A 403(b) plan, often referred to as a tax-sheltered annuity (TSA) plan, is a type of retirement savings plan specifically designed for employees of public schools, non-profit organizations, and certain ministers. It's named after Section 403(b) of the Internal Revenue Code, which sets the rules for this kind of retirement plan. The origin of 403(b) plans can be traced back to 1958, when they were introduced by the U.S. Congress to encourage non-profit employees to start saving for retirement. They've evolved over time with several changes in contribution limits and investment options. However, the primary goal remains the same: to provide a secure and efficient method for eligible employees to save toward retirement. Eligibility for a 403(b) plan is primarily limited to employees of public schools and certain tax-exempt organizations. Once an individual confirms their eligibility, the enrollment process can begin. This usually involves choosing the amount to contribute from each paycheck and selecting the investments. Employees can generally choose to make either pre-tax or Roth (after-tax) contributions. The employee's chosen contributions are automatically deducted from their pay and invested in the chosen investments. Employers offering a 403(b) plan have the responsibility of setting up the plan, ensuring it complies with all relevant laws and regulations, and offering appropriate investment options. They must also provide employees with necessary information about the plan and its benefits. These are contributions made by the employee from their salary before taxes. The money grows tax-deferred until it's withdrawn, at which time it is taxed as ordinary income. Employers have the option to match a certain percentage of the employee's contributions, but this isn't a requirement. These contributions are usually vested over time, meaning employees earn the right to keep them after a certain number of years of service. These are contributions made by the employer that are not dependent on the amount the employee contributes to the plan. They may include profit-sharing contributions or contributions made under a Simplified Employee Pension Plan (SEP). The general limit on the amount an employee can contribute to a 403(b) plan in 2026 is $24,500 ($23,500 in 2025). Employees aged 50 or over can make additional contributions beyond the regular limit, known as catch-up contributions. In 2026, the catch-up contribution limit is $8,000 ($7,500 in 2025). Vesting refers to the employee's ownership of the money in the 403(b) plan. Employee contributions and earnings are always 100% vested. However, any employer contributions may be subject to a vesting schedule, which varies by plan. One option for 403(b) plan investments is an annuity contract provided through an insurance company. Annuities are contracts between the investor and the insurance company where the investor makes a lump-sum payment or a series of payments in exchange for regular disbursements in the future. Another option is to invest in custodial accounts that are primarily invested in mutual funds. Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. Churches or church-related organizations can invest in retirement income accounts for their employees, which include mutual funds and other investment vehicles. This option provides a great deal of flexibility, allowing the investor to tailor their portfolio to their individual needs and goals. One significant advantage of a 403(b) plan is the tax benefit it offers. Contributions are made on a pre-tax basis, meaning they lower the participant's taxable income for the year, reducing the amount of income tax they owe. Additionally, the investments grow tax-deferred, meaning that taxes on the gains aren't paid until the money is withdrawn in retirement. Some employers may choose to match their employees' contributions, providing an additional source of retirement income. This effectively increases the employee's total compensation without increasing their taxable income. Despite its benefits, a 403(b) plan has limitations. Contribution limits restrict how much can be invested in the plan annually. Withdrawals before age 59 1/2 may be subject to a 10% early withdrawal penalty in addition to income taxes. Some 403(b) plans have limited investment options, and employees of small non-profit organizations may not receive an employer match. While your money is meant to stay in a 403(b) until retirement, certain situations qualify you to make withdrawals. These include reaching age 59 1/2, leaving your employer, disability, and financial hardship, though the latter may be subject to income tax and potentially an early withdrawal penalty. Early withdrawals, or distributions taken before age 59 ½, are typically subject to a 10% early withdrawal penalty in addition to being taxed as regular income. However, exceptions may apply, such as in the case of disability or certain medical expenses. Some 403(b) plans allow for loans. When permitted, the IRS allows for loans up to 50% of the vested account balance or $50,000, whichever is less. These must be paid back with interest, typically through payroll deductions. If you leave your job, you may have the option to roll over your 403(b) to another retirement plan or an Individual Retirement Account (IRA). This allows you to avoid an early withdrawal penalty and continue to defer paying taxes on your investment. Both 403(b) and 401(k) plans are types of defined contribution plans, and their annual contribution limits are the same. The primary difference is the type of employer that can offer these plans – 401(k)s are offered by for-profit companies, while 403(b)s are available to employees of non-profit organizations. Like 403(b) plans, 457(b) plans are available to employees of certain non-profit organizations. However, 457(b) plans also allow employees to take penalty-free withdrawals if they leave their employer, regardless of their age at the time of withdrawal. While IRAs also offer tax-advantaged retirement savings, they have lower contribution limits than 403(b) plans. However, IRAs often offer more investment options. A traditional IRA offers tax-deferred growth like a 403(b), while a Roth IRA offers tax-free growth. Investing in a variety of asset classes can help manage risk and potentially increase returns. The right mix of stocks, bonds, and other investments depends on your risk tolerance and retirement goals. Understanding the fees associated with your 403(b) can save you a significant amount of money over time. Look for low-cost options, like index funds, that offer diversification at a low cost. Regularly reviewing your 403(b) can help ensure it stays aligned with your retirement goals. This includes checking your contribution amount, investment mix, and beneficiary designations. A 403(b) plan is a highly advantageous tool for retirement savings, particularly for those employed by public schools, non-profit organizations, and certain ministers. It offers significant tax benefits and the potential for employer matching, providing a lucrative means of saving for retirement. While it has its limitations, understanding the specifics, such as contribution limits and early withdrawal penalties, can help employees maximize their benefits. Comparing the 403(b) plan with other retirement options allows individuals to make informed decisions best suited to their financial goals. Regular reviews and smart strategies like diversifying investments and understanding fees can enhance the benefits of a 403(b) plan. As with any financial decision, individuals should consider their unique circumstances and possibly consult with a financial advisor before making decisions about their 403(b) plan. The right approach can ensure a secure and comfortable retirement.Overview of 403(b) Plans

