A 403(b) to 457(b) rollover refers to the process of moving funds from a 403(b) retirement plan to a 457(b) plan. The 403(b) plan, also known as a tax-sheltered annuity plan, is primarily offered to employees of public schools and certain tax-exempt organizations. A 457(b) plan is a deferred compensation retirement plan offered to state and local public employees and certain non-profit employees. The purpose of this rollover is to consolidate retirement assets, potentially access a broader array of investment options, or adapt to a change in employment. This procedure involves assessing both plans, confirming the receiving plan accepts rollovers, initiating the transfer (either directly or indirectly), and verifying the successful transfer and appropriate allocation of assets. It's crucial to carefully navigate this process to avoid possible tax penalties or disruptions to long-term retirement savings. Conducting a rollover from a 403(b) to a 457(b) plan involves several critical steps. Before initiating the rollover process, you'll need to understand both your current 403(b) and the prospective 457(b) plans. Make sure to assess the fees, investment options, and any potential penalties associated with each plan. If you decide to proceed with the rollover, the first step is to confirm that your 457(b) plan accepts rollovers from 403(b) plans. This information can typically be obtained by contacting the plan administrator. Once you've confirmed that a rollover is possible, you can initiate the transfer process. This process can either be a direct rollover, where the funds are transferred directly from your 403(b) account to your 457(b) account, or an indirect rollover, where the funds are distributed to you, and you have 60 days to deposit them into the new account. After the rollover, it's essential to confirm that the funds have been successfully transferred to your 457(b) account. Additionally, you'll want to review the investment options in your new plan and ensure your assets are allocated according to your investment strategy. There are several advantages to consider when contemplating a 403(b) rollover to a 457(b) plan. One of the significant benefits is the potential for expanded investment options. While 403(b) plans are often limited to annuities and mutual funds, 457(b) plans may provide a broader array of investment options, depending on the plan's specifics. Consolidating retirement savings from multiple accounts into a single 457(b) account can help streamline your retirement planning. It simplifies management and provides a clearer picture of your overall retirement savings. 457(b) plans come with unique features that might not be available with 403(b) plans. For instance, unlike 403(b) and 401(k) plans, there's no 10% penalty for withdrawals before age 59½, providing greater flexibility for early retirement. Despite its potential benefits, a 403(b) rollover to a 457(b) plan also presents certain challenges. There could be fees associated with the rollover, such as surrender charges on annuity contracts within the 403(b) plan. Additionally, an indirect rollover can trigger taxes if you fail to deposit the funds into your 457(b) account within 60 days. Some 457(b) plans may limit access to the funds until the plan participant experiences a "trigger" event, like separation from service, which might not align with your financial needs. Not all 457(b) plans accept rollovers from 403(b) plans. It's important to confirm the specifics of your plan before initiating the rollover process to avoid complications. When contemplating a rollover from a 403(b) to a 457(b), there are several key considerations to keep in mind. Understanding the unique features, advantages, and limitations of both your current 403(b) and prospective 457(b) plans is crucial. It ensures you're making a fully informed decision that aligns with your financial goals and retirement strategy. Rollovers can have tax implications. Direct rollovers generally don't incur taxes, but with indirect rollovers, you could end up with a significant tax bill if you fail to deposit the funds into your new account within the 60-day window. Given the complexities involved, consulting with a financial advisor is highly recommended. They can provide personalized advice, taking into consideration your financial situation and retirement goals. Rollover from a 403(b) to a 457(b) plan can be a viable retirement strategy for employees transitioning within the public or nonprofit sector. This move consolidates retirement savings, potentially simplifying account management and offering a wider range of investment options. However, it's crucial to thoroughly understand both plans' features, fees, and potential penalties before initiating the rollover. Moreover, not all 457(b) plans accept rollovers from 403(b) plans, and there may be fees or penalties involved. Key benefits include increased investment options, streamlined retirement planning, and unique 457(b) features like no penalty for early withdrawals. However, accessibility limitations and potential tax implications need to be considered. Therefore, professional advice from a financial advisor is highly recommended to navigate this complex process and make informed decisions that align with one's financial goals and retirement strategy.Overview of 403(b) Rollover to 457(b)

