The term "403(b) plan termination" refers to the discontinuation of a 403(b) retirement plan, which is designed for employees of public schools, certain tax-exempt organizations, and ministers. The purpose of the termination can be varied, often due to reasons like organizational closure, a change in tax status, or the decision to switch to a different retirement plan. The impact of a 403(b) plan termination can be significant for plan participants as it affects their retirement savings and tax situations. They might need to reallocate their funds to a different retirement plan or an individual retirement account (IRA) to maintain the tax advantages. In a broader context, understanding the implications of a 403(b) plan termination is crucial for both employers and employees in planning for financial stability and retirement security. The termination process for a 403(b) plan is multifaceted and requires meticulous attention to several steps. The decision to terminate a 403(b) plan should not be taken lightly. An organization must consider the financial and operational implications, explore alternative options, and consult with financial and legal professionals. Once the decision is made, participants must be informed about the plan termination. This communication should include the reason for termination, the expected timeline, and the options available to the participants. Organizations are required to comply with specific IRS guidelines for 403(b) plan termination. They must also prepare a plan termination resolution, update plan documents, and notify the IRS. Participants' assets must be fully vested and distributed, or rolled over into another eligible retirement plan or individual retirement account (IRA). The final step involves filing a Form 5500-series return and any necessary plan termination forms with the IRS. Terminating a 403(b) plan can have significant implications for both employers and employees. Financial Implications: There may be costs associated with the termination, including professional fees and potential penalties for non-compliance. Legal Implications: Employers must adhere to the legal requirements for plan termination to avoid possible litigation. Operational Implications: The termination may involve administrative challenges and potential disruption to normal business operations. Financial Implications: Plan termination might affect the retirement savings of the employees, especially if they have not reached retirement age. Tax Implications: Without a proper rollover, the distributed assets might be subjected to income tax and possibly early withdrawal penalties. Retirement Planning Implications: The termination can impact the employees' retirement planning strategies, necessitating revisions to their plans. After the termination of a 403(b) plan, there are several post-termination actions that must be addressed. Direct Rollover Into Another Retirement Plan: Employees may move their assets into another eligible retirement plan, if available and permitted by the new program. This action can preserve the tax advantages and allow the savings to continue to grow. Direct Rollover Into an Individual Retirement Account (IRA): Employees can also choose to roll over their funds into an IRA. Both traditional and Roth IRAs can be suitable options, depending on the individual's circumstances and goals. Lump-Sum Distribution: If an immediate need for the funds arises, an employee may choose a lump-sum distribution. However, this might have significant tax implications and potential early withdrawal penalties. Leave It With the Original Plan: In some cases, the plan administrator may allow the funds to stay in the original plan, even after its termination, until the normal retirement age is reached. Information Provision and Assistance: Employers should assist employees in understanding the implications of the termination and the options available to them. Continued Regulatory Compliance: Even after termination, employers have an obligation to ensure all IRS filings are up-to-date and any outstanding issues are resolved. Several special considerations must be taken into account during the termination process. Orphaned plans, those abandoned by their sponsoring organizations, present unique challenges. The Department of Labor provides guidance through its Abandoned Plan Program. Plan terminations can be complex, and complications may arise, such as dealing with lost participants, erroneous contributions, or issues with the plan's vesting schedule. Throughout the termination process, it's essential to ensure the legal rights of participants are protected. Participants must be fully vested in their account balance, have the opportunity to roll over their assets and receive any required notices. The termination of a 403(b) plan is a multi-faceted process with significant implications for both employers and employees. It demands careful deliberation, comprehensive communication, strict adherence to regulations, and strategic handling of assets. While the decision can impact the financial landscape and retirement planning for employees, it also carries financial, legal, and operational repercussions for employers. Nevertheless, through effective post-termination actions, employees can safeguard their retirement savings and tax benefits. The process may involve potential challenges, including handling orphaned plans and navigating potential complications, but the overall aim is to ensure legal protection for participants. In sum, although a 403(b) plan termination is a substantial event, with thoughtful management, it can be navigated smoothly, leading to a strategic shift in retirement planning, rather than a derailment.What Is a 403(b) Plan Termination?

