Default risk, also known as credit risk, is the probability that a borrower will be unable to fulfill their financial obligations, such as repaying a loan or making scheduled interest payments. It is a fundamental consideration in the lending process, as it directly impacts the decision-making of lenders and the availability of credit to borrowers. When lenders extend credit to borrowers, they take on the risk that the borrower may default on their obligations. To mitigate this risk, lenders assess the creditworthiness of potential borrowers before approving loans or extending credit. This assessment involves evaluating various factors, including the borrower's credit history, income, financial stability, and ability to repay the loan. By understanding the default risk associated with each borrower, lenders can make informed decisions about whether to approve or deny credit applications and determine the appropriate interest rates and terms for approved loans. Credit History: Credit history is a record of a borrower's past debt repayments and credit usage. A strong credit history indicates a lower likelihood of default, while a poor history may signal a higher default risk. Debt-to-Income Ratio: Debt-to-income (DTI) ratio measures a borrower's total debt relative to their income. A higher DTI ratio implies a greater risk of default, as the borrower may struggle to meet their debt obligations. Financial Stability: A borrower's financial stability, including their assets and liabilities, influences their ability to repay debt. Greater financial stability reduces default risk, while instability increases it. Employment Status: Employment status is a key determinant of a borrower's income stability. Stable employment reduces default risk, while unemployment or frequent job changes increase the likelihood of default. Loan Amount: The loan amount is the principal sum borrowed. Larger loans typically carry higher default risk, as the borrower may struggle to meet higher repayment obligations. Interest Rate: Interest rates are the cost of borrowing money. Higher interest rates increase default risk, as they raise the cost of debt servicing for the borrower. Loan Term: The loan term is the period over which the loan is repaid. Longer loan terms increase default risk, as the borrower's financial situation may change unfavorably over time. Collateral: Collateral is an asset pledged by the borrower to secure the loan. Loans with collateral generally have lower default risk, as the lender can seize the asset if the borrower defaults. Economic Conditions: General economic conditions, such as GDP growth and unemployment rates, influence default risk. Adverse economic conditions can increase default risk, as borrowers may struggle financially. Industry Performance: Industry performance affects the financial health of borrowers in that industry. A struggling industry may lead to higher default risk for borrowers within that sector. Regulatory Environment: Regulations in the financial sector can impact default risk. Strict regulations may reduce default risk by promoting responsible lending practices, while lax regulations may increase risk. Political Stability: Political stability influences the overall economic environment and investor confidence. Political instability can increase default risk, as it may lead to economic uncertainty and negatively affect borrowers. Credit rating agencies (CRAs) assess the creditworthiness of borrowers and assign credit ratings. These ratings help lenders and investors gauge the default risk associated with a particular borrower or security. CRAs use various methodologies to assess default risk, including quantitative and qualitative factors. These methodologies are designed to provide a comprehensive evaluation of a borrower's creditworthiness. CRAs have faced criticism for their role in financial crises and potential conflicts of interest. Concerns include the accuracy of their ratings, potential biases, and the lack of competition in the rating industry. Various types of credit scoring models exist, such as logistic regression, decision trees, and machine learning algorithms. Each model uses different techniques to predict the probability of default based on borrower-specific factors. Internal credit scoring models rely on multiple data sources, including credit history, financial statements, and demographic information. The accuracy and comprehensiveness of the data sources are crucial for effective default risk assessment. Predictive analytics involves using historical data and statistical techniques to forecast future default probabilities. This enables lenders to identify high-risk borrowers and make informed lending decisions. Evaluating the management quality of a borrower, especially in the case of corporate borrowers, provides insight into their ability to navigate financial challenges. Experienced and competent management teams can mitigate default risk through effective decision-making. Assessing the industry outlook helps lenders understand the future prospects and potential risks facing borrowers. A positive industry outlook may lower default