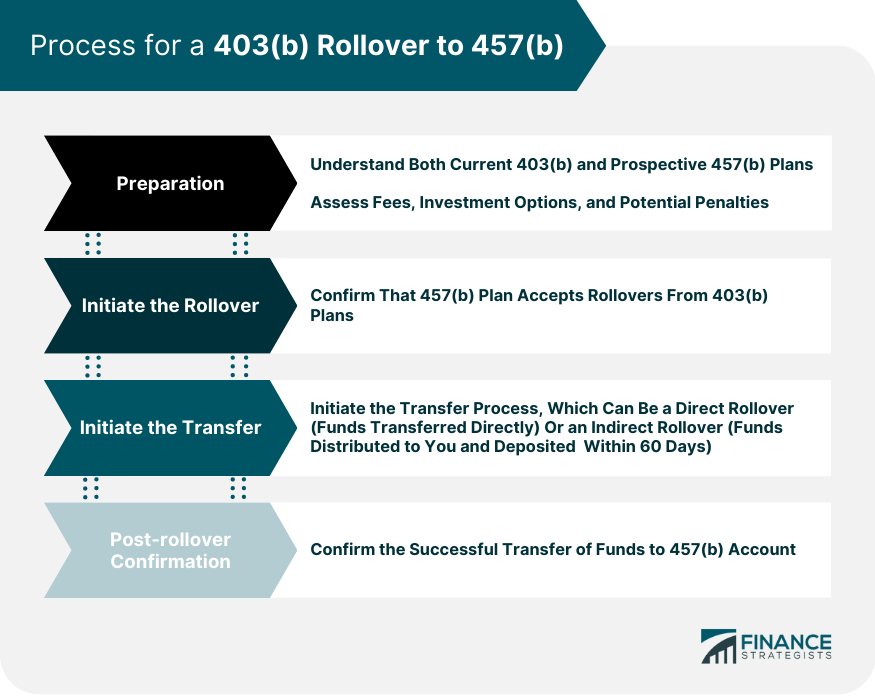

Process for a 403(b) Rollover to 457(b)

Preparation

Initiate the Rollover

Initiate the Transfer

Post-rollover Confirmation

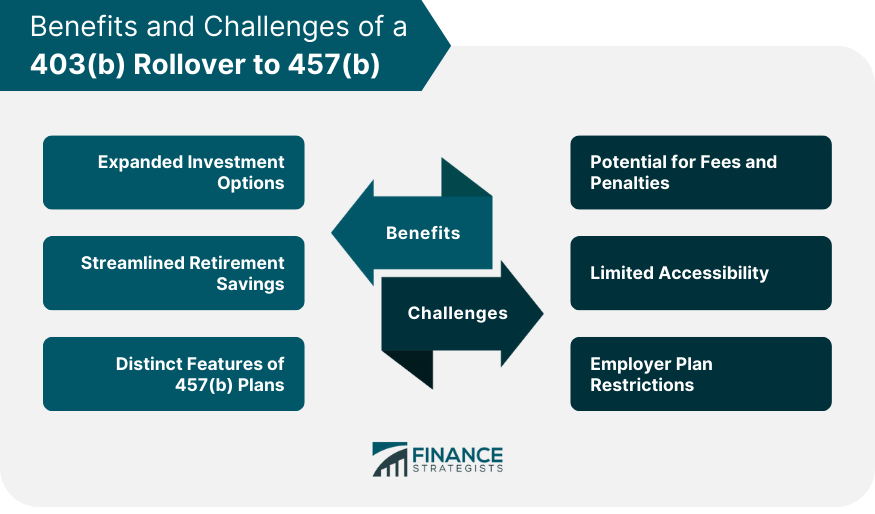

Benefits of a 403(b) Rollover to 457(b)

Expanded Investment Options

Streamlined Retirement Savings

Distinct Features of 457(b) Plans

Challenges of a 403(b) Rollover to 457(b)

Potential for Fees and Penalties

Limited Accessibility

Employer Plan Restrictions

Key Considerations for a 403(b) Rollover to 457(b)

Comparison of Plan Features

Understanding Tax Implications

Role of Financial Advisors

Final Thoughts

403(b) Rollover to 457(b) FAQs

A 403(b) rollover to a 457(b) is a financial strategy involving the transfer of retirement savings from a 403(b) plan, typically offered to employees of public schools and certain tax-exempt organizations, to a 457(b) plan, commonly provided to government and some nonprofit employees.

A rollover may be considered to consolidate retirement savings, simplify account management, and possibly expand investment options. Notably, 457(b) plans do not penalize early withdrawals before age 59½, providing greater flexibility for those planning an early retirement.

Steps include: reviewing details of both the 403(b) and 457(b) plans, consulting a financial advisor, initiating the rollover (confirming the 457(b) plan accepts rollovers), executing the transfer (either direct or indirect), and confirming the successful transfer.

Challenges may include fees and penalties associated with the rollover, limited access to funds until a "trigger" event occurs, and the fact that not all 457(b) plans accept rollovers from 403(b) plans.

Direct rollovers, where funds transfer from the 403(b) directly to the 457(b), typically do not incur immediate taxes. However, indirect rollovers, where funds are distributed to the individual who then has 60 days to deposit them into the new account, could trigger taxes if not completed within the allotted timeframe.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.