The 4% rule is a widely-accepted guideline used in retirement planning to determine the annual withdrawal rate from an investment portfolio. This rule suggests that retirees can withdraw 4% of their portfolio's value in the first year of retirement and then adjust the withdrawn amount for inflation in subsequent years. The primary objective of this rule is to ensure a steady stream of income during retirement while minimizing the risk of depleting the retiree's savings over a 30-year period. The 4% rule has become a cornerstone of retirement planning because it provides retirees with a clear and straightforward approach to managing their savings. By following this rule, individuals can gain a better understanding of how much money they need to save for retirement, estimate the amount they can safely withdraw each year, and minimize the risk of outliving their savings. To apply the 4% rule, retirees should calculate 4% of their total investment portfolio's value at the beginning of retirement. This will be the initial amount withdrawn for the first year. In subsequent years, the withdrawal amount should be adjusted for inflation, based on the previous year's withdrawal. The 4% rule takes into account the impact of inflation on a retiree's purchasing power. By adjusting the withdrawal amount each year for inflation, retirees can maintain a consistent standard of living throughout their retirement. Under the 4% rule, a retiree's annual withdrawal amount is determined by the portfolio's value at the beginning of retirement. This means that if the portfolio's value decreases due to poor investment performance, the withdrawal amount will not be automatically adjusted. To maintain the desired withdrawal rate, retirees may need to reevaluate their portfolios and make adjustments. The success of the 4% rule depends on a retiree's asset allocation, which is the mix of investments in their portfolio. Typically, the rule assumes a balanced portfolio of 60% stocks and 40% bonds. This allocation aims to provide a balance between growth and stability, enabling retirees to benefit from stock market gains while also having a buffer against market downturns. One of the primary advantages of the 4% rule is its simplicity. The rule is easy to understand and apply, making it an appealing option for individuals who want a straightforward approach to managing their retirement savings. The 4% rule has been shown to be successful in the majority of historical scenarios, providing a reasonable withdrawal rate that allows retirees to maintain their standard of living without depleting their savings over a 30-year period. The 4% rule serves as a valuable benchmark for individuals planning for retirement, offering a starting point for determining how much money they need to save and how much they can safely withdraw each year during retirement. One of the main criticisms of the 4% rule is that it assumes a fixed retirement period of 30 years. This may not be suitable for all individuals, as some may experience a longer or shorter retirement period. The 4% rule is based on historical data and may not accurately predict future market conditions. While it has worked well in the past, there is no guarantee that it will continue to be effective in the future, particularly in the face of changing economic landscapes or unforeseen financial crises. The 4% rule does not automatically adjust for changes in market conditions, such as periods of low returns or high volatility. This inflexibility can expose retirees to the risk of running out of money sooner than anticipated, especially if their portfolio suffers significant losses early in retirement. The 4% rule may not provide sufficient income for retirees in an environment of low-interest rates and high market valuations, as it was developed during a period of higher historical returns. In such conditions, retirees may need to consider alternative withdrawal strategies or adjust their expectations for retirement income. One alternative to the 4% rule is to use a percentage-based withdrawal strategy, in which retirees withdraw a fixed percentage of their portfolio's value each year, regardless of market performance. This approach provides greater flexibility, as it allows retirees to benefit from market gains while also adjusting their withdrawals during periods of poor returns. Another variable withdrawal strategy involves making adjustments to withdrawal rates based on market performance. For example, retirees could reduce their withdrawal rate during periods of market decline, preserving their portfolio value, and increase their withdrawal rate when the market is performing well. The Guyton-Klinger rules are a set of guidelines that incorporate dynamic adjustments to withdrawal rates based on market performance and portfolio value. These rules allow for increased flexibility in retirement income planning, helping retirees navigate changing market conditions and preserve their savings. Required Minimum Distributions (RMDs) are a withdrawal strategy based on the IRS guidelines for traditional IRAs and 401(k) plans. Under this approach, retirees must withdraw a specific percentage of their account balance each year, based on their age and life expectancy. RMDs can provide a more personalized and flexible withdrawal strategy, although they may not be suitable for all retirees. Annuities and other guaranteed income products can provide retirees with a stable source of income during retirement, regardless of market conditions. These products can be used in conjunction with the 4% rule or other withdrawal strategies to create a diversified and secure retirement income plan. The age at which an individual retires can have a significant impact on the appropriate withdrawal rate. Those who retire early may need to use a lower withdrawal rate to ensure their savings last for a longer retirement period, while those who retire later may be able to use a higher withdrawal rate. The expected duration of an individual's retirement is another important factor to consider when determining an appropriate withdrawal rate. Those with longer life expectancies may need to use a lower withdrawal rate to avoid outliving their savings. An individual's risk tolerance can also play a role in determining the appropriate withdrawal rate. Those with a higher risk tolerance may be more comfortable using a higher withdrawal rate, while those with a lower risk tolerance may prefer a more conservative approach. The 4% rule has served as a valuable starting point for retirement planning, offering a simple and historically successful guideline for managing retirement savings. However, it's crucial for retirees to understand its limitations and consider other factors that may impact their withdrawal strategy. By recognizing the limitations of the 4% rule, such as its reliance on historical data and inflexibility in changing market conditions, retirees can make more informed decisions about their retirement income planning and explore alternative strategies that may better suit their needs. Ultimately, a successful retirement withdrawal strategy should be tailored to an individual's unique needs, risk tolerance, and financial goals. Definition of the 4% Rule