How a 403(b) Plan Works

Setting up a 403(b) Plan

Employee Enrollment Process

Employer Responsibilities

Understanding Contributions

Elective Deferrals

Employer Contributions

Non-elective Contributions

Contribution Limits

Regular Contribution Limits

Catch-up Contributions for Older Employees

Vesting in a 403(b) Plan

Investment Options Within a 403(b) Plan

Annuity Contracts With Insurance Companies

Custodial Accounts With Mutual Funds

Retirement Income Accounts for Church Employees

Advantages of a 403(b) Plan

Significant Tax Advantages

Employer Contribution Matching

Disadvantages of a 403(b) Plan

Contribution Limitations

Penalties for Early Withdrawals

Limited Investment Options and Employer Matching

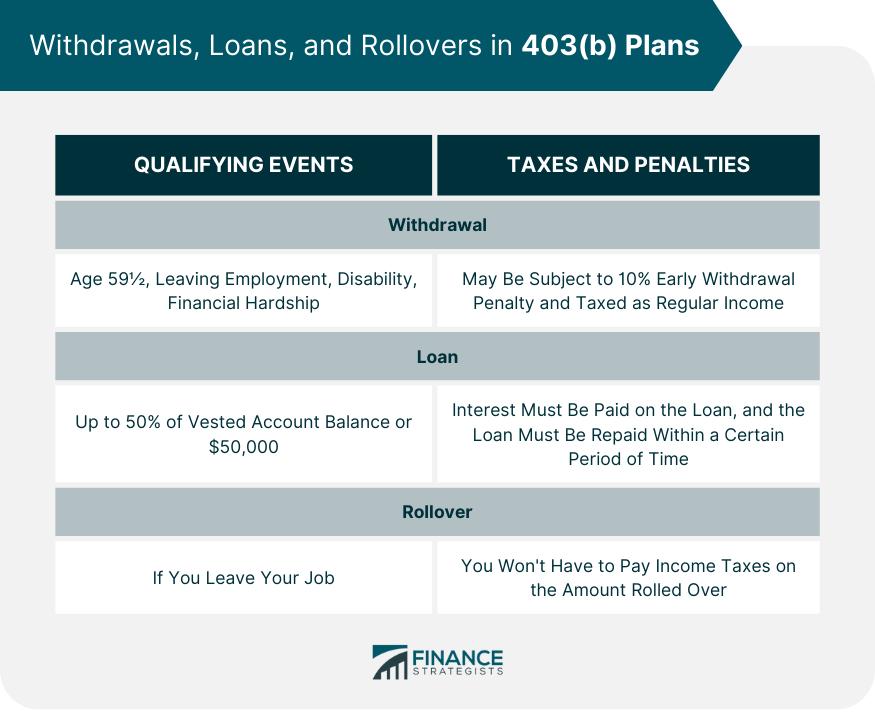

Understanding Withdrawals, Loans, and Rollovers in 403(b) Plans

Guidelines for Withdrawals

Qualifying Events for Withdrawals

Taxes and Penalties on Early Withdrawals

Policies on Loans Against a 403(b) Plan

Rollover Provisions for 403(b) Plans

Comparison of a 403(b) Plan to Other Retirement Plans

403(b) vs 401(k)

403(b) vs 457(b)

403(b) vs Traditional and Roth IRAs

Strategies for Maximizing 403(b) Plan

Diversify Investments

Decipher Fees and Expenses

Review Plan Regularly

Bottom Line

How a 403(b) Plan Works FAQs

A 403(b) plan is a tax-advantaged retirement savings plan for employees of public schools, non-profit organizations, and certain ministers.

The 403(b) plan offers significant tax advantages. Contributions are made on a pre-tax basis, reducing taxable income for the year. Investments grow tax-deferred until withdrawn in retirement.

Some employers may choose to match employees' contributions to a 403(b) plan, effectively increasing the employee's total compensation without increasing their taxable income.

A 403(b) plan has several limitations, including annual contribution limits, potential penalties for early withdrawal, and sometimes limited investment options or lack of employer matching.

Similar to 401(k) plans, 403(b) plans are offered by non-profit employers. The contribution limits are the same, but 403(b) plans may have fewer investment options. Compared to IRAs, 403(b) plans allow higher contributions but may have higher fees.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.