Interest rate risk refers to the potential for financial losses due to changes in interest rates. It can affect a firm's profitability and the value of its assets and liabilities. Banks, financial institutions, and non-financial firms all face interest rate risk. Fluctuations in interest rates can lead to changes in the value of interest-sensitive assets and liabilities, which can impact the company's net interest income and overall financial stability. Managing interest rate risk is crucial for the financial stability of companies and the economy as a whole. Effective management of this risk can help firms maintain profitability and protect the value of their assets and liabilities. By effectively managing interest rate risk, firms can better cope with changes in market conditions, reduce their exposure to potential losses, and ensure the long-term success of their business operations. There are various types of interest rate risk that firms need to consider when managing their financial risks. These risks can arise from mismatches in the repricing of assets and liabilities, changes in the shape of the yield curve, and other factors. Repricing risk is the risk of changes in interest rates affecting the net interest income of a firm. This risk arises when there is a mismatch between the repricing of assets and liabilities, which can lead to fluctuations in net interest income. For example, if a bank has more liabilities repricing in the short term compared to its assets, it faces the risk that an increase in interest rates will lead to higher interest expenses without a corresponding increase in interest income. This can result in reduced profitability and financial stability. Yield curve risk refers to the potential for losses resulting from changes in the shape of the yield curve, which represents the relationship between interest rates and the time to maturity of financial instruments. This risk can affect the value of a firm's interest-sensitive assets and liabilities. A change in the yield curve's shape, such as a flattening or steepening, can affect the relative values of assets and liabilities with different maturities. This can lead to changes in the firm's net interest income and potentially result in financial losses. Basis risk is the risk that arises when the interest rates of different financial instruments or indexes do not move in perfect correlation. This risk can affect firms that use hedging strategies to manage their interest rate risk. For instance, a firm may use interest rate swaps to hedge its exposure to fluctuations in interest rates. However, if the reference rates used in the swap agreement do not move in perfect correlation with the firm's actual interest rate exposure, it may still face financial losses due to basis risk. Optionality risk is the risk associated with embedded options in financial instruments, such as callable bonds or mortgages with prepayment options. The presence of these options can affect the value of the instrument and create uncertainty regarding future cash flows. For example, if interest rates decline, borrowers may choose to prepay their mortgages, causing the lender to receive lower interest income than anticipated. This can lead to financial losses for the lender and impact the overall value of its interest-sensitive assets. Measuring and assessing interest rate risk is essential for effective risk management. Various methods can be used to quantify the potential impact of interest rate fluctuations on a firm's financial position and performance. Gap analysis is a commonly used method for measuring interest rate risk. It involves comparing the repricing of assets and liabilities within specified time periods, which helps identify potential mismatches that could affect a firm's net interest income. Using gap analysis, firms can assess their exposure to repricing risk and develop strategies to mitigate the potential impact of interest rate changes. However, this method may not fully capture the complexity of a firm's interest rate risk exposure, particularly when considering yield curve risk and optionality risk. Duration analysis is another method for assessing interest rate risk, focusing on the sensitivity of a firm's assets and liabilities to changes in interest rates. Duration measures the weighted average time until an instrument's cash flows are received, which can help estimate the potential impact of interest rate changes on the value of assets and liabilities. By comparing the duration of assets and liabilities, firms can gauge their exposure to interest rate risk and develop strategies to manage this risk, such as duration matching. However, duration analysis may not fully capture the effects of non-parallel shifts in the yield curve or the impact of embedded options. Simulation analysis involves using computer models to estimate the potential impact of various interest rate scenarios on a firm's financial position and performance. This method can help firms assess their exposure to different types of interest rate risk, including repricing risk, yield curve risk, and optionality risk. By simulating the potential impact of interest rate changes under various scenarios, firms can better understand their interest rate risk exposure and develop appropriate risk management strategies. However, the accuracy of simulation analysis depends on the quality of the underlying models and assumptions. Value at Risk (VaR) is a statistical technique used to estimate the potential losses a firm could incur due to changes in market factors, including interest rates. VaR calculates the maximum potential loss a firm could experience within a specified time period and confidence level. Using VaR, firms can quantify their interest rate risk exposure and develop strategies to manage this risk. However, VaR has limitations, as it may not fully capture the potential losses in extreme market events and may underestimate the tail risk associated with interest rate fluctuations. Firms can employ various techniques to manage their interest rate risk exposure, including asset and liability management (ALM), hedging strategies, diversification, and duration matching. ALM is a comprehensive approach to managing a firm's interest rate risk by aligning the maturities and repricing characteristics of its assets and liabilities. This approach aims to maintain a balance between interest-sensitive assets and liabilities, which can help mitigate the impact of interest rate changes on net interest income and the firm's financial stability. By effectively managing their assets and liabilities, firms can reduce their exposure to interest rate risk and maintain profitability in various interest rate environments. However, ALM may be challenging for firms with complex financial structures or limited access to suitable financial instruments. Interest rate hedging strategies involve the use of financial instruments, such as interest rate swaps, futures and