An Original Issue Discount (OID) is a unique financial concept that arises when a bond or other debt instrument is issued for a price lower than its par (face) value. The OID represents the difference between the issue price and the bond's redemption value at maturity. The bond issuer effectively offers a discount to incentivize investors to purchase the bond. Over time, the investor gradually earns this discount as it accretes towards its face value, providing a form of interest. OID has been a significant part of the bond market since its inception, often used by corporations, governments, and municipalities as a financing tool. The practice became more regulated with the introduction of the Tax Reform Act of 1986 in the United States, which established rules for the taxation of the income earned from OID bonds. The calculation of OID involves determining the difference between the stated redemption price at maturity and the issue price. Redemption Price: This refers to the face value of the bonds, which is the amount set to be repaid on the maturity date. Issuance Price: This denotes the initial price at which the bonds were marketed and sold on their sale date. For instance, if a bond with a face value of $1,000 is issued for $900, the OID is $100. Using an accretion method, the bondholder then recognizes this amount as income over the bond's life. The yield on a bond with OID is generally higher than that of a bond issued at par. This is because the investor purchases the bond at a discount but receives the full face value at maturity. The difference between the discounted purchase price and the face value is effectively additional interest, increasing the bond yield. Suppose a 5-year zero-coupon bond with a face value of $1,000 is issued for $800. The OID is $200. This amount is then recognized as income over the five years. If we use straight-line accretion, the investor would recognize $40 ($200/5 years) as interest income each year, regardless of the bond's cash flow. An important aspect of OID is its tax implications. In the eyes of tax authorities, such as the Internal Revenue Service (IRS) in the United States, OID is treated as interest income. This means that bondholders must pay income tax on the OID amount even though they receive the cash once the bond matures. Investors must understand this tax obligation when considering an investment in OID bonds. OID is reported annually as it accrues, not when the bondholder receives the cash payment at the bond's maturity. This concept is known as the accrual method of accounting. The IRS provides Form 1099-OID for issuers to report the annual accrual of OID. The bondholder is responsible for reporting this as interest income on their tax return. The taxation of OID has some unique exceptions and special cases. Key variations include: US Savings Bonds: These bonds often carry different OID taxation rules, deviating from the typical accrual method. This is due to their special status and purpose of promoting savings among U.S. citizens. Tax-Exempt Municipal Bonds: Due to their tax-exempt status, municipal bonds can have different OID taxation rules. The interest earned from these bonds is usually exempt from federal income tax and potentially state and local taxes, depending on the investor's state of residence. Short-Term Bonds: Bonds with a maturity date of one year or less from the issue date are not subject to the standard OID rules. These are often treated differently due to their brief term, with taxation typically applied only upon redemption or sale rather than annually. If an OID bond is sold on the secondary market before it matures, the seller must recognize as income the portion of the OID that has accrued while they held the bond. Any gain or loss on the sale of the bond is considered a capital gain or loss. For a buyer purchasing an OID bond on the secondary market, the tax implications depend on the purchase price. The buyer could have OID income if the bond were purchased at a price less than its adjusted issue price. If the bond was bought at a price greater than its adjusted issue price, the buyer has a bond premium, which can be used to offset OID income. The OID mechanism has various implications, from how the yield is affected to tax obligations and secondary market considerations. These need to be understood before investing in or issuing such bonds. OID is intrinsically linked with zero-coupon bonds. A zero-coupon bond is a bond that does not make periodic interest payments. Instead, it's sold at a discount to its face value, and maturity, the bondholder receives the face value of the bond. All zero-coupon bonds are OID bonds, but not all OID bonds are zero-coupon bonds. While both OID bonds and zero-coupon bonds are sold at a discount, the discount treatment is slightly different. The discount is considered a capital gain for OID bonds, whereas, for zero-coupon bonds, the discount is considered interest income. The tax implications are also different, with zero-coupon bonds being taxed on the accrued interest each