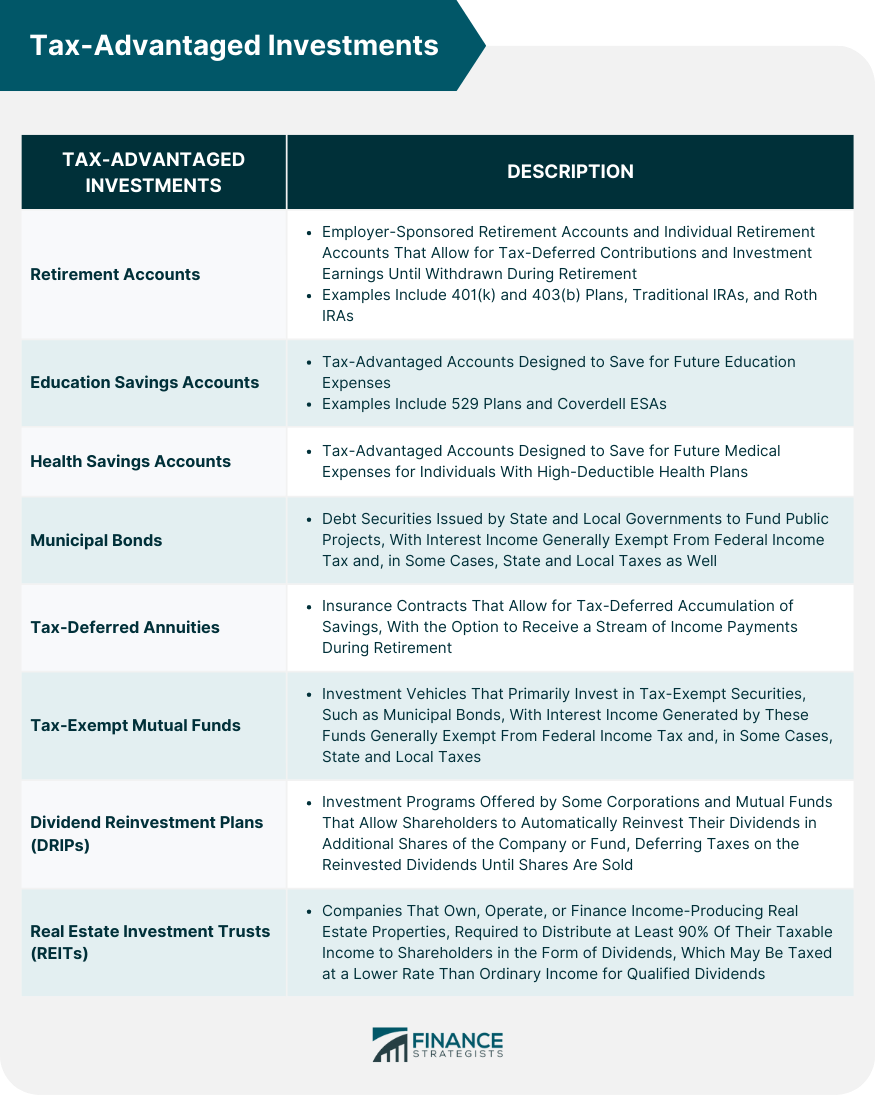

Tax-advantaged investments refer to financial products and strategies designed to minimize tax liability and maximize after-tax returns for investors. These investments offer tax deductions, deferrals, or exemptions on income, capital gains, or dividends, providing investors with more opportunities to grow their wealth over time. The primary goals of tax-advantaged investing are to optimize after-tax returns, preserve capital, and achieve financial goals such as retirement, education funding, or wealth transfer. The benefits of tax-advantaged investments include: Reduced tax liability: By minimizing the taxes on investment income, capital gains, and dividends, investors can keep more of their earnings, leading to higher after-tax returns. Enhanced compounding effect: Tax deferral allows investors to benefit from the compounding effect of their earnings, as they can reinvest the untaxed portion of their gains, which can lead to more significant long-term growth. Improved financial planning: Tax-advantaged investments can help investors plan for their future financial needs, such as retirement or education expenses, by providing tax-efficient savings vehicles. When selecting tax-advantaged investments, investors should consider factors such as their risk tolerance, investment horizon, financial goals, and current and future tax situation. It is essential to evaluate each investment's tax implications and weigh them against the potential returns, risks, and other investment characteristics. 401(k) and 403(b) plans are employer-sponsored retirement accounts that allow employees to contribute pre-tax dollars to their retirement savings. The contributions and investment earnings within these accounts grow tax-deferred until the funds are withdrawn during retirement. At that time, the distributions are taxed as ordinary income. Traditional IRAs are tax-deferred retirement accounts that allow individuals to contribute pre-tax dollars to their retirement savings. The contributions may be tax-deductible, depending on the individual's income and participation in an employer-sponsored retirement plan. Investment earnings within the account grow tax-deferred until withdrawn during retirement, when they are taxed as ordinary income. Roth IRAs are another type of retirement account that allows individuals to contribute after-tax dollars to their retirement savings. The contributions are not tax-deductible, but the investment earnings and qualified withdrawals are tax-free, providing tax-free income in retirement. 529 plans are state-sponsored education savings plans that allow individuals to save for future college expenses. Contributions to a 529 plan are made with after-tax dollars, but the investment earnings grow tax-deferred, and qualified withdrawals for education expenses are tax-free. Coverdell ESAs are tax-advantaged accounts designed to help families save for future education expenses, including K-12 and college costs. Contributions to a Coverdell ESA are made with after-tax dollars, but the investment earnings grow tax-deferred, and qualified withdrawals for education expenses are tax-free. HSAs are tax-advantaged accounts designed to help individuals with high-deductible health plans (HDHPs) save for future medical expenses. Contributions to an HSA are made with pre-tax dollars, and the investment earnings grow tax-deferred. Qualified withdrawals for medical expenses are tax-free Municipal bonds are debt securities issued by state and local governments to fund public projects, such as infrastructure improvements or public services. Interest income earned from municipal bonds is generally exempt from federal income tax and, in some cases, state and local taxes as well. This tax exemption makes municipal bonds attractive to investors in high tax brackets seeking tax-free income. Tax-deferred annuities are insurance contracts that allow investors to accumulate savings on a tax-deferred basis, with the option to receive a stream of income payments during retirement. Contributions to a tax-deferred annuity are made with after-tax dollars, but the investment earnings grow tax-deferred until withdrawn. At the time of withdrawal, the earnings are taxed as ordinary income. Tax-exempt mutual funds are investment vehicles that primarily invest in tax-exempt securities, such as municipal bonds. The interest income generated by these funds is generally exempt from federal income tax, and in some cases, state and local taxes. Tax-exempt mutual funds can be an attractive option for investors seeking tax-free income and diversification within their portfolios. Dividend reinvestment plans (DRIPs) are investment programs offered by some corporations and mutual funds that allow shareholders to automatically reinvest their dividends in additional shares of the company or fund. By reinvesting dividends rather than receiving them as cash, investors can benefit from the compounding effect of their investment and defer taxes on the reinvested dividends until the shares are sold. Real Estate Investment Trusts (REITs) are companies that own, operate, or finance income-producing real estate properties. REITs are required to distribute at least 90% of their taxable income to shareholders in the form of dividends, which may be taxed at a lower rate than ordinary income for qualified dividends. Investing in REITs can provide investors with a tax-efficient source of income and exposure to the real estate market. Some tax-advantaged investments, such as contributions to traditional IRAs and HSAs, may be