Understanding the 4% Rule

Calculation of Withdrawal Rate

Inflation Adjustment

Relationship to Portfolio Value

Asset Allocation Recommendations

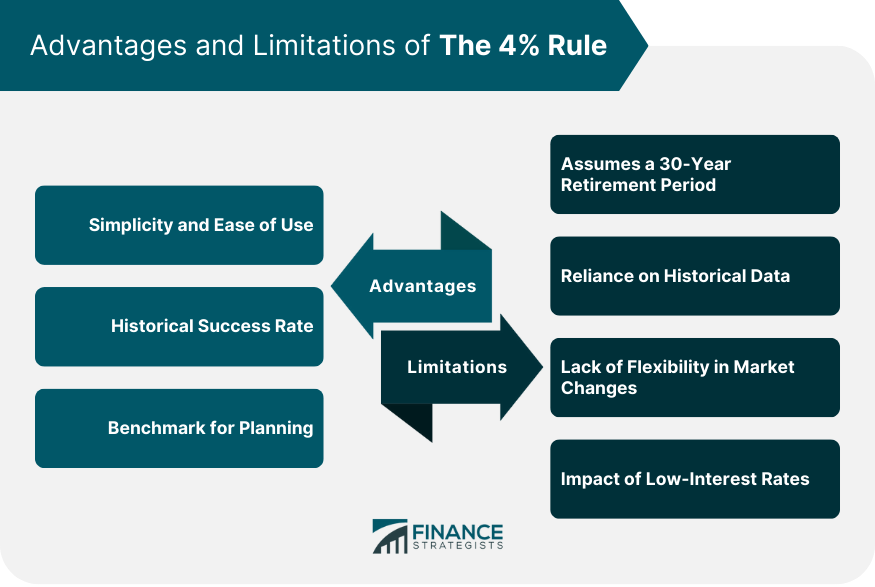

Advantages of the 4% Rule

Simplicity and Ease of Use

Historical Success Rate

Provides a Benchmark for Retirement Planning

Limitations of the 4% Rule

Assumes a 30-Year Retirement Period

Reliance on Historical Data

Lack of Flexibility in Changing Market Conditions

Potential Impact of Low-Interest Rates and High Market Valuations

Alternative Withdrawal Strategies

Variable Withdrawal Rates

Percentage-Based Withdrawals

Adjustments for Market Performance

Dynamic Withdrawal Strategies

Guyton-Klinger Rules

Required Minimum Distributions (RMDs)

Annuities and Guaranteed Income Products

Tailoring the 4% Rule to Individual Needs

Factors Affecting Withdrawal Rates

Retirement Age

Retirement Duration

Personal Risk Tolerance

The Bottom Line

The 4% Rule FAQs

The 4% rule is a widely-used guideline in retirement planning, suggesting that retirees can withdraw 4% of their investment portfolio's value in the first year of retirement and adjust the amount for inflation in subsequent years. This rule aims to provide a steady income stream while minimizing the risk of depleting savings over a 30-year period.

The 4% rule accounts for inflation by adjusting the withdrawal amount each year based on the previous year's withdrawal and the rate of inflation. This helps retirees maintain a consistent standard of living throughout their retirement, even as their purchasing power is affected by inflation.

The main limitations of the 4% rule include its assumption of a fixed 30-year retirement period, reliance on historical data, lack of flexibility in changing market conditions, and potential impact of low interest rates and high market valuations. These limitations can expose retirees to the risk of running out of money sooner than anticipated or not generating sufficient income during retirement.

Alternative withdrawal strategies include variable withdrawal rates (percentage-based withdrawals or adjustments for market performance), dynamic withdrawal strategies (Guyton-Klinger rules or required minimum distributions), and annuities or guaranteed income products. These alternatives can provide more flexibility and adaptability in retirement income planning.

When using the 4% rule, retirees should consider factors like their retirement age and expected retirement duration. Those who retire early may need to use a lower withdrawal rate to ensure their savings last for a longer period, while those who retire later may be able to use a higher withdrawal rate. Periodic reassessment and adjustment of the withdrawal strategy can also help retirees adapt to changing circumstances and maintain a secure retirement income.