Retirement income refers to the financial resources that individuals receive during their retirement years. It serves as a replacement for the regular income they earned while actively working. Retirement income is essential for maintaining a comfortable and fulfilling lifestyle after leaving the workforce. It is important for individuals to plan and save for retirement to ensure a sufficient and reliable income stream. Factors such as projected living expenses, desired lifestyle, and retirement goals should be considered when determining how much retirement income is needed. Determining your retirement income involves several factors. You'll need to consider your current savings and investments, projected future savings, potential Social Security benefits, pensions, and other income sources like annuities or part-time work. Tools like retirement calculators can help you estimate your income based on these factors. Remember, optimizing investment strategies, using tax-advantaged retirement accounts, and planning for potential risks can significantly influence your retirement income. It's recommended to seek professional advice to create a robust retirement plan. While the exact calculation can vary depending on individual circumstances and the sources of retirement income, there are some common steps you can follow to get a rough estimate. Start by envisioning the type of lifestyle you want to have during retirement. Consider factors such as housing, healthcare, travel, hobbies, and any other expenses you anticipate. Having a clear understanding of your retirement goals will help you determine the amount of income you need to support that lifestyle. Visit the Social Security Administration's website or use their online tools to obtain an estimate of your projected Social Security benefits. This will provide you with an idea of the monthly income you can expect from Social Security. Keep in mind that the age at which you begin receiving benefits can impact the amount you receive. If you are entitled to a pension, gather information about the terms of your pension plan. Review the documentation or consult with your employer's benefits department to understand the projected monthly income you will receive from your pension during retirement. Evaluate your personal savings and investment accounts, such as savings accounts, IRAs, 401(k)s, or other retirement savings vehicles. Take stock of the current balance of each account and estimate the rate of return on your investments. Consider consulting with a financial advisor to help assess your investment portfolio and project its potential growth over time. Consider any additional sources of income you may have during retirement. This could include rental income from investment properties, dividends from stocks or bonds, or income from part-time work. Take these potential sources into account when calculating your estimated retirement income. Add up the estimated income from Social Security, pension benefits, personal savings and investments, and any other potential income sources. This will give you a total estimated retirement income. Keep in mind that inflation can erode the purchasing power of your retirement income over time. Factor in a reasonable estimate for inflation when projecting your future income needs. Additionally, consider your life expectancy and plan for a retirement duration that aligns with your circumstances. A well-planned investment strategy can significantly boost your retirement income. Consider an Asset Allocation and Diversification strategy to balance risk and return in your portfolio. Another strategy involves Dividend Investing, where you invest in companies that regularly pay dividends, providing a steady income stream. Lastly, Real Estate Investing can also provide retirement income, whether through rental income or by selling property for a profit. Social Security benefits can be maximized through smart decision-making. The Timing of Benefit Claims can significantly impact the total benefits received. Delaying benefits until full retirement age or later can significantly increase your monthly income. Understanding Spousal Benefits can also be beneficial for couples. In some cases, claiming spousal benefits can provide a higher income than claiming on your own work record. Tax-advantaged retirement accounts can greatly increase your retirement income by reducing your tax burden. Traditional and Roth IRAs offer tax advantages that can result in more income in retirement. 