tax-deductible, reducing an investor's taxable income. Tax credits may also be available for certain investments, such as contributions to retirement accounts for low-income taxpayers or investments in renewable energy. Tax-deferral is a key benefit of many tax-advantaged investments, allowing investors to postpone taxes on their investment earnings until a future date, typically during retirement. This can lead to enhanced compounding effects and potentially higher after-tax returns. Certain tax-advantaged investments, such as Roth IRAs, 529 plans, and municipal bonds, offer tax-free earnings, providing investors with tax-free income and potentially higher after-tax returns. Tax-efficient asset allocation is a strategy that involves placing investments with different tax characteristics in the most suitable accounts to minimize overall tax liability. For example, investors might hold tax-exempt municipal bonds in a taxable account, while keeping tax-deferred investments, such as traditional IRAs, in tax-advantaged accounts. Diversification and asset allocation are essential strategies for optimizing tax-advantaged investments. By spreading investments across various asset classes and tax-advantaged vehicles, investors can achieve a balanced portfolio that aligns with their risk tolerance, financial goals, and tax situation. The timing of contributions and withdrawals can have a significant impact on the tax efficiency of an investment strategy. For example, making contributions to retirement accounts early in the year can maximize the compounding effect of tax-deferred growth. Additionally, strategically timing withdrawals from tax-advantaged accounts can help minimize taxes and penalties, especially during retirement when investors may be in a lower tax bracket. Tax-loss harvesting is a strategy that involves selling investments at a loss to offset capital gains realized on other investments. This can help reduce an investor's overall tax liability and improve the tax efficiency of their portfolio. Tax-loss harvesting should be done carefully, considering factors such as the investor's risk tolerance, investment goals, and the potential impact on their overall portfolio. Income shifting is a tax planning strategy that involves transferring income-producing assets or investments to family members in lower tax brackets. This can help reduce the overall tax liability for the family unit and maximize the after-tax returns on the investments. However, income shifting must be done within the bounds of tax laws and regulations to avoid potential tax penalties. Charitable giving can play a significant role in tax-advantaged investing, as donations to qualified charities can be tax-deductible and reduce an investor's taxable income. Donating appreciated assets, such as stocks or real estate, can provide additional tax benefits by avoiding capital gains taxes on the appreciated value. Charitable remainder trusts and donor-advised funds are other tax-efficient strategies for incorporating charitable giving into an investment plan. Tax-advantaged accounts, such as IRAs, 401(k)s, and 529 plans, often have annual contribution limits. Exceeding these limits can result in tax penalties and may undermine the tax efficiency of the investment strategy. Some tax-advantaged investments, such as Roth IRAs and certain tax deductions or credits, have income restrictions that limit their availability to high-income earners. Investors should be aware of these restrictions and plan their investment strategy accordingly. Many tax-advantaged accounts have rules and restrictions on withdrawals, such as early withdrawal penalties or required minimum distributions. Investors should understand these rules and plan their withdrawal strategy to minimize taxes and penalties. Tax laws and regulations are subject to change, which can impact the tax benefits and implications of various investment strategies. Investors should stay informed about legislative changes and consult with a tax professional or financial advisor to ensure their investment strategy remains tax-efficient. Tax professionals, such as Certified Public Accountants (CPAs) or Enrolled Agents (EAs), can help investors navigate the complex tax landscape and develop tax-efficient investment strategies. They can provide guidance on tax laws and regulations, assist with tax planning and compliance, and help maximize tax benefits and deductions. Financial planners can help investors develop a comprehensive financial plan that incorporates tax-advantaged investments and aligns with their financial goals, risk tolerance, and investment horizon. They can provide guidance on asset allocation, diversification, and other investment strategies to optimize after-tax returns. Investment advisors can help investors select and manage tax-advantaged investments, such as mutual funds, ETFs, or individual securities. They can provide insights on market trends, investment analysis, and portfolio management to help investors achieve their financial objectives while minimizing tax liability. Tax-advantaged investments play a crucial role in helping investors minimize tax liability and maximize after-tax returns. By understanding the various types of tax-advantaged investments and strategically incorporating them into their portfolios, investors can achieve their financial goals more effectively. However, it is important to be aware of the risks and limitations associated with these investments and to consult with professional advisors to ensure a tax-efficient investment strategy.Definition of Tax-Advantaged Investments