year, even though no cash is received until maturity. OID bonds, like all securities, are subject to securities laws. In the United States, this primarily means the Securities Act of 1933, the Securities Exchange Act of 1934, and any related rules and regulations promulgated by the Securities and Exchange Commission (SEC). Securities laws often require issuers to provide extensive disclosures about their financial condition and the specific terms of their bonds. This includes providing information about the OID and how it impacts the bond yield. These disclosure requirements aim to ensure that investors have all the information they need to make informed investment decisions. Securities laws also contain anti-fraud provisions that prohibit issuers and others from misleading investors about the nature of the bonds. This means that issuers must accurately represent the OID and how it affects the return on the bond. Issuers of OID bonds have specific compliance requirements to meet. These requirements can include filing appropriate forms with the SEC, providing ongoing disclosures to investors, and adhering to any restrictions on how and to whom the bonds can be sold. In many cases, issuers must file a registration statement with the SEC before issuing the bonds. This statement includes detailed information about the issuer and the bonds, including the OID. Once the bonds are issued, the issuer often must provide ongoing disclosures to investors. This can include annual and quarterly financial statements and immediate disclosure of any material events that could impact the value of the bonds. In some cases, there may be restrictions on how and to whom the issuer can sell the bonds. For example, some bonds may only be sold to "accredited investors," a category of investors who meet specific income or net worth criteria. OID can play a strategic role in a company's capital structure. By issuing bonds at a discount, companies can defer the cash outflow related to interest payments until the bond's maturity, which can be beneficial for managing cash flow. However, this comes with a trade-off, as the company will need to pay a higher effective interest rate to compensate investors for the deferred payments. Corporate bond issuance is an integral part of many companies' funding strategies, and OID bonds can make this issuance more attractive to potential investors. By offering bonds at a discount, companies can appeal to investors who are looking for a higher yield, making it easier for the company to raise capital. Investing in OID bonds carries both potential benefits and risks. On the one hand, the appeal of these bonds largely lies in their high yield, resulting from the discount at which they are issued. They can also offer a predictable income stream, as the amount to be received at maturity is known from the onset. However, the key risk with OID bonds is the tax treatment. Investors must pay tax on the imputed interest each year, even though they receive the actual cash once the bond matures. This requires careful tax planning and sufficient cash reserves to cover the tax liability. In terms of portfolio management, OID bonds can provide diversification. They can also serve as a hedge against interest rate risk since the total return is known at the time of purchase, making them less susceptible to price fluctuations due to changes in interest rates. However, given their unique tax implications, they should be used strategically within a portfolio. The treatment of OID varies globally. While the U.S. treats OID as taxable income annually, other jurisdictions may have different rules. For example, some countries may only tax the discount when it is realized at the bond's maturity. Thus, international investors must understand the tax implications in their respective jurisdictions. In terms of financial reporting, the International Financial Reporting Standards (IFRS) have specific guidelines for accounting for OID. Under IFRS, OID is typically amortized over the bond's life using the effective interest method, which distributes the interest income more evenly than the straight-line method. OID is a powerful financial concept and an important part of the bond market. It refers to the difference between the face value of a bond and its issue price, providing a form of interest that accrues over the bond's life. Understanding OID's mechanics, tax implications, and legal aspects is crucial for both issuers and investors. The OID market is complex and multifaceted, shaped by various factors, including financial regulations, technological advancements, and international accounting standards. Investors considering OID bonds should assess their potential return, their tax implications, and the broader market context. Investing in OID bonds can be a wise decision but requires careful planning and expert advice. Therefore, consulting with a wealth management advisor can help you navigate the complexities of OID and align your investments with your financial goals.What Is an Original Issue Discount (OID)?

