In the dynamic world of finance, bonds serve as crucial investment tools, representing loans made by investors to borrowers. On the other hand, the Federal Deposit Insurance Corporation (FDIC), a stalwart of banking stability, offers insurance to protect depositors against bank failures. The intersection of these two elements prompts an important question for investors and financial strategists: Are bonds insured by the FDIC? Understanding the relationship between bonds and FDIC insurance becomes pivotal as it forms the foundation of risk assessment and the development of robust investment strategies. Delving into this vital aspect can shed light on the risks associated with bond investing and the strategies to mitigate them, fostering a more informed and confident approach to investment decisions. Simply put, bonds are not insured by the FDIC. While the FDIC insures specific deposit accounts at FDIC-insured banks, it does not cover investment products, even if purchased from an insured bank. FDIC is an independent agency of the U.S. government that insures the deposits made by individuals and businesses into member banks. Bonds, however, are not insured by the FDIC because they are not considered deposits. Rather, bonds are considered investments, and they carry their own set of risks. When you buy a bond, you are essentially lending money to the entity issuing the bond, whether it's a corporation, a municipality, or the federal government. The issuer promises to pay you a specified rate of interest during the life of the bond and to repay the principal when the bond "matures," or comes due. The risk comes from the fact that the issuer might default, meaning they fail to pay the interest or principal as promised. The likelihood of this happening depends on the creditworthiness of the issuer. In the case of U.S. government bonds, also known as Treasury bonds, the risk of default is very low because they are backed by the full faith and credit of the U.S. government. Corporate and municipal bonds carry a higher risk, and their credit ratings are assessed by agencies like Moody's and Standard & Poor's. While the FDIC does not insure bonds, the Securities Investor Protection Corporation (SIPC) may protect customers if their brokerage firm fails. However, SIPC protection is limited and does not protect against losses due to a decline in the market value of your securities. A bond is a financial instrument representing a loan made by an investor to a borrower, typically corporate or governmental. Bonds are characterized by their face value, maturity date, coupon rate, and issuer. Various types of bonds exist, each having its unique characteristics. Key examples include: Government Bonds: These are issued by national governments. In the United States, they are referred to as Treasuries and are deemed as low-risk investments because they're backed by the full faith and credit of the U.S. government. Municipal Bonds: These are issued by states, cities, or other local entities to finance public projects. Corporate Bonds: Corporations issue these to fund business operations, expansions, or acquisitions. Agency Bonds: Government-affiliated organizations issue these. They carry a slightly higher risk than government bonds. Asset-Backed Securities: These are bonds whose interest and principal payments are backed by underlying cash flows from other assets. The FDIC is an independent agency of the United States government designed to protect consumers within the banking system. Created in 1933 following a spate of bank failures during the Great Depression, the FDIC's mission is to maintain stability and public confidence in the nation's financial system. FDIC insurance covers the depositors of a failed FDIC-insured depository institution dollar-for-dollar, including principal and any accrued interest, within the insurance limit. FDIC insurance covers all types of deposits received at an insured bank, such as: Savings accounts Money market deposit accounts Certificates of deposit It's essential to note that FDIC insurance is limited to $250,000 per depositor, per FDIC-insured bank, per ownership category. Credit risk, also known as default risk, refers to the possibility that the bond issuer will not be able to make principal and interest payments when due. Interest rate risk refers to the risk that a bond's price will decrease due to an increase in interest rates. This is a significant concern for bondholders planning to sell their bonds before maturity. Inflation risk, also known as purchasing power risk, is the risk that inflation will undermine the performance of the investment. If the rate of inflation surpasses the return on the bond, the investor's purchasing power declines. Liquidity risk is the risk that an investor may not be able to buy or sell bonds quickly without significantly affecting the bond price due to a lack of buyers or sellers. Bond ratings provide an objective evaluation of the creditworthiness of bond issuers. The main agencies that provide these ratings are Moody's, Standard & Poor's, and Fitch Ratings. These ratings influence the interest rate that firms must pay to attract investors. A high bond rating, typically at 'AAA' or 'Aaa', indicates a low credit risk, translating into lower interest rates for the bond issuer. Conversely, a lower bond rating means a higher credit risk, necessitating higher interest rates to attract investors. Bond insurance guarantees that even if the bond issuer defaults, scheduled payments of interest and the principal on the bond will still be made to the bondholders. This insurance is typically taken by corporate and municipal bond issuers to enhance their creditworthiness. Bond insurance mitigates the credit risk associated with a bond investment. By ensuring that payments will be made, insurance helps keep the bond's value stable, making it more attractive to potential investors. The Securities Investor Protection Corporation (SIPC) is a nonprofit corporation created by Congress to protect customers if a brokerage firm fails. Unlike FDIC insurance, SIPC does not insure against losses due to market fluctuations. It instead aims to restore customer funds and securities left in the hands of bankrupt or financially troubled brokerage firms. While the FDIC covers deposit account losses due to a bank failure, SIPC protects against the loss of cash and securities – such as stocks and bonds – held by a customer at a financially troubled SIPC-member brokerage firm. Neither insures against market losses. Diversification is an investment strategy that involves spreading investments among different types of assets (stocks, bonds, cash, etc.) to reduce exposure to any single asset or risk. The theory is that a diversified portfolio will, on average, yield higher returns and pose a lower risk than any single investment. Asset allocation involves distributing an investor's portfolio across different asset classes such as bonds, stocks, and cash. This strategy aims to balance risk and reward by adjusting the portfolio's percentage of each asset class according to the investor's risk tolerance, goals, and investment time frame. The bond market is regulated to maintain fair dealing and transparency. The key regulators include the Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA), and the Municipal Securities Rulemaking Board (MSRB). Regulatory bodies set rules and standards to promote transparency, integrity, and fairness in the bond market. These rules cover areas like disclosure requirements, trade reporting, market practices, and professional conduct, protecting investors from fraudulent activities and market manipulation. By enforcing these regulations, these bodies ensure that the bond market operates in a fair and orderly manner. While bonds represent valuable financial instruments for investors, they are not insured by the FDIC. This is because they are classified as investments rather than deposits, subjecting them to a variety of risks such as credit, interest rate, inflation, and liquidity risk. The risk associated with bonds can be mitigated through several strategies such as purchasing bond insurance, diversifying investments, following asset allocation principles, and closely adhering to bond ratings provided by reputable agencies. To navigate these complexities and manage the inherent risks in bond investing, it is highly recommended to seek professional guidance. Wealth management services can provide invaluable assistance in this regard, offering comprehensive financial planning and investment strategies tailored to individual financial goals and risk tolerance. A wealth manager can help assess the viability of bonds in your investment portfolio, alongside other asset classes, to optimize returns while effectively managing potential risks.Bonds and FDIC Insurance: An Intersection in Financial Strategy