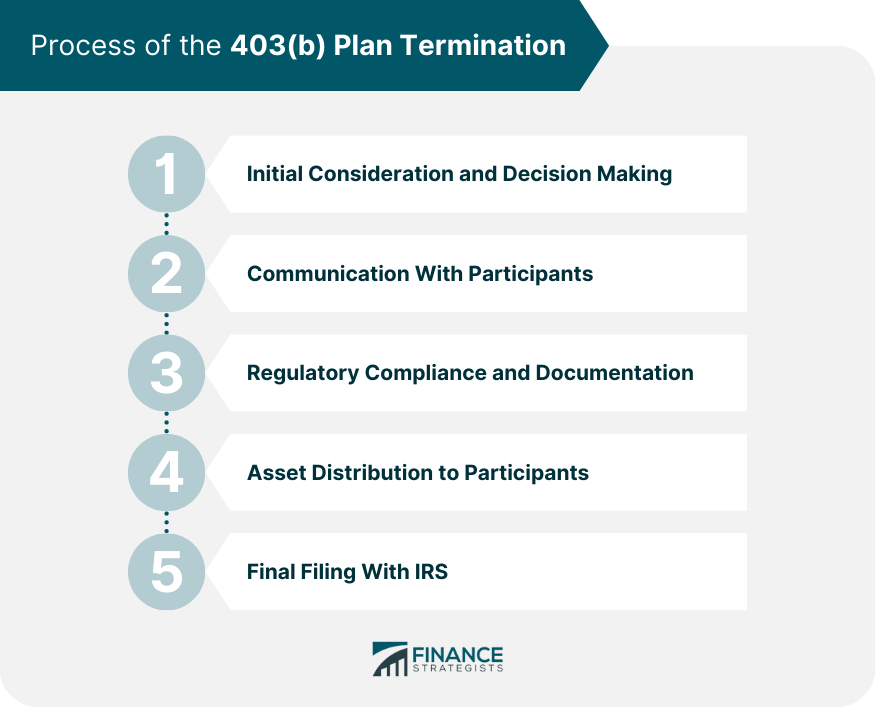

Process of the 403(b) Plan Termination

Initial Consideration and Decision Making

Communication With Participants

Regulatory Compliance and Documentation

Asset Distribution to Participants

Final Filing With IRS

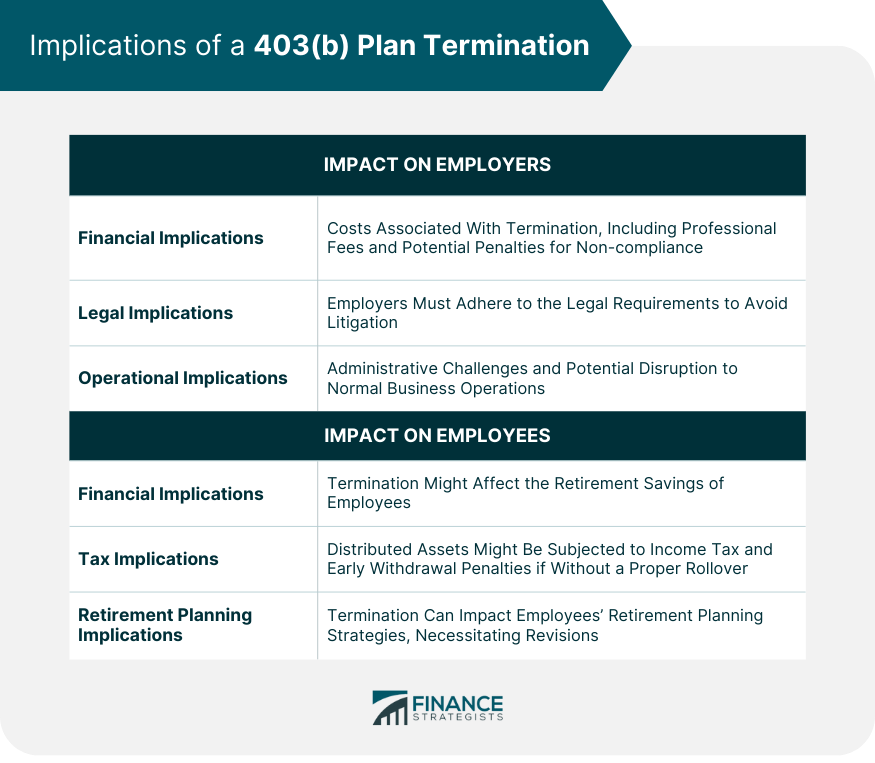

Implications of a 403(b) Plan Termination

Impact on Employers

Impact on Employees

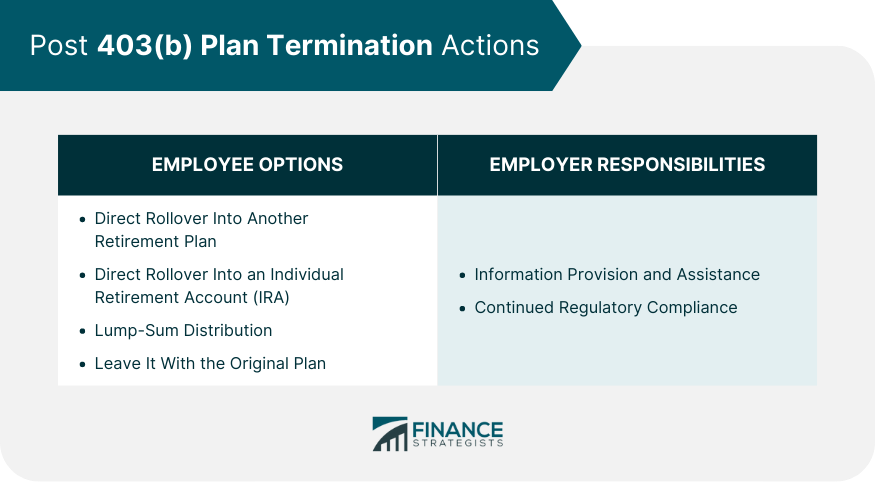

Post Termination Actions

Options for Employees

Responsibilities of Employers

This might involve arranging consultations with financial advisors or providing educational materials.

Special Considerations During a 403(b) Plan Termination

Handling of Orphaned 403(b) Plans

Possible Complications During Plan Termination

Legal Protection and Rights of Participants

Conclusion

403(b) Plan Termination FAQs

A 403(b) plan termination refers to the discontinuation of a 403(b) retirement plan typically designed for employees of public schools, certain tax-exempt organizations, and ministers. This termination may be due to organizational closure, a change in tax status, or a decision to switch to a different retirement plan.

The process involves several key steps: initial decision-making, communication with plan participants, regulatory compliance and documentation, distribution of assets to participants, and final filing with the IRS. Each step requires careful attention to ensure a smooth and compliant termination.

For employers, the termination can lead to financial costs, legal responsibilities, and operational challenges. For employees, it may impact retirement savings, lead to potential tax implications, and require changes in retirement planning strategies.

Post-termination, employees have several options such as rolling over their funds into another retirement plan or an individual retirement account (IRA), receiving a lump-sum distribution, or leaving it with the original plan in certain cases. Employers should assist employees in understanding these options and continue to comply with IRS regulations.

Special considerations during termination include handling orphaned 403(b) plans, dealing with possible complications during the process, and ensuring the legal protection and rights of plan participants. These aspects require careful management to ensure a compliant and efficient termination process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.