Charitable tax credits are the government's financial incentives to encourage taxpayers to support nonprofit organizations, foundations, and religious institutions through charitable giving. These credits reduce taxpayers' tax liability by allowing them to deduct a portion or the full amount of their charitable contributions, depending on the applicable rules and limits. By offering these tax benefits, the government promotes philanthropy and fosters support for organizations that contribute to the public good. Nonprofit organizations are entities that operate for the public good rather than for the benefit of owners or shareholders. Examples of nonprofits include educational institutions, hospitals, and environmental groups. Foundations are organizations established to provide financial support for charitable purposes. They often provide grants and funding to other nonprofits, including private foundations, such as family or corporate foundations, and public charities, such as community foundations. Religious organizations include churches, synagogues, mosques, and other institutions that primarily engage in religious activities. These organizations often provide essential community services and support humanitarian efforts. Taxpayers can deduct charitable contributions if they itemize their deductions on Schedule A of Form 1040 rather than claiming the standard deduction. Itemizing allows taxpayers to reduce their taxable income by the amount of their donations up to certain limits. The Internal Revenue Service (IRS) limits the amount of charitable deductions that can be claimed in a given tax year. Generally, taxpayers can deduct up to 60% of their adjusted gross income (AGI) for cash contributions made to public charities. Excess contributions can be carried over and deducted in subsequent tax years, subject to limitations. If a taxpayer's charitable contributions exceed the annual deduction limits, the excess amount can be carried over and deducted in the following tax year. The carryover period is limited to five years. To claim a charitable tax deduction, taxpayers must contribute to a qualified charitable organization, as defined by the IRS. To verify an organization's status, taxpayers can use the IRS's Tax Exempt Organization Search tool. To claim a charitable tax deduction, taxpayers must meet certain requirements, including maintaining proper documentation and records of their donations. Cash donations include cash, check, credit card, or electronic fund transfer contributions. These are the most straightforward donations to document and claim as deductions. Non-cash donations include contributions of tangible personal property, real estate, and stock or securities. The tax treatment of non-cash donations can be more complex, as it often depends on the type and value of the donated property. While the value of volunteer services is not deductible, taxpayers can deduct certain out-of-pocket expenses incurred while performing volunteer work, such as travel expenses and the cost of supplies. The fair market value (FMV) of a donated item is the price at which it would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts. The IRS provides guidelines for determining the FMV of various types of property. When donating appreciated property, taxpayers may be able to deduct the full FMV of the property without paying capital gains tax on the appreciation. Conversely, when donating depreciated property, taxpayers can only deduct the property's adjusted basis (the original cost minus depreciation). Special rules also apply to the donation of vehicles and boats, which may require additional documentation and valuation methods. Bunching donations involve making multiple years' worth of charitable contributions in a single tax year, allowing taxpayers to itemize deductions and claim a larger tax benefit. Donor-advised funds allow taxpayers to contribute to a specific fund, receive an immediate tax deduction, and then recommend grants to qualified charities over time. CRTs are irrevocable trusts that provide a stream of income to the donor or other beneficiaries for a specified period, with the remaining assets going to a designated charity upon the trust's termination. CLTs are irrevocable trusts that provide a stream of income to a designated charity for a specified period, with the remaining assets reverting to the donor or other beneficiaries upon the trust's termination. Taxpayers aged 70½ or older can make tax-free transfers from their Individual Retirement Account (IRA) directly to a qualified charity, which can satisfy their required minimum distribution (RMD) without increasing their taxable income. Taxpayers report their total charitable contributions on Line 12 of Form 1040 and their other itemized deductions. Taxpayers who itemize deductions must complete Schedule A, which provides a detailed breakdown of their charitable contributions and other deductible expenses. For non-cash contributions exceeding $500 in value, taxpayers must complete Form 8283, which provides additional information about the donated property and its valuation. Failing to maintain proper documentation, such as receipts, canceled checks, or written acknowledgment from the charitable organization, can result in the IRS disallowing a taxpayer's claimed deductions. Taxpayers should verify an organization's qualified status before making a donation, as contributions to non-qualified organizations are not deductible. Overvaluing non-cash contributions can result in penalties and interest if the IRS determines that the taxpayer has significantly overstated the value of the donated property. Given the complexity of charitable tax credits, taxpayers should consider consulting with a tax services professional to ensure they maximize their deductions and comply with all applicable laws and regulations. Charitable tax credits are a vital incentive for taxpayers to support nonprofit organizations, foundations, and religious institutions. There are various aspects of charitable tax credits, including the types of eligible organizations, tax benefits, eligibility requirements, types of contributions, valuation methods, tax planning strategies, reporting requirements, and common mistakes to avoid. By understanding and adhering to these guidelines, taxpayers can maximize the financial benefits of their charitable giving while supporting the causes they care about. Proper planning, accurate record-keeping, and consultation with tax professionals can help taxpayers navigate the complexities of charitable tax credits and ensure compliance with all applicable laws and regulations.What Are Charitable Tax Credits?

