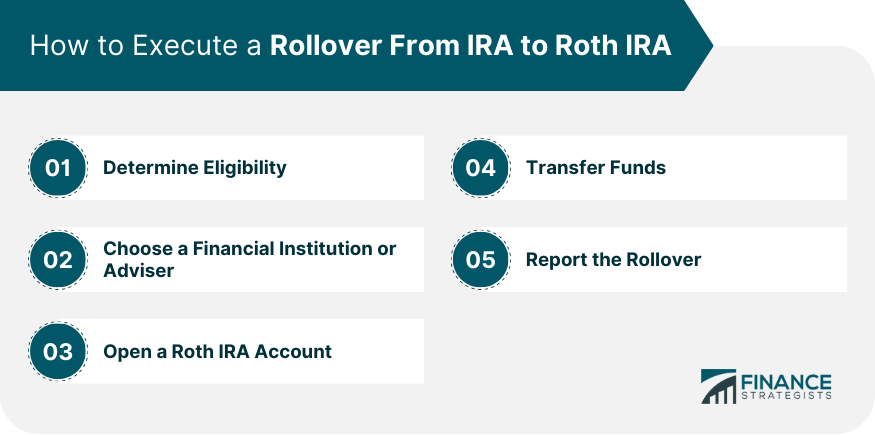

How to Execute a Rollover From IRA to Roth IRA

Determine Eligibility

Choose a Financial Institution or Adviser

Open a Roth IRA Account

Transfer Funds

Report the Rollover

Tax Implications of a Rollover

Upfront Tax Cost

Treatment of Converted Amount

Minimizing Tax Burden

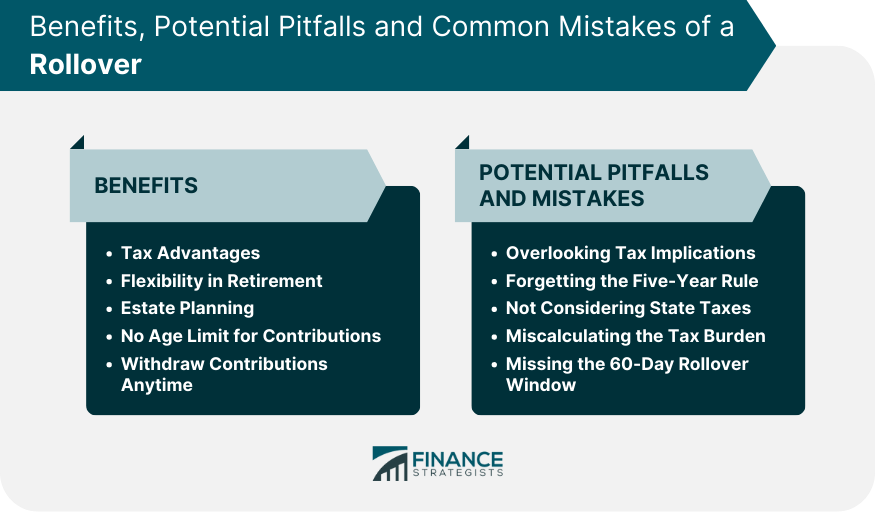

Benefits of a Roth IRA Over a Traditional IRA

Tax Advantages

Flexibility in Retirement

Estate Planning

No Age Limit for Contributions

Withdraw Contributions Anytime

Potential Pitfalls and Common Mistakes of a Rollover

Overlooking Tax Implications

Forgetting the Five-Year Rule

Not Considering State Taxes

Miscalculating the Tax Burden

Missing the 60-Day Rollover Window

Bottom Line

When to Rollover IRA to Roth IRA FAQs

Roth IRAs offer tax-free withdrawals, no age limit for contributions, flexibility in retirement, and advantages for estate planning.

The ideal time considers factors like your current tax bracket, expected retirement income, and potential future tax law changes.

Conversion incurs an upfront tax cost, with the converted amount treated differently, but strategies exist to minimize the tax burden.

Mistakes include overlooking tax implications, forgetting the five-year rule, not considering state taxes, and missing the 60-day rollover window.

Determine eligibility, choose a financial institution or adviser, open a Roth account, transfer funds, and report the rollover.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.