Are Bonds Insured by the FDIC?

Bonds Are Not Insured by the FDIC

Reasons Why FDIC Doesn't Insure Bonds

Understanding Bonds and FDIC Insurance

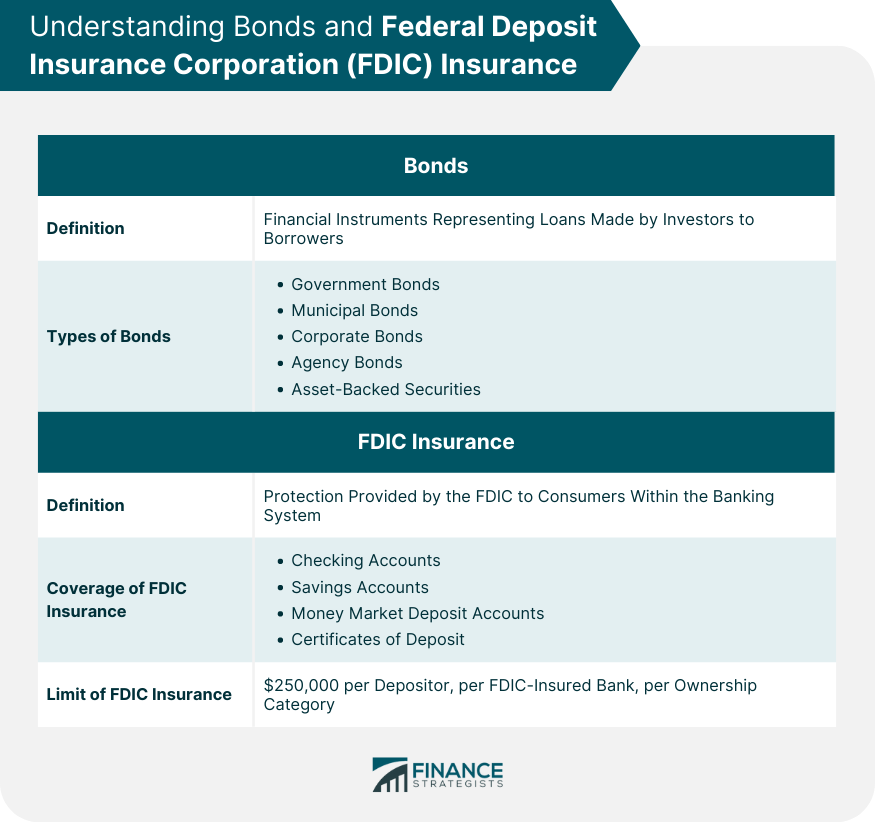

Bonds

Types of Bonds

FDIC Insurance

What FDIC Insurance Covers

Risks and Safeguards of Investing in Bonds

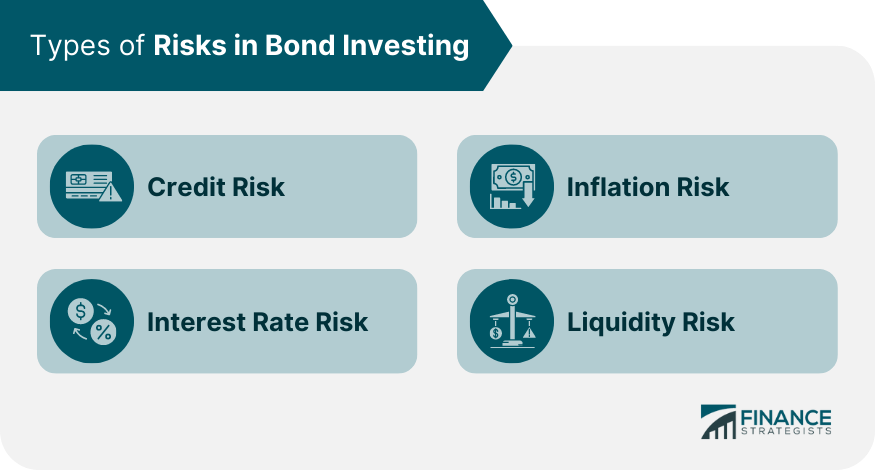

Types of Risks in Bond Investing

Credit Risk

Interest Rate Risk

Inflation Risk

Liquidity Risk

Understanding Bond Ratings

Purpose and Agencies That Issue Bond Ratings

How Bond Ratings Impact Risk and Return

Bond Insurance

Other Methods of Protection for Investors

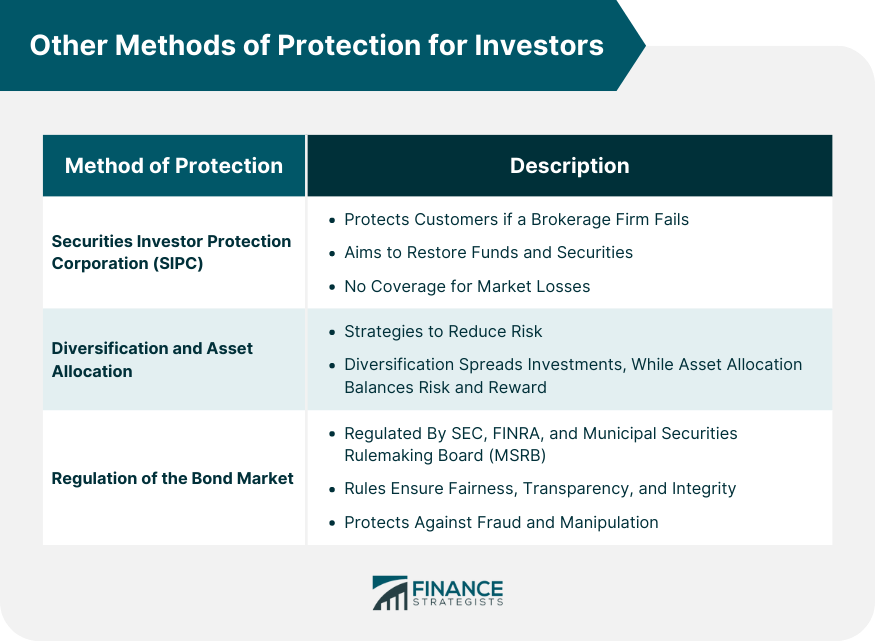

Securities Investor Protection Corporation (SIPC)

Diversification and Asset Allocation

Regulation of the Bond Market

Bottom Line

Are Bonds Insured by the FDIC? FAQs

No, bonds are not insured by the FDIC. The FDIC only insures deposit accounts like checking and savings accounts at FDIC-insured banks, not investment products like bonds.

The FDIC doesn't insure bonds because they are investment products and inherently carry risks from market fluctuations. The FDIC's purpose is to protect depositors against losses from bank failures, not market losses.

Yes, some bond issuers purchase bond insurance, which guarantees payment of the principal and interest to bondholders if the issuer defaults.

Regulators such as the SEC and FINRA protect bond investors by enforcing rules and standards for transparency and fair dealing. Additionally, the SIPC can protect against the loss of cash and securities at a financially troubled brokerage firm.

Understanding the issuer's creditworthiness (via bond ratings), diversifying your investments, and employing strategic asset allocation can help mitigate the risks associated with bond investing. You might also consider bond insurance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.