options, to mitigate the potential impact of interest rate changes on a firm's financial position and performance. For example, a firm might enter into an interest rate swap to convert its floating-rate liabilities to fixed-rate liabilities, which can help reduce its exposure to fluctuations in interest rates. By using hedging strategies, firms can manage their interest rate risk more effectively, but these strategies may involve additional costs and complexities. Diversification involves spreading a firm's investments across a range of assets and liabilities with different interest rate sensitivities, which can help reduce the overall exposure to interest rate risk. By diversifying their portfolios, firms can better manage the potential impact of interest rate changes on their financial position and performance. For instance, a firm might invest in a mix of fixed-rate and floating-rate instruments to balance its interest rate risk exposure. Diversification can help firms manage interest rate risk more effectively, but it may not entirely eliminate the risk and may require additional resources to implement and maintain a diversified portfolio. Duration matching involves aligning the duration of a firm's assets and liabilities to reduce its sensitivity to interest rate fluctuations. By matching the duration of interest-sensitive assets and liabilities, firms can minimize the potential impact of interest rate changes on the value of their portfolios. This strategy can be particularly useful for financial institutions, such as banks and insurance companies, which often have significant interest rate risk exposure due to the nature of their business activities. However, achieving perfect duration matching can be challenging, and this strategy may not fully address other types of interest rate risk, such as yield curve risk and optionality risk. Regulatory frameworks and supervisory authorities play a crucial role in ensuring that firms effectively manage their interest rate risk exposure. This section will discuss the regulatory framework, the role of central banks and supervisory authorities, and the Basel III framework's impact on interest rate risk management. The regulatory framework for interest rate risk management consists of rules, guidelines, and standards that govern the management of interest rate risk by financial institutions and other firms. This framework aims to ensure that firms effectively manage their interest rate risk exposure, maintain financial stability, and protect the interests of their stakeholders. Regulatory frameworks vary across jurisdictions but typically include requirements for capital adequacy, risk management processes, and reporting of interest rate risk exposures. Compliance with these regulations is essential for firms to maintain their financial stability and meet their regulatory obligations. Central banks and supervisory authorities play a critical role in overseeing the management of interest rate risk by financial institutions and other firms. They are responsible for setting regulatory standards, monitoring compliance, and taking corrective actions when necessary to maintain financial stability and protect the interests of stakeholders. These authorities may use various tools to supervise and regulate interest rate risk management, including on-site examinations, off-site monitoring, and the analysis of financial reports. Effective supervision and regulation of interest rate risk management can help maintain the stability of the financial system and promote sound risk management practices among firms. Basel III is an international regulatory framework that aims to enhance the resilience of the banking sector by strengthening capital and liquidity requirements and improving risk management practices. One of the key components of Basel III is the management of interest rate risk in the banking book (IRRBB), which addresses the potential impact of interest rate fluctuations on a bank's earnings and economic value. Under Basel III, banks are required to assess their IRRBB exposure using various methods, such as gap analysis, duration analysis, and stress testing. They must also maintain adequate capital buffers to cover potential losses arising from interest rate risk. Compliance with these requirements can help banks manage their interest rate risk more effectively and maintain financial stability in the face of changing market conditions. While interest rate risk is particularly relevant for financial institutions, non-financial firms also face exposure to this risk. This section will discuss the impact of interest rate risk on non-financial firms and how they can manage their exposure. Non-financial firms can be exposed to interest rate risk through various channels, such as the cost of borrowing, the value of their investments, and the impact of interest rate changes on their customers and suppliers. Changes in interest rates can affect a non-financial firm's profitability, cash flow, and financial stability, making it essential for these firms to manage their interest rate risk effectively. For example, a rise in interest rates can increase a firm's borrowing costs, reduce the value of its interest-sensitive assets, and affect the demand for its products and services. By understanding their exposure to interest rate risk, non-financial firms can develop strategies to mitigate the potential impact of interest rate fluctuations on their operations. Non-financial firms can employ various techniques to manage their interest rate risk exposure, including adjusting the maturity structure of their debt, using interest rate hedging instruments, and diversifying their investments and funding sources. For instance, a non-financial firm might issue long-term fixed-rate debt to lock in borrowing costs and reduce its exposure to fluctuations in interest rates. Alternatively, it might use interest rate swaps, futures, or options to hedge its interest rate risk and protect its financial position from potential interest rate changes. By adopting effective interest rate risk management practices, non-financial firms can maintain their financial stability and support their long-term business objectives. Interest rate risk is an essential aspect of financial management that affects both financial and non-financial firms. By understanding the types of interest rate risk, measuring and assessing their exposure, and implementing effective risk management techniques, firms can better manage the potential impact of interest rate fluctuations on their operations. In the future, technological advances and new financial instruments may offer additional opportunities for firms to manage their interest rate risk more effectively. However, firms will also need to stay abreast of regulatory developments and evolving market conditions to ensure they maintain effective risk management practices and achieve long-term financial stability.Definition of Interest Rate Risk

