An ETF Portfolio for Retirement Income refers to a diversified collection of exchange-traded funds (ETFs) curated to generate steady income during retirement. ETFs, essentially investment funds traded on stock exchanges, allow investors to buy a range of assets like stocks or bonds in one purchase. This retirement income strategy leverages the flexibility, low cost, and diversification of ETFs to balance growth and income. The portfolio typically includes bond ETFs for stable income, dividend ETFs for consistent yield, and some equity ETFs for capital appreciation. The purpose is to provide retirees a reliable income stream and cushion against inflation while mitigating market risk. The ETF Portfolio for Retirement Income is an effective approach to maintain purchasing power and achieve financial security in the golden years. Equity ETFs that focus on dividend-yielding stocks can be an excellent source of income for retirees. These ETFs invest in companies known for regularly paying dividends, providing a steady income stream. Moreover, companies that consistently pay dividends are typically well-established and financially sound, which can add an element of safety to your retirement portfolio. Bond ETFs invest in a portfolio of bonds and can provide regular income through interest payments. Different types of bond ETFs invest in different types of bonds, including government bonds, corporate bonds, and municipal bonds. Depending on their investment objectives, some bond ETFs may aim to provide higher income, while others might focus on preserving capital. Real Estate ETFs, which invest in Real Estate Investment Trusts (REITs) or direct real estate properties, offer potential for both income and growth. REITs are required to distribute at least 90% of their taxable income to shareholders annually in the form of dividends, offering a steady income stream. Moreover, as the value of real estate properties appreciates over time, investors may also benefit from capital gains. Commodity ETFs invest in physical commodities like gold, oil, or agricultural products. They can serve as a hedge against inflation, protecting the purchasing power of your retirement income. During periods of high inflation, the price of commodities typically increases, which can offset the impact of inflation on your portfolio. Multi-Asset ETFs invest in a combination of different asset classes, including stocks, bonds, and commodities. This diversification can provide balanced returns, as different asset classes may perform well at different times. Multi-Asset ETFs can be a good choice for retirees seeking a balanced investment approach. Investing in an ETF essentially means investing in a wide array of securities, providing protection against the underperformance of any single security. This diversification reduces risk, making ETFs a valuable component of a retirement portfolio. ETFs typically have lower expense ratios compared to mutual funds. These lower costs can significantly enhance your retirement income over time. ETFs are tax efficient, generally resulting in fewer capital gains distributions. This efficiency can result in a lower tax bill for retirees, allowing them to retain more of their income. The flexibility of ETFs—being tradable throughout the day—can lead to over-trading. This frequent buying and selling can increase costs, potentially diminishing investment returns. While ETFs provide broad market exposure, they do not guarantee returns. An ETF's performance is linked to the performance of the underlying asset or index it tracks. If this asset or index performs poorly, the ETF will as well. Some ETFs, such as leveraged or inverse ETFs, are quite complex. These may not be suitable for all investors, particularly those nearing retirement, as they may entail higher risks. The first step in designing an ETF portfolio for retirement is to clearly define your retirement goals and risk tolerance. Your retirement goals might include the income you need to sustain your desired lifestyle, your plans for travel, and potential healthcare expenses. Once you have a clear understanding of your retirement needs, you can select ETFs that align with these objectives and your risk tolerance. When selecting ETFs, aim for a mix of different types that offer broad diversification. This strategy can help manage risk and potentially increase returns. For instance, you might consider a blend of equity ETFs, bond ETFs, and commodity ETFs to ensure your portfolio isn't overly reliant on a single asset class. The proportion of your portfolio you dedicate to different types of ETFs should be informed by your risk tolerance and your retirement income needs. As a general rule, the closer you are to retirement, the more conservative your portfolio should be. This might mean a larger allocation to bond ETFs, which tend to be less volatile than equity ETFs, and a smaller allocation to riskier assets like commodity ETFs. Asset location refers to the type of account in which you hold different investments for tax purposes. For maximum tax efficiency, consider holding tax-inefficient investments, like REITs, in tax-advantaged accounts, and tax-efficient investments, like equity ETFs, in taxable accounts. Over time, market fluctuations can cause your portfolio's allocation to drift from your original target. Regular rebalancing, which involves buying and selling assets to maintain your desired allocation, is essential to manage risk and ensure your portfolio stays aligned with your retirement goals. While rebalancing is important, it's also essential to consider the tax implications. Selling investments can trigger capital gains tax, so it's important to strategize when and how to rebalance. Market fluctuations can lead to periods of volatility in your portfolio's value. Having a well-diversified ETF portfolio can help smooth out these fluctuations. Additionally, maintaining a long-term perspective and resisting the urge to make rash decisions during market downturns can be beneficial. Determining a sustainable withdrawal rate - the percentage of your portfolio that you can withdraw each year without running out of money - is crucial. While the "4% rule" (withdrawing 4% of your portfolio each year) is commonly used, your specific rate should depend on your individual circumstances, including the composition of your portfolio, your age, and the expected length of your retirement. Sequence of returns risk refers to the danger of experiencing poor investment returns early in retirement, which can significantly impact your portfolio's longevity. One way to mitigate this risk is by maintaining a diversified portfolio and adjusting your withdrawal rate based on market performance. When withdrawing from your ETF portfolio, it's important to consider the tax implications. A tax-efficient withdrawal strategy might involve drawing first from taxable accounts while letting tax-advantaged accounts continue to grow. Investing in an ETF portfolio for retirement income can provide a balanced approach to achieve financial security. ETFs offer diversified, cost-efficient, and tax-effective investment solutions, mitigating risks while fostering income growth. However, investors should be mindful of potential drawbacks such as over-trading, no guaranteed returns, and the complexity of certain ETFs. Ideal types of ETFs for retirement income include Equity, Bond, Real Estate, Commodity, and Multi-Asset ETFs. Crafting an ETF portfolio demands clear goal setting, wise diversification, apt portfolio allocation, and tax-efficient asset location. It's crucial to regularly rebalance the portfolio and manage it strategically amidst market fluctuations. Finally, deciding a sustainable withdrawal rate, understanding the sequence of returns risk, and utilizing tax-efficient withdrawal strategies can significantly enhance the longevity and utility of your retirement portfolio. By astutely harnessing the potential of ETFs, retirees can optimize income streams, navigate market risks, and safeguard their golden years.ETFs: A Key Component for Retirement Income

