The 403(b) Early Withdrawal Penalty is a fee imposed by the Internal Revenue Service (IRS) on individuals who withdraw money from their 403(b) retirement accounts before reaching a specified age. The penalty is designed to dissuade individuals from depleting their retirement savings prematurely. In general, the penalty applies to withdrawals made before the age of 59½. These withdrawals are not only taxed as ordinary income but are also subject to a 10% additional tax, commonly known as the early withdrawal penalty. The IRS, however, allows for certain exceptions where the penalty may not apply. The IRS aims to ensure that funds set aside in 403(b) retirement accounts are used for their intended purpose – providing income during retirement. Imposing a penalty on early withdrawals discourages individuals from tapping into these funds prematurely. This policy aims to help maintain the integrity of the retirement savings system and ensure that people have sufficient funds for their post-working years. Generally, individuals who withdraw funds from their 403(b) account before reaching the age of 59½ are subject to the penalty. However, there are exceptions to this rule. For instance, if the account holder qualifies for early retirement (typically defined as age 55 or older), they may be exempt from the penalty. If an account holder is still employed by the organization sponsoring the 403(b) plan, they may not be eligible for penalty-free withdrawals. However, certain circumstances, such as a permanent separation from service or a change in employment status, might allow for penalty exceptions. It's important to review the specific employment status criteria outlined in your 403(b) plan documents to understand how they affect the penalty for early withdrawals. In most cases, the penalty applies to both contributions made by the account holder and any earnings on those contributions. However, if an individual has not yet vested in their employer's contributions, the penalty may only apply to the vested portion of the account balance. Vesting schedules can vary, so it's crucial to understand the specific criteria outlined in your 403(b) plan documents. The amount of the early withdrawal penalty from a 403(b) retirement account is typically 10% of the distribution. This penalty is levied in addition to any regular income taxes due on the withdrawal. Therefore, an early withdrawal can result in a significant reduction of the total amount received. To illustrate, consider a scenario where an individual in the 24% tax bracket takes an early distribution of $10,000 from their 403(b) plan. In this case, they would owe $2,400 in income taxes and an additional $1,000 as an early withdrawal penalty, leaving only $6,600 of the original withdrawal. Withdrawals from a 403(b) retirement account before age 59½ are not only subject to the 10% early withdrawal penalty but are also taxable as ordinary income. This means that the withdrawal amount is added to the individual's other income for the year, possibly pushing them into a higher tax bracket. This can significantly impact an individual's tax liability for the year. As such, understanding the tax implications of early withdrawals from a 403(b) plan can help individuals make informed decisions and potentially avoid unnecessary financial stress. Qualified distributions are certain types of withdrawals from a 403(b) plan that are not subject to the 10% early withdrawal penalty. These typically include distributions made on or after the age of 59½, distributions made due to the account holder's total and permanent disability, and distributions made to a beneficiary or estate upon the death of the account holder. There are also other types of qualified distributions that are subject to more complex rules. For instance, distributions that are part of a series of substantially equal periodic payments (SEPP) can avoid the penalty, but they must adhere to specific IRS guidelines. The most common age-based exception to the 10% early withdrawal penalty is for individuals who are at least 59½ years old. At this age, they are free to withdraw funds from their 403(b) account without penalty, though the withdrawals are still subject to regular income tax. Another age-related exception occurs for individuals who leave their job in or after the year they turn 55. They may be able to take withdrawals from the 403(b) account associated with that job without incurring the penalty, a rule known as the Rule of 55. However, this rule doesn't apply to accounts from previous employers or to IRAs. There are also exceptions to the 10% early withdrawal penalty for special circumstances, including disability and certain medical expenses. For instance, if a person becomes totally and permanently disabled, they can withdraw funds from their 403(b) account without incurring the penalty. Additionally, individuals can also make penalty-free withdrawals to pay for unreimbursed medical expenses that exceed a certain percentage of their adjusted gross income (AGI). However, these withdrawals must be made in the same year the medical expenses are incurred. The 10% early withdrawal penalty is typically withheld by the financial institution managing the 403(b) plan at the time of distribution. The institution is responsible for reporting the withdrawal and any withheld taxes to the IRS, and the individual also receives a form (1099-R) reporting the distribution. The penalty and the regular income tax due on the withdrawal are settled when the individual files their income tax return for the year. If the financial institution does not withhold enough to cover the total amount due, the individual may have to pay additional taxes when they file their tax return. One effective way to avoid the early withdrawal penalty is through a rollover. This is a method by which you can move your funds from your current retirement account to another eligible retirement account or IRA. By doing a rollover, the funds remain within the retirement system and continue to grow tax-deferred. A direct rollover, where the funds move directly from one institution to another, is generally the best option as it avoids any possibility of the distribution being considered a taxable event. It's crucial, however, to ensure that the rollover is completed within 60 days to avoid the distribution being treated as an early withdrawal. Taking a loan from your 403(b) plan can be another strategy to access funds without triggering the early withdrawal penalty. Although not all 403(b) plans allow for loans, those that do typically let you borrow the lesser of $50,000 or 50% of your vested account balance. It's important to note that such loans must be repaid within five years, and payments must be made at least quarterly. Failure to meet these repayment terms could result in the remaining loan balance being considered a distribution, which could be subject to taxes and penalties. Individuals might also explore other retirement savings alternatives to minimize the early withdrawal penalty. Find you frequently need to access your retirement funds due to financial hardship. It may be worth considering alternatives such as a Roth IRA, where contributions can be withdrawn at any time without taxes or penalties. Another potential alternative is to build up an emergency fund outside of your retirement accounts. This can provide a buffer for unexpected expenses, reducing the need to tap into your retirement savings early. The 403(b) early withdrawal penalty is a significant deterrent against using retirement funds prematurely, and knowing when it applies and how much it can cost you is essential for effective retirement planning. Age-based criteria play a significant role, with individuals typically facing penalties for withdrawals made before the age of 59½. However, exceptions exist, such as early retirement eligibility or the Rule of 55. Employment status also impacts penalty applicability, with exceptions for permanent separation or employment status changes. Contribution and vesting criteria determine the portion of the account balance subject to the penalty. The penalty amount is generally 10% of the distribution, in addition to regular income taxes. Understanding these criteria empowers individuals to make informed decisions. Considering alternatives like rollovers, loans, or exploring other retirement savings options to minimize the early withdrawal penalty.Overview of 403(b) Early Withdrawal Penalty