risk, while a negative outlook can increase the likelihood of default. Analyzing a borrower's competitive position within their industry helps determine their ability to withstand market fluctuations. A strong competitive position can reduce default risk, while a weak position may increase the likelihood of default. Diversification involves spreading risk across a portfolio of loans, reducing the impact of individual defaults. Lenders can diversify by lending to borrowers from different industries, regions, or with varying credit profiles. Collateral reduces default risk by providing lenders with an asset to seize if the borrower defaults. This security decreases the lender's potential losses and encourages responsible borrowing behavior. Guarantees involve a third party, such as a government agency or another company, agreeing to cover the borrower's debt in case of default. This reduces default risk for the lender and increases the borrower's access to credit. Credit default swaps (CDS) are financial instruments that allow lenders to transfer default risk to another party. By purchasing a CDS, the lender can protect themselves from potential losses, while the seller of the CDS assumes the default risk. Loan covenants are contractual agreements between lenders and borrowers that set specific conditions and restrictions on the borrower. These covenants can help minimize default risk by ensuring the borrower maintains a certain level of financial stability. Loan renegotiation involves modifying the terms of a loan to help a struggling borrower avoid default. This process can include extending the loan term, lowering interest rates, or providing payment holidays. Debt collection strategies are employed by lenders to recover outstanding debts from borrowers who have defaulted. These strategies may involve legal actions, debt restructuring, or engaging collection agencies to pursue repayment. Lenders charge higher interest rates to compensate for higher default risk, which can lead to increased borrowing costs for riskier borrowers and influence overall credit market dynamics. Lenders consider default risk when approving loans, often denying credit to high-risk borrowers or imposing stricter lending conditions to minimize potential losses. Lenders must actively manage their loan portfolios to minimize default risk and maintain financial stability. This includes monitoring borrower performance, adjusting lending policies, and implementing risk mitigation strategies. Default risk affects borrowers' access to credit, with high-risk borrowers facing limited credit availability or higher borrowing costs due to perceived risk. Borrowers with higher default risk may face higher borrowing costs, such as increased interest rates or fees, reflecting the lender's need to compensate for potential losses. This can impact the borrower's overall financial situation and affordability of credit. Understanding and managing default risk is essential for borrowers' financial planning. By improving creditworthiness and minimizing default risk, borrowers can access better credit terms and manage their debt obligations more effectively. Default risk contributes to credit cycles, where periods of easy credit availability and low default rates are followed by periods of credit tightening and increased defaults. These cycles can influence overall economic activity and financial market stability. High levels of default risk within the financial system can lead to systemic risk, where the failure of one financial institution or borrower triggers a cascade of defaults, potentially causing a broader financial crisis. Default risk has implications for economic growth, as it affects the cost and availability of credit, which in turn influences business investment and consumer spending. Efficient management of default risk is crucial for maintaining a stable and growing economy. Default risk, or credit risk, refers to the likelihood that a borrower will fail to meet their financial commitments, such as repaying a loan or making interest payments. This risk is a key factor in the lending process, influencing lenders' decisions and the accessibility of credit for borrowers. When lenders provide credit, they assume the risk of potential default by the borrower. Managing default risk is essential for the stability and growth of financial markets and the broader economy. Both lenders and borrowers must actively assess and manage default risk to ensure responsible lending practices and maintain financial stability. As the financial landscape continues to evolve, new challenges and developments will emerge in managing default risk, such as the impact of technological advancements and changing economic conditions. Lenders and borrowers must stay informed and adapt their risk management strategies accordingly. Seeking professional wealth management services can help both lenders and borrowers better understand and manage default risk. By working with experienced financial advisors, individuals and institutions can develop tailored strategies to optimize their financial health and minimize default risk.What Is Default Risk?