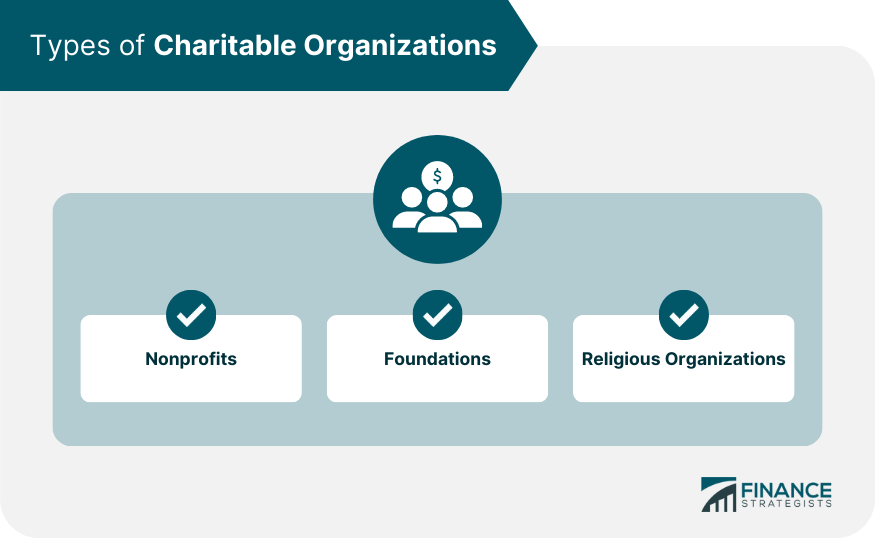

Types of Charitable Organizations

Nonprofits

Foundations

Religious Organizations

Tax Benefits of Charitable Contributions

Deductibility of Donations

Limits on Charitable Deductions

Carryover Provisions

Eligibility for Charitable Tax Credits

Qualified Charitable Organizations

Donor Requirements

Types of Charitable Contributions

Cash Donations

Non-cash Donations

Volunteer Services

Valuation of Charitable Contributions

Fair Market Value (FMV) Determination

Special Rules for Specific Types of Contributions

Tax Planning Strategies for Charitable Giving

Bunching Donations

Donor-Advised Funds (DAFs)

Charitable Remainder Trusts (CRTs)

Charitable Lead Trusts (CLTs)

IRA Charitable Rollover

Reporting Charitable Contributions on Tax Returns

IRS Form 1040

Schedule A: Itemized Deductions

Form 8283: Non-cash Contributions

Common Mistakes and Pitfalls of Charitable Tax Credits

Inadequate Documentation

Donating to Non-qualified Organizations

Overvaluing Contributions

Failing to Consult Tax Professionals

Conclusion

Charitable Tax Credits FAQs

Charitable tax credits provide financial incentives for taxpayers by reducing their tax liability when they contribute to eligible organizations. For society, these credits encourage philanthropy and support nonprofit organizations, foundations, and religious institutions that contribute to the public good.

To qualify for charitable tax credits, your donation must be made to an organization recognized by the IRS as a qualified charitable organization. You can verify an organization's status using the IRS's Tax Exempt Organization Search tool.

Yes, there are limits on the number of charitable tax credits you can claim based on your adjusted gross income (AGI). Generally, you can deduct up to 60% of your AGI for cash contributions made to public charities. Excess contributions can be carried over and deducted in subsequent tax years, subject to limitations.

Yes, you can claim charitable tax credits for non-cash donations, such as property or stock, provided that you follow the appropriate valuation and documentation guidelines. The tax treatment of non-cash donations can be more complex, as it depends on the type and value of the donated property.

When claiming charitable tax credits, you must maintain proper documentation and records of your donations, such as receipts, canceled checks, or written acknowledgment from the charitable organization. For non-cash contributions exceeding $500 in value, you must also complete Form 8283, which provides additional information about the donated property and its valuation.