401(k) Plans provide tax-deferred growth, and your contributions can often be matched by your employer, boosting your savings. Health Savings Accounts (HSAs) can also provide tax advantages if used for qualified medical expenses, which can be a significant portion of spending in retirement. Annuities can provide a guaranteed income stream in retirement. There are different types of annuities, including fixed, variable, and indexed, each with its own pros and cons. Understanding these can help you decide if an annuity is a good fit for your retirement plan. Retirement income management is as crucial as its accumulation. The 4% Rule is a common guideline for withdrawal. It suggests that if you withdraw 4% of your retirement savings in the first year and adjust for inflation in the following years, your savings should last 30 years. Required Minimum Distributions (RMDs) are mandatory withdrawals from retirement accounts starting at a certain age. Understanding RMDs is essential to avoid hefty penalties and manage your retirement income effectively. Dynamic Withdrawal Strategies involve adjusting your withdrawal rate based on market performance and your portfolio's value, which could help extend the longevity of your savings. Taxes can significantly impact your retirement income. Taxation of Social Security Benefits varies based on your income level. Understanding how your benefits may be taxed can help you plan for retirement more effectively. Certain retirement accounts are subject to Required Minimum Distributions and Taxation. Failing to take these distributions can result in a substantial tax penalty. Different states also have different tax rules for retirees. Understanding the State Tax Implications where you plan to retire can help you keep more of your income. Inflation can erode your retirement savings. Understanding the Impact of Inflation on Retirement Savings can help you plan for a more secure retirement. Some Strategies to Offset Inflation include investing in inflation-protected securities and planning for a higher withdrawal rate. Retirement income planning provides a roadmap for achieving financial security during retirement. By evaluating your current assets, estimating future income streams, and accounting for potential expenses, you can gain peace of mind knowing that you have a solid plan in place to meet your financial needs. Proper planning ensures that you can maintain your desired lifestyle even after you retire. It allows you to set realistic expectations based on your income sources and expenses, helping you avoid financial strain and potential downsizing or compromises in your retirement years. Retirement income planning helps you determine the most effective allocation of your assets. By considering factors such as risk tolerance, time horizon, and income needs, you can make informed decisions about investment strategies, ensuring your portfolio aligns with your retirement goals. Through retirement income planning, you can identify and optimize various income sources. This may include maximizing Social Security benefits by understanding the best claiming strategies, leveraging pension plans, utilizing tax-advantaged retirement accounts, exploring annuities, or even considering part-time work to supplement your income. Longevity risk is the risk of outliving your savings. With people living longer, this has become a significant concern for retirees. Planning for a longer retirement can help mitigate this risk. Market volatility can significantly impact your retirement savings. A poorly timed downturn could significantly decrease your savings and the income they can generate. Healthcare costs are a major concern for many retirees and can significantly impact retirement income. It's crucial to plan for these costs, including considering long-term care insurance. The sequence of returns risk refers to the danger of receiving poor returns early in retirement. This could force you to withdraw a larger portion of your savings, potentially depleting your savings faster. Planning for a secure retirement entails several critical factors. Foremost, an estimate of your retirement income must be accurately computed, considering all income sources - Social Security, personal savings, pensions, and more. Emphasis should be placed on sound investment strategies, effectively utilizing benefits, and employing tax-advantaged retirement accounts for maximal gain. Particular attention should be paid to annuities as they offer a guaranteed income stream. Remember, managing retirement income is just as crucial as accruing it. Implement dynamic withdrawal strategies, comprehend tax implications, and devise plans to mitigate inflation's impact. Familiarize yourself with potential risks, including longevity risk, market volatility, escalating healthcare costs, and sequence of returns risk. The journey toward retirement may seem daunting, but armed with this knowledge and continuous professional advice, you'll be well-equipped to navigate it.What Is Retirement Income?