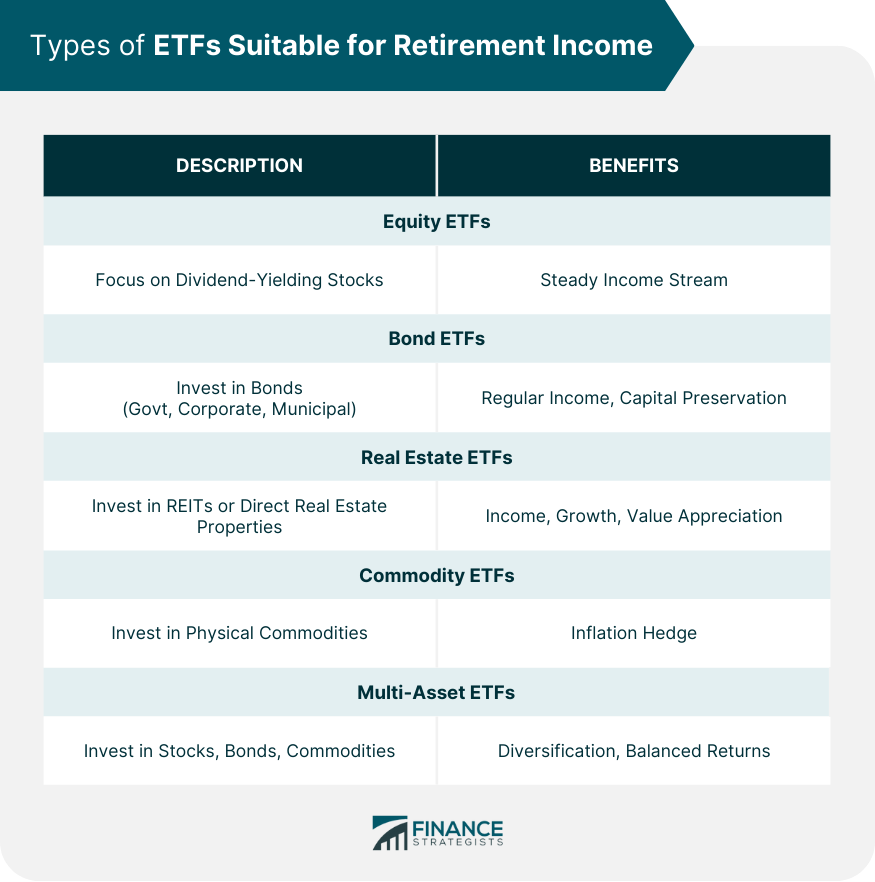

Types of ETFs Suitable for Retirement Income

Equity ETFs

Bond ETFs

Real Estate ETFs

Commodity ETFs

Multi-Asset ETFs

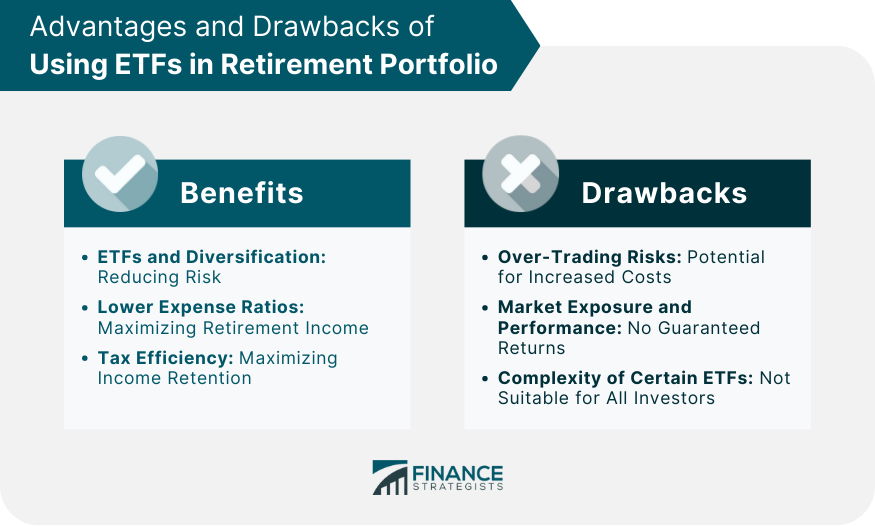

Advantages of Using ETFs in Retirement Portfolio

ETFs and Diversification: Reducing Risk

Lower Expense Ratios: Maximizing Retirement Income

Tax Efficiency: Maximizing Income Retention

Drawbacks of Using ETFs in Retirement Portfolio

Over-Trading Risks: Potential for Increased Costs

Market Exposure and Performance: No Guaranteed Returns

Complexity of Certain ETFs: Not Suitable for All Investors

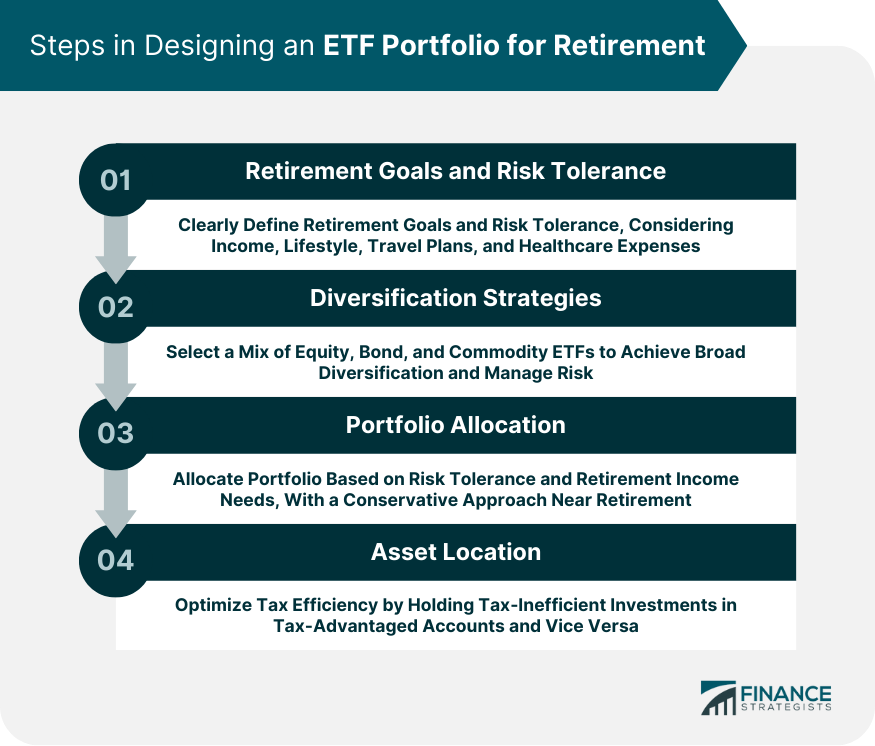

Designing an ETF Portfolio for Retirement

Defining Retirement Goals and Risk Tolerance

Diversification Strategies in ETF Selection

Portfolio Allocation: Balancing Risk and Return

Asset Location: Tax Efficiency Considerations

Rebalancing and Managing the ETF Retirement Portfolio

Importance of Regular Portfolio Rebalancing

Tax Considerations in Rebalancing

Dealing With Market Fluctuations

Withdrawing From Your ETF Retirement Portfolio

Sustainable Withdrawal Rate

Sequence of Returns Risk and Its Impact on Withdrawal Strategy

Tax-Efficient Withdrawal Strategies

Final Thoughts

ETF Portfolio for Retirement Income FAQs

An ETF portfolio for retirement income is an investment strategy that involves using exchange-traded funds (ETFs) to generate a steady income stream during retirement.

An ETF portfolio can support retirement income through dividends from equity ETFs, interest from bond ETFs, and potential capital gains from various types of ETFs.

ETFs offer a range of benefits for retirement income, including diversification, flexibility, tax efficiency, and often lower costs compared to mutual funds.

Several types of ETFs can be suitable for retirement income, including equity ETFs (especially those focused on dividend-yielding stocks), bond ETFs, real estate ETFs, commodity ETFs, and multi-asset ETFs.

Some risks of using ETFs for retirement income include market volatility, regulatory changes, and longevity risk (the risk of outliving your savings). However, these risks can be managed with a well-diversified portfolio and sound investment strategies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.