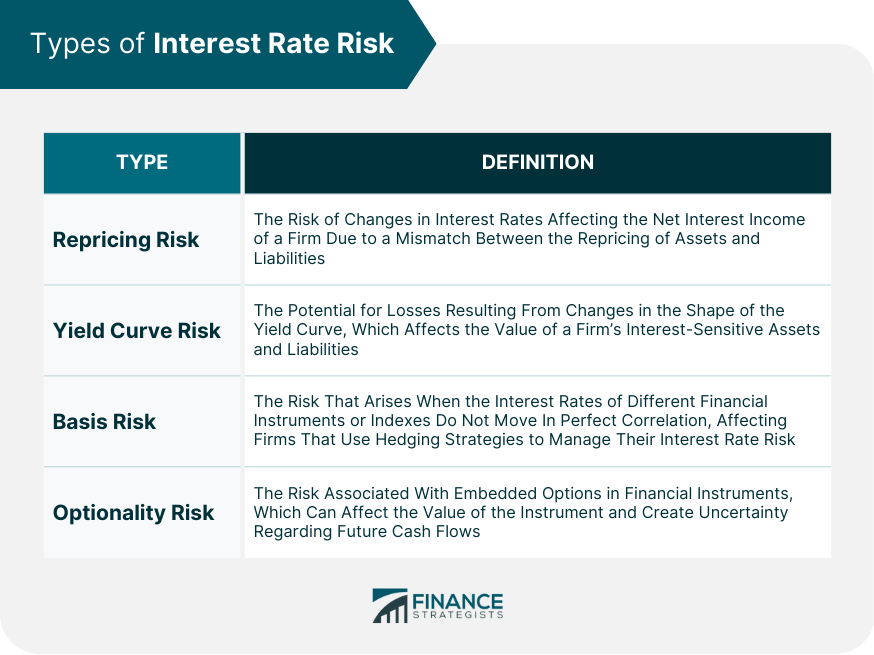

Types of Interest Rate Risk

Repricing Risk

Yield Curve Risk

Basis Risk

Optionality Risk

Measurement and Assessment of Interest Rate Risk

Gap Analysis

Duration Analysis

Simulation Analysis

Value at Risk

Interest Rate Risk Management Techniques

Asset and Liability Management

Interest Rate Hedging Strategies

Diversification of Assets and Liabilities

Duration Matching

Interest Rate Risk Regulation and Supervision

Regulatory Framework

Role of Central Banks and Supervisory Authorities

Basel III and Interest Rate Risk in the Banking Book (IRRBB)

Interest Rate Risk in Non-Financial Firms

Interest Rate Exposure in Non-Financial Firms

Managing Interest Rate Risk in Non-Financial Firms

Conclusion

Interest Rate Risk FAQs

Interest rate risk is the potential for a change in interest rates to negatively impact the value of an investment or asset.

There are two main types of interest rate risk: 1) price risk, which affects the market value of fixed-income securities, and 2) reinvestment risk, which affects future returns on fixed-income securities.

Interest rate risk can be measured using various methods such as duration, convexity, and value at risk (VaR).

Some strategies to manage interest rate risk include diversification, asset-liability management (ALM), interest rate swaps, and hedging.

Investors and financial institutions such as banks and insurance companies are most affected by interest rate risk as they hold significant amounts of fixed-income securities. However, interest rate risk can also impact individuals who hold bonds or have variable rate loans.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.