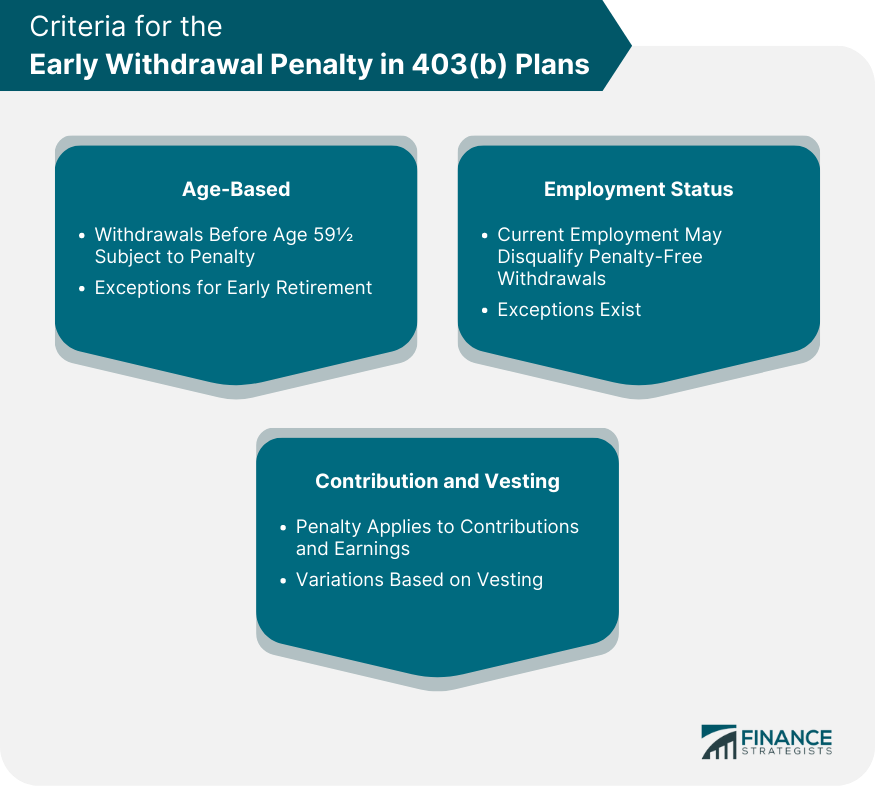

Criteria for the Early Withdrawal Penalty to 403(b) Plans

Age-Based

Employment Status

Contribution and Vesting

403(b) Early Withdrawal Penalty Amount

Tax Implications of 403(b) Early Withdrawals

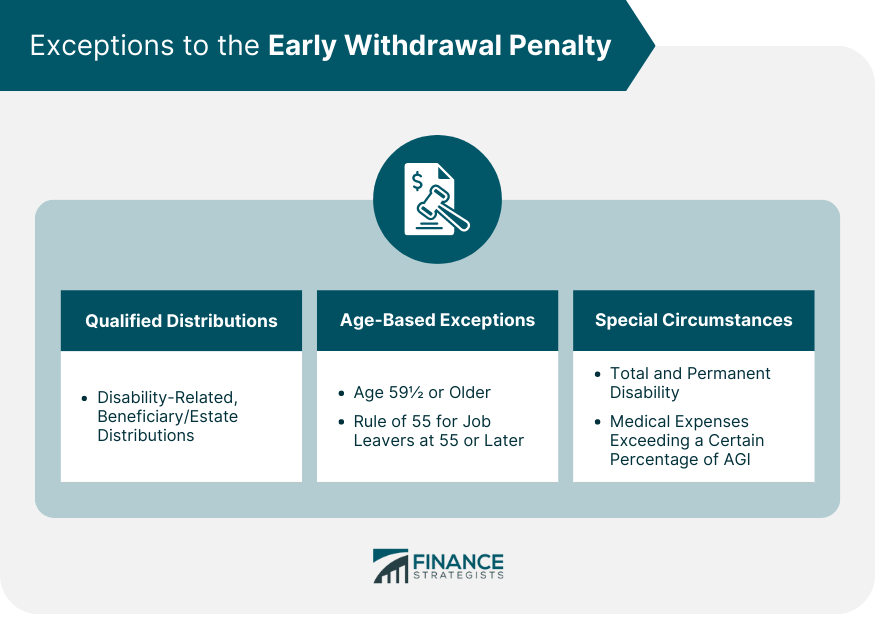

Exceptions to the Early Withdrawal Penalty

Qualified Distributions

Age-Based Exceptions

Special Circumstances (e.g., Disability, Medical Expenses)

Paying the Early Withdrawal Penalty

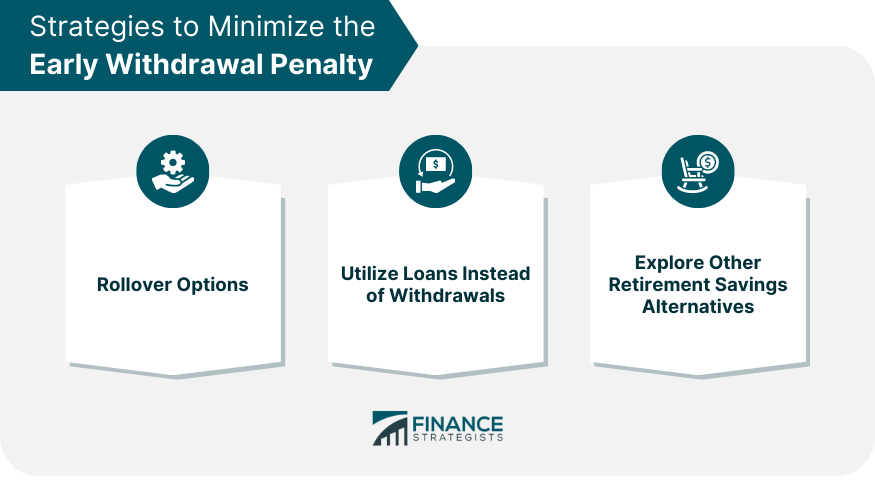

Strategies to Minimize the Early Withdrawal Penalty

Rollover Options

Utilizing Loans Instead of Withdrawals

Exploring Other Retirement Savings Alternatives

Conclusion

403(b) Early Withdrawal Penalty FAQs

The 403(b) early withdrawal penalty is a 10% additional tax that applies to distributions made from a 403(b) retirement account before the account holder reaches the age of 59 ½, unless an exception applies.

Yes, there are several exceptions to the penalty, including distributions made after age 59½, distributions due to total and permanent disability, distributions to a beneficiary or estate upon the account holder's death, and distributions for certain medical expenses.

Yes, rolling over your 403(b) distribution to another eligible retirement account within 60 days can allow you to avoid the early withdrawal penalty.

Yes, if your 403(b) plan allows loans, you can borrow funds without incurring the early withdrawal penalty. However, the loan must be repaid according to specific terms to avoid being considered a taxable distribution.

Early withdrawals from a 403(b) plan are subject to regular income tax and the 10% early withdrawal penalty unless an exception applies. The distribution can also increase your total income for the year, possibly pushing you into a higher tax bracket.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.