How Much Income Will I Have in Retirement?

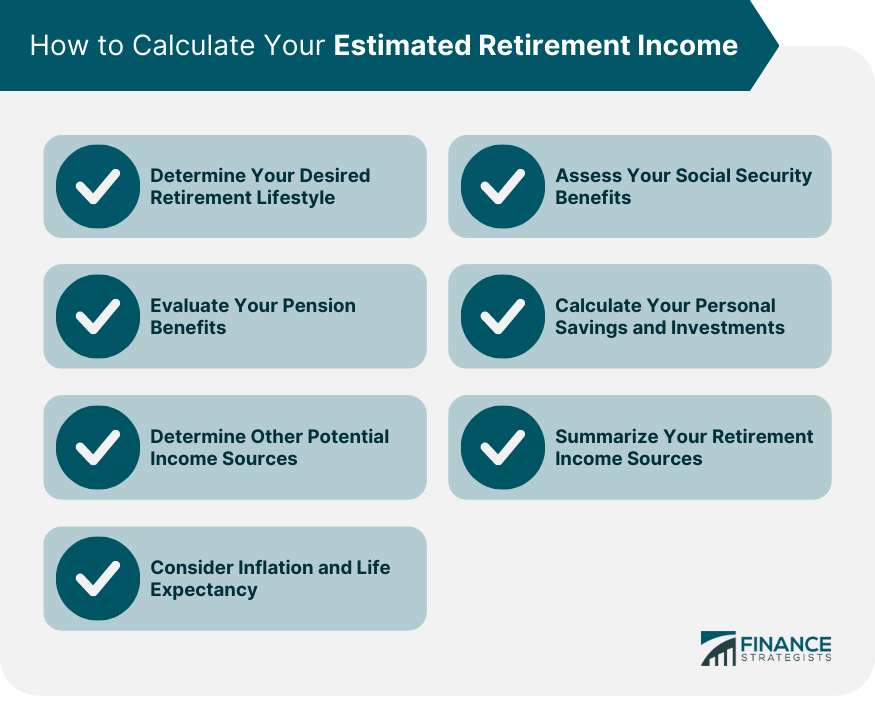

How to Calculate Your Estimated Retirement Income

Determine Your Desired Retirement Lifestyle

Assess Your Social Security Benefits

Evaluate Your Pension Benefits

Calculate Your Personal Savings and Investments

Determine Other Potential Income Sources

Summarize Your Retirement Income Sources

Consider Inflation and Life Expectancy

Maximizing Retirement Income

Investment Strategies for Retirement Income

Making the Most of Social Security Benefits

Utilizing Tax-Advantaged Retirement Accounts

Annuities as a Guaranteed Income Stream

Managing Retirement Income

Retirement Withdrawal Strategies

Tax Considerations in Retirement

Dealing With Inflation

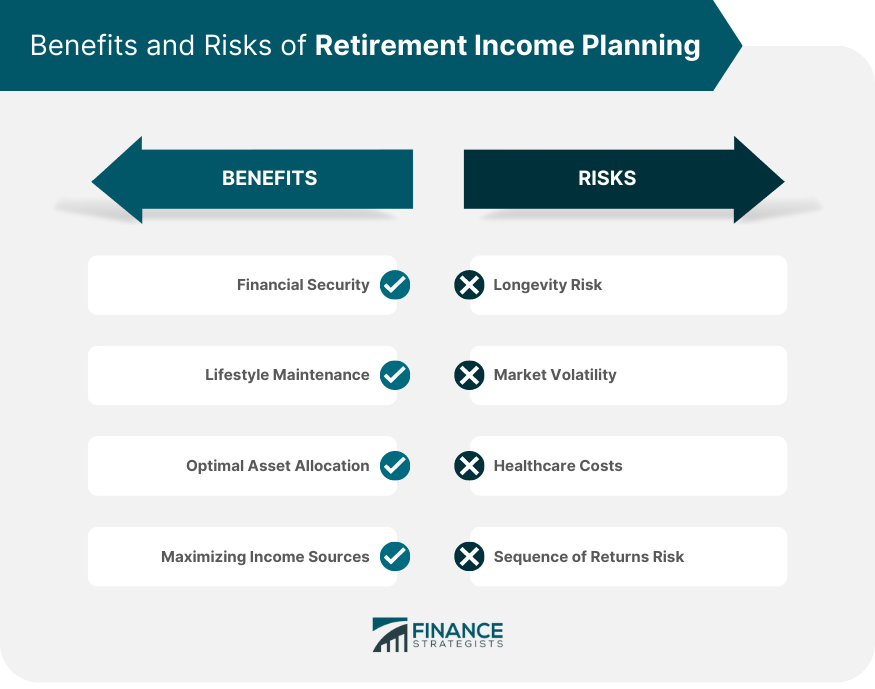

Benefits of Retirement Income Planning

Financial Security

Lifestyle Maintenance

Optimal Asset Allocation

Maximizing Income Sources

Risks and Challenges in Retirement Income Planning

Longevity Risk

Market Volatility

Healthcare Costs

Sequence of Returns Risk

Conclusion

How Much Income Will I Have in Retirement? FAQs

Determining your retirement income depends on various factors such as your current savings, investments, Social Security benefits, pensions, and other income sources. It's recommended to use retirement calculators and seek professional advice to estimate your income accurately.

To maximize retirement income, consider asset allocation and diversification strategies, dividend investing for a steady income stream, and real estate investing for rental income or property sales. These strategies can help optimize your portfolio and generate additional income.

You can maximize Social Security benefits by making smart decisions. Timing benefit claims is crucial, as delaying until full retirement age or later can increase monthly income. Understanding spousal benefits can also be beneficial for couples, potentially providing a higher income than claiming on your own work record.

Tax-advantaged retirement accounts, such as Traditional and Roth IRAs and 401(k) Plans, offer tax advantages that can result in more income during retirement. These accounts provide tax-deferred growth and potential employer contributions, reducing your tax burden and boosting savings.

Annuities can offer a guaranteed income stream in retirement. There are different types, including fixed, variable, and indexed annuities, each with its own benefits. Understanding these options can help you determine if an annuity aligns with your retirement plan and income needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.