Goals and Benefits of Tax-Advantaged Investing

Factors to Consider When Choosing Tax-Advantaged Investments

Types of Tax-Advantaged Investments

Retirement Accounts

401(k) and 403(b) Plans

Individual Retirement Accounts (IRAs)

Roth IRAs

Education Savings Accounts

529 Plans

Coverdell Education Savings Accounts (ESAs)

Health Savings Accounts (HSAs)

Municipal Bonds

Tax-Deferred Annuities

Tax-Exempt Mutual Funds

Dividend Reinvestment Plans (DRIPs)

Real Estate Investment Trusts (REITs)

Tax Benefits and Implications of Tax-Advantaged Investments

Tax Deductions and Credits

Tax Deferral

Tax-Free Earnings

Tax-Efficient Asset Allocation

Strategies for Optimizing Tax-Advantaged Investments

Diversification and Asset Allocation

Timing of Contributions and Withdrawals

Tax-Loss Harvesting

Income Shifting

Charitable Giving Strategies

Risks and Limitations of Tax-Advantaged Investments

Contribution Limits

Income Restrictions

Withdrawal Penalties and Restrictions

Legislative Changes

Role of Professional Advisors in Tax-Advantaged Investing

Tax Professionals

Financial Planners

Investment Advisors

Conclusion

Tax-Advantaged Investments FAQs

Tax-advantaged investments are investments that offer tax benefits or incentives, such as tax-deferred growth, tax-free withdrawals, or tax deductions, that can help investors minimize their tax liabilities.

Examples of tax-advantaged investments include 401(k) plans, individual retirement accounts (IRAs), Roth IRAs, Health Savings Accounts (HSAs), 529 college savings plans, and municipal bonds.

Investing in tax-advantaged investments can help you save on taxes in several ways, such as reducing your taxable income, deferring taxes on investment gains, and avoiding taxes on qualified withdrawals.

Tax-advantaged investments can benefit anyone who wants to minimize their tax liabilities and maximize their investment returns. They are especially beneficial for high-income earners who are in higher tax brackets.

One potential drawback of tax-advantaged investments is that there may be restrictions or penalties for early withdrawals or non-qualified distributions. Additionally, some tax-advantaged investments may have higher fees or lower returns compared to other investment options. It is important to carefully evaluate the potential benefits and drawbacks before investing in tax-advantaged investments.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.