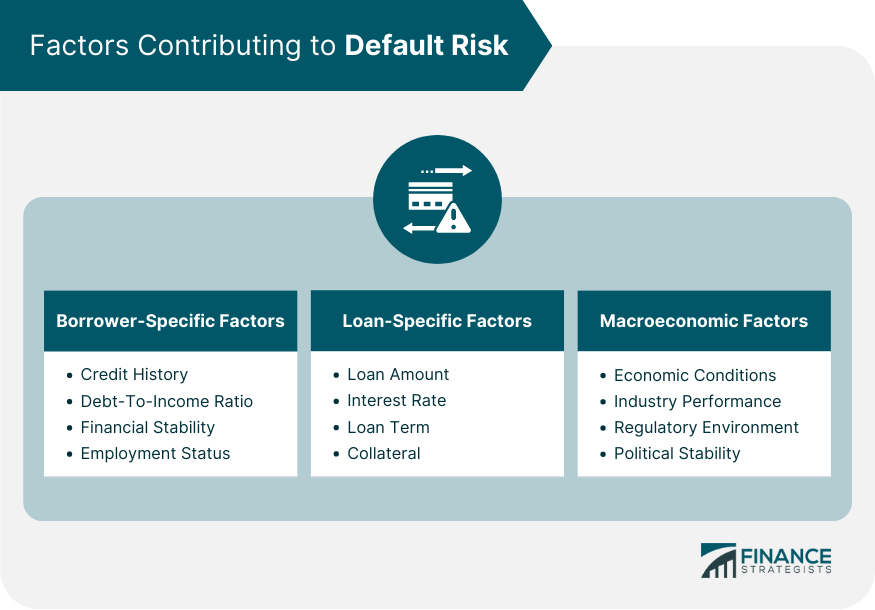

Factors Contributing to Default Risk

Borrower-Specific Factors

Loan-Specific Factors

Macroeconomic Factors

Assessing Default Risk

Credit Rating Agencies

Role and Function

Rating Methodologies

Limitations and Criticism

Internal Credit Scoring Models

Types of Models

Data Sources

Predictive Analytics

Qualitative Assessment

Management Quality

Industry Outlook

Competitive Position

Managing Default Risk

Diversification

Credit Enhancements

Collateral

Guarantees

Credit Default Swaps

Loan Covenants

Loan Renegotiation

Debt Collection Strategies

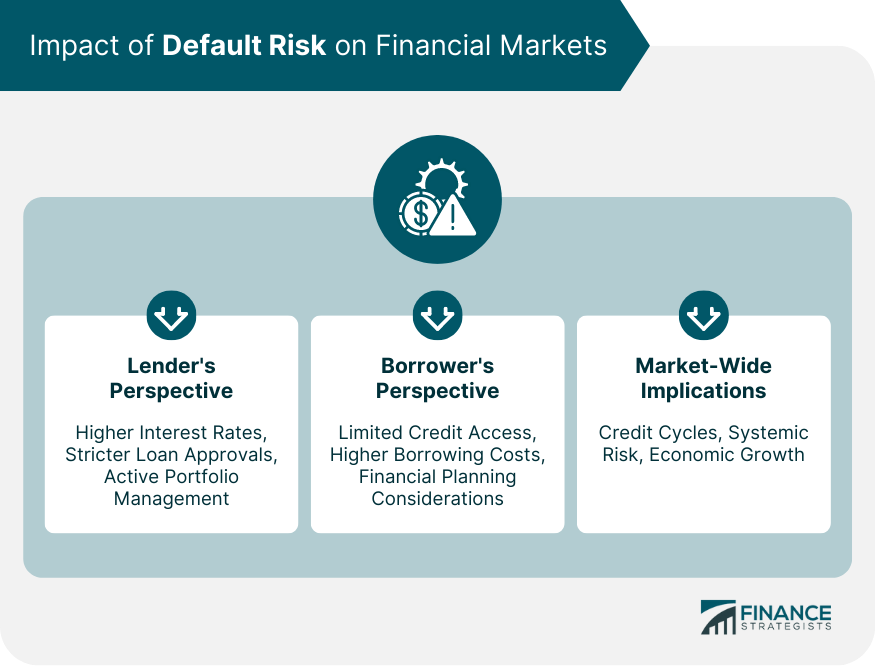

Impact of Default Risk on Financial Markets

Lender's Perspective

Interest Rates

Loan Approvals

Portfolio Management

Borrower's Perspective

Access to Credit

Borrowing Costs

Financial Planning

Market-Wide Implications

Credit Cycles

Systemic Risk

Economic Growth

Final Thoughts

Default Risk FAQs

Default risk refers to the likelihood that a borrower will fail to repay a loan or meet their financial obligations. It is crucial in finance because it affects the cost of borrowing, access to credit, and overall financial market stability for both lenders and borrowers.

Default risk is influenced by borrower-specific factors (e.g., credit history, debt-to-income ratio, financial stability, employment status), loan-specific factors (e.g., loan amount, interest rate, loan term, collateral), and macroeconomic factors (e.g., economic conditions, industry performance, regulatory environment, political stability).

Lenders and credit rating agencies assess default risk using a combination of quantitative and qualitative methods, such as credit scoring models, rating methodologies, and qualitative assessments of management quality, industry outlook, and competitive position.

Strategies for managing default risk include diversification, credit enhancements (e.g., collateral, guarantees, credit default swaps), loan covenants, loan renegotiation, and debt collection strategies.

Default risk impacts financial markets by influencing interest rates, loan approvals, and portfolio management for lenders, as well as access to credit, borrowing costs, and financial planning for borrowers. In turn, this affects credit cycles, systemic risk, and overall economic growth.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.