A qualified distribution, in essence, refers to tax-free withdrawals from certain types of retirement accounts, such as a Roth Individual Retirement Account (IRA) or a Roth 401(k). To be deemed "qualified," the distribution must meet specific criteria set by the Internal Revenue Service (IRS). This typically includes certain age or time period requirements. The financial industry is complex, and so is the terminology used. When defining a qualified distribution, it is worth noting that it applies predominantly to post-tax retirement accounts. These are accounts where contributions are made after-tax, and therefore, under the right circumstances, distributions can be made tax-free. In this way, qualified distributions can provide a tax-efficient way to access retirement savings. At this point, you might be wondering about the purpose of a qualified distribution. Why do such regulations exist in the first place? Qualified distributions serve a dual purpose. They not only offer a tax advantage to encourage long-term retirement savings, but also provide a framework to ensure these savings are used for their intended purpose - retirement. By making the distribution rules for these retirement accounts somewhat stringent, the IRS aims to deter individuals from using these funds prematurely or for non-retirement purposes. Essentially, the purpose of the qualified distribution rules is to encourage responsible retirement planning and savings habits, and to ensure the longevity of these crucial savings. A common question that arises when discussing qualified distributions is, "Which retirement accounts are eligible?" Qualified distributions can only occur from certain types of accounts. The primary accounts that allow for qualified distributions are Roth IRAs and Roth 401(k)s. Both of these accounts are funded with after-tax dollars, which means the contributions have already been taxed prior to entering the account. It's also worth noting that certain other types of accounts, such as Roth 403(b)s and Roth Thrift Savings Plans (TSPs), may also be eligible for qualified distributions. These accounts, like Roth IRAs and Roth 401(k)s, are also funded with post-tax dollars, hence, under the right circumstances, the distributions can be tax-free. The next qualification for a qualified distribution is based on age. The IRS specifies that, for a distribution to be considered qualified, the account holder must be at least 59.5 years old at the time of the distribution. This age limit is designed to ensure that the funds saved in these retirement accounts are used for their intended purpose: providing financial support during retirement. The age requirement aligns with the larger purpose of the retirement savings plan. It serves as a deterrent against early withdrawal, thereby promoting the idea of long-term savings. By setting an age limit, the IRS ensures that these retirement funds are used at the right time and for the right reason, aiding in secure and comfortable retirement years. In addition to age requirements, the IRS stipulates that a distribution can only be qualified if it occurs at least five years after the initial contribution to the Roth account. This rule, also known as the "5-year rule," applies to the tax year in which the first contribution was made. For instance, if the first contribution was made any time in 2023, the five-year period would start on January 1, 2023, and end on December 31, 2027. The 5-year rule serves as a mechanism to encourage long-term savings behavior and discourages account holders from making immediate withdrawals. The aim of this rule is to ensure the preservation of retirement savings, providing a more stable financial foundation during retirement. A Roth IRA is an individual retirement account funded with post-tax dollars, meaning that taxes are paid upfront, allowing for tax-free withdrawals during retirement under qualifying conditions. A Roth IRA distribution will be considered qualified if it meets the age and time period requirements discussed earlier. Roth IRAs offer several benefits, including tax-free growth on investments and the ability to withdraw contributions at any time without tax or penalty. This flexibility can make Roth IRAs a popular choice for individuals seeking a tax-advantaged way to save for retirement. The other primary source of qualified distributions comes from employer-sponsored retirement plans, such as Roth 401(k)s, Roth 403(b)s, and Roth TSPs. Like Roth IRAs, these plans are funded with after-tax dollars, and under the right circumstances, they allow for tax-free withdrawals during retirement. As long as the age and time period requirements are met, distributions from these accounts are considered qualified. Employer-sponsored retirement plans can be a valuable tool for retirement savings, often featuring additional benefits such as employer matching contributions. When combined with the tax advantages offered by qualified distributions, these plans can play a crucial role in achieving a comfortable retirement. One key benefit of qualified distributions is that they are exempt from the early withdrawal penalty. If a distribution from a retirement account does not meet the criteria for a qualified distribution, an early withdrawal penalty of 10% may be applied to the taxable portion of the distribution. However, if the distribution is deemed qualified, this penalty does not apply. This penalty exemption is another incentive for individuals to ensure they meet the qualifications for a qualified distribution. By doing so, they can avoid unnecessary financial burdens and make the most of their retirement savings. Understanding the taxable portion of distributions is essential for retirement planning. While qualified distributions are generally tax-free, there are some exceptions to this rule. In cases where an individual has made non-deductible contributions to a Roth account or has converted a traditional account to a Roth, a portion of the distribution may still be taxable. The specific tax treatment of these situations can be complex, so consulting a financial professional is recommended. Regardless, the majority of qualified distributions offer significant tax advantages, including tax-free growth and the ability to access retirement savings without incurring additional taxes or penalties. The tax benefits of qualified distributions are a major draw for many individuals seeking a tax-advantaged way to save for retirement. Because contributions to Roth accounts are made with after-tax dollars, the distributions are generally tax-free, as long as they meet the necessary qualifications. These tax benefits can have a substantial impact on an individual's overall retirement plan. By strategically utilizing qualified distributions, individuals can better control their taxable income in retirement, potentially lowering their overall tax burden. As discussed earlier, one of the most significant advantages of qualified distributions is tax-free growth. This means that, while the investments within the account grow, no taxes are levied on the gains. The tax-free nature of these distributions can lead to substantial savings and increased retirement income over time. Tax-free growth can provide a major benefit, especially when compared to traditional retirement accounts, where taxes are deferred until distribution. With qualified distributions, individuals can enjoy their retirement savings without worrying about additional tax burdens. Another advantage of qualified distributions is the flexibility they offer in retirement planning. Since qualified distributions are generally tax-free, they can be strategically used to control taxable income in retirement. This can be particularly beneficial for individuals seeking to minimize taxes on Social Security benefits or who wish to manage their income to remain eligible for certain tax credits or deductions. Moreover, the absence of required minimum distributions (RMDs) for Roth IRAs provides even greater flexibility, allowing account holders to withdraw funds at their discretion, rather than being forced to take distributions at a specific age. The ability to withdraw funds tax-free during retirement can lead to lower tax rates for individuals utilizing qualified distributions. This is especially advantageous for individuals who expect to be in a higher tax bracket during retirement. By making contributions with after-tax dollars and enjoying tax-free withdrawals in retirement, individuals can strategically minimize their lifetime tax burden. Although qualified distributions offer several advantages, there are some potential drawbacks to consider. One such disadvantage is the early withdrawal restrictions that come with these accounts. While contributions to a Roth IRA can be withdrawn at any time without tax or penalty, earnings within the account may be subject to taxes and penalties if withdrawn before meeting the qualifications for a qualified distribution. These restrictions may limit an individual's ability to access their retirement savings in cases of financial hardship or other unexpected expenses before reaching the age and time period requirements. Another potential disadvantage of qualified distributions is their impact on Social Security benefits. While the tax-free nature of qualified distributions can help individuals manage their taxable income in retirement, these distributions may still be considered when determining the taxability of Social Security benefits. This means that, in some cases, large qualified distributions could potentially result in a reduction of Social Security benefits due to increased income levels. To avoid this issue, careful planning and strategic withdrawal strategies may be necessary. Lastly, it is important to consider the impact of qualified distributions on eligibility for certain tax credits or deductions. Although qualified distributions are generally tax-free, they may still be factored into calculations for certain tax credits or deductions, such as the Earned Income Tax Credit or education tax credits. In some cases, this could result in a reduction or loss of these tax benefits. As with the potential reduction in Social Security benefits, careful planning and consideration of withdrawal strategies may be needed to avoid these issues. A qualified distribution is a tax-free withdrawal from specific types of retirement accounts, such as Roth IRAs or Roth 401(k)s. To be considered qualified, a distribution must meet certain age and time period requirements set forth by the IRS. These distributions offer a variety of tax advantages and can play a crucial role in retirement planning. While there are many advantages to qualified distributions, such as tax-free growth, flexibility in retirement planning, and the potential for lower tax rates, there are also some disadvantages to be aware of. These may include early withdrawal restrictions, potential reduction in Social Security benefits, and impact on eligibility for certain tax credits or deductions. Careful planning, along with consultation with a financial professional, can help individuals make the most of their retirement savings and ensure a comfortable and financially secure retirement.What Is a Qualified Distribution?