Mechanics of Original Issue Discounts

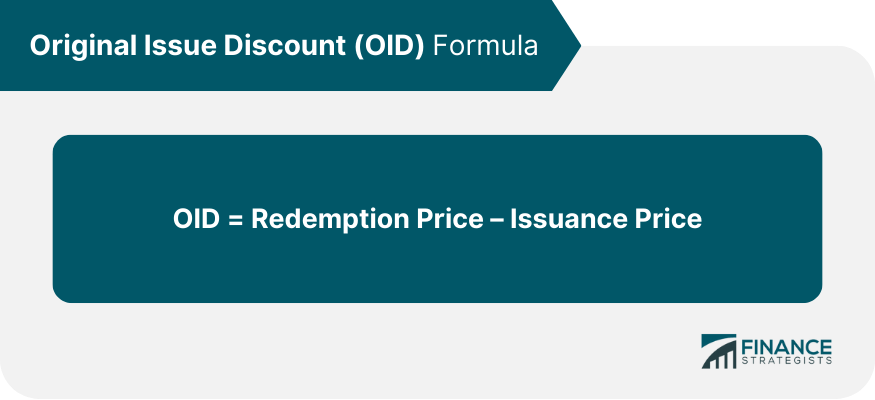

Formula and Calculation of OID

Effect on the Yield of the Bond

Example of OID Calculation

Original Issue Discounts and Tax Implications

OID as Income

Tax Reporting of OID

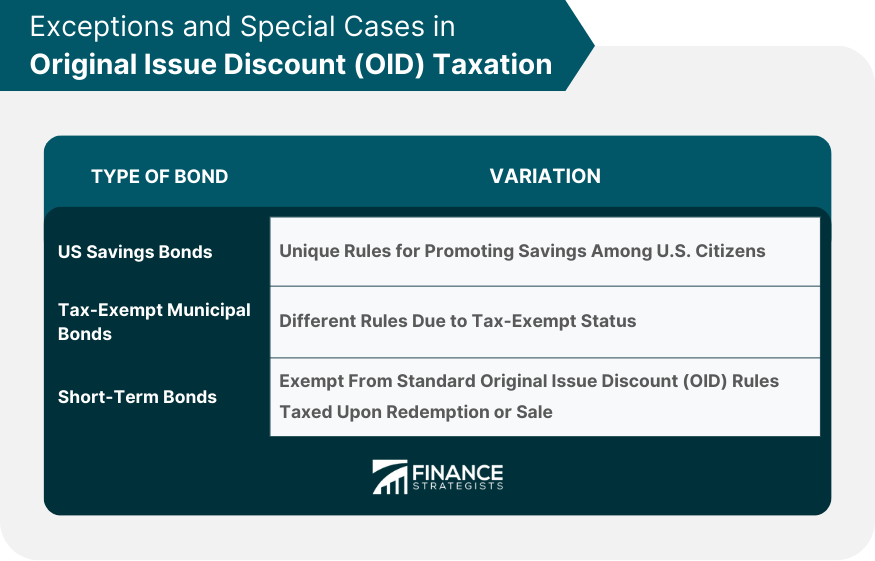

Exceptions and Special Cases in OID Taxation

Original Issue Discounts and the Secondary Market

Original Issue Discounts and Zero-Coupon Bonds

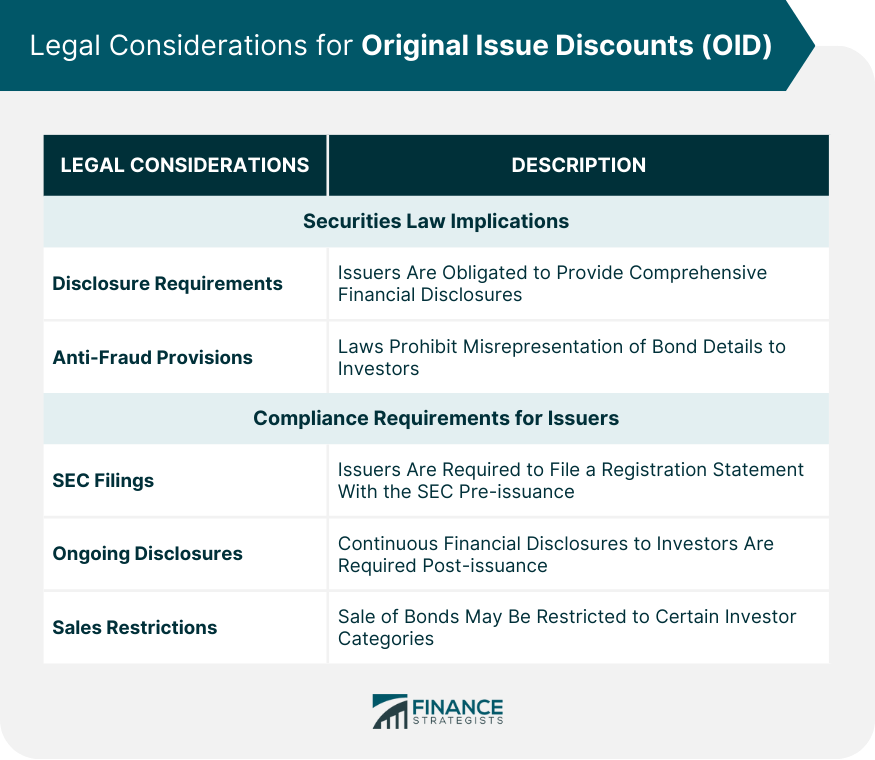

Legal Considerations for Original Issue Discounts

Securities Law Implications

Disclosure Requirements

Anti-fraud Provisions

Compliance Requirements for Issuers

SEC Filings

Ongoing Disclosures

Sales Restrictions

Role of Original Issue Discounts in Corporate Finance

Strategic Use of OID in Capital Structure

OID and Corporate Bond Issuance

Original Issue Discounts and Personal Investment Strategies

Risks and Benefits for Individual Investors

Considerations in Portfolio Management

Original Issue Discounts in the International Context

Comparison of OID Treatment in Different Jurisdictions

Impact of International Financial Reporting Standards (IFRS) on OID

Final Thoughts

Original Issue Discount (OID) FAQs

Regular bonds are issued at their face value and pay periodic interest, also known as coupons, to the bondholders. On the other hand, OID bonds are issued at a discount to their face value and do not pay periodic interest. Instead, the interest is effectively included in the redemption price received at maturity.

Yes, but it depends on the specific tax laws applicable to the investor. In some cases, OID can provide a tax advantage if the bondholder is in a lower tax bracket when they recognize OID income compared to the year the bond matures. However, because tax laws are complex and vary widely, it's crucial to seek professional tax advice when investing in OID bonds.

While all zero-coupon bonds can be considered OID bonds, not all OID bonds are zero-coupon bonds. Zero-coupon bonds do not make any interest payments over their life, and the entire return to the investor comes from the discount at which the bond is issued. In contrast, an OID bond can have some coupon payments in addition to the discount at issuance.

Like any bond, the risk of an OID bond is primarily determined by the issuer's creditworthiness. However, OID bonds do carry additional risks, such as reinvestment risk, because they don't make periodic interest payments. Furthermore, they also have unique tax implications that can impact the bondholder's return.

If an OID bond is sold in the secondary market before maturity, the original owner must recognize as income the OID that has accrued during the period they held the bond. The new owner will then start accruing OID from the price they paid to purchase the bond.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.