Purpose of Qualified Distributions

Qualifications for Qualified Distributions

Eligible Retirement Accounts

Age Requirements

Time Period of Participation

Types of Qualified Distributions

Roth IRA Distributions

Qualified Distributions From Employer-Sponsored Retirement Plans

Tax Treatment of Qualified Distributions

Exempt From Early Withdrawal Penalty

Taxable Portion of Distributions

Tax Benefits of Qualified Distributions

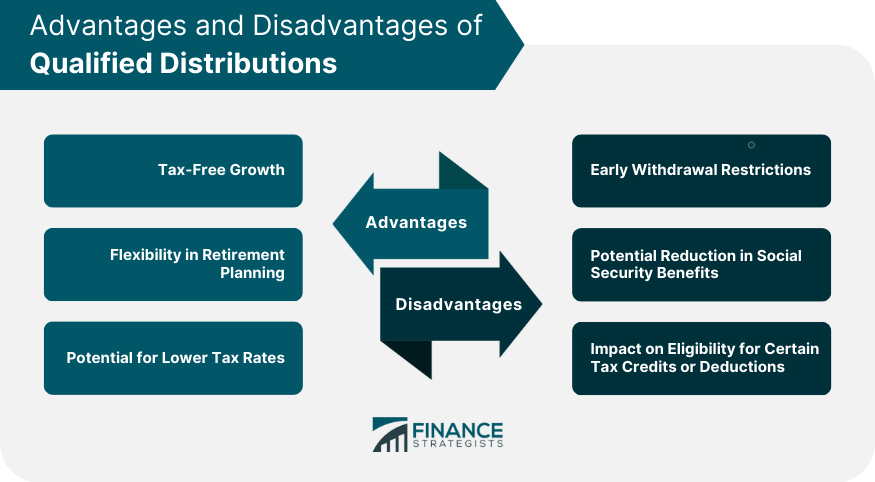

Advantages of Qualified Distributions

Tax-Free Growth

Flexibility in Retirement Planning

Potential for Lower Tax Rates

Disadvantages of Qualified Distributions

Early Withdrawal Restrictions

Potential Reduction in Social Security Benefits

Impact on Eligibility for Certain Tax Credits or Deductions

Final Thoughts

Qualified Distribution FAQs

A qualified distribution is a tax-free withdrawal from specific types of retirement accounts, such as Roth IRAs or Roth 401(k)s, that meet certain age and time period requirements set forth by the IRS.

For a distribution to be considered qualified, the account holder must be at least 59.5 years old, and the distribution must occur at least five years after the initial contribution to the Roth account.

Generally, qualified distributions are tax-free. However, there are some exceptions, such as when non-deductible contributions have been made or a traditional account has been converted to a Roth. In these cases, a portion of the distribution may still be taxable.

Some advantages of qualified distributions include tax-free growth, flexibility in retirement planning, and the potential for lower tax rates in retirement.

Disadvantages of qualified distributions may include early withdrawal restrictions, potential reduction in Social Security benefits, and impact on eligibility for certain tax credits or deductions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.