Inflation-protected securities (IPS) are financial instruments designed to shield investors from the eroding effects of inflation. These debt instruments, typically issued by governments or corporations, have their principal and interest payments adjusted to keep pace with inflation. As a result, they offer a reliable and predictable return on investment for those seeking protection against rising prices. IPS act as a hedge against inflation, which is the general increase in prices of goods and services over time. By linking principal and interest payments to a measure of inflation, such as the Consumer Price Index (CPI), these securities offer investors a way to maintain their purchasing power. This makes them particularly appealing during periods of high inflation or when investors expect inflation to rise in the future. Inflation-protected securities are typically structured as bonds, with a fixed maturity date and periodic interest payments. The principal amount of the bond is adjusted for inflation, and the interest payments are based on the adjusted principal. This ensures that both the principal and interest payments rise with inflation, maintaining the investor's real return. The inflation adjustments for IPS are made by linking the principal and interest payments to a specific inflation index, such as the CPI. This index tracks changes in the overall level of prices for a basket of goods and services. As the index rises, the principal and interest payments on the security are adjusted upward, ensuring the investor's real return remains constant. The real interest rate represents the nominal interest rate adjusted for inflation. IPS offer investors a way to earn a real return that is protected from the effects of inflation. This can be an attractive feature for long-term investors or those seeking a reliable source of income that maintains its purchasing power over time. TIPS are U.S. government-issued bonds that offer investors protection against inflation. The principal and interest payments for TIPS are adjusted based on the CPI, ensuring that investors receive a real return that is protected from rising prices. These securities are considered very low-risk, as they are backed by the full faith and credit of the U.S. government. Series I Savings Bonds are another type of inflation-protected security issued by the U.S. government. These bonds also adjust their principal and interest payments based on the CPI, but they have some unique features, such as tax deferral and a guaranteed minimum interest rate. They are intended for individual investors and can be purchased in small denominations. Some corporations issue inflation-linked bonds as a way to raise capital while providing investors with protection against inflation. These securities function similarly to TIPS, with their principal and interest payments adjusted based on a specified inflation index. However, they carry a higher degree of risk compared to government-issued IPS due to the potential for default. Several countries around the world issue their own inflation-protected securities, providing investors with additional opportunities for diversification. These securities are similar to TIPS, with their principal and interest payments adjusted based on a specific inflation index. Investing in international IPS can expose investors to currency risk, but it can also offer additional protection against inflation in different economies. One of the primary benefits of IPS is their ability to shield investors from the negative effects of inflation. By adjusting the principal and interest payments for inflation, these securities provide a reliable source of income that maintains its purchasing power over time. This can be particularly valuable during periods of high inflation or when investors expect inflation to rise in the future. Adding inflation-protected securities to an investment portfolio can help investors achieve diversification and reduce overall portfolio risk. By including assets that perform differently under various economic conditions, investors can protect their portfolio from the impact of inflation and other market fluctuations. This diversification can help smooth out returns and potentially enhance long-term investment performance. Inflation-protected securities typically exhibit lower volatility compared to other types of fixed-income investments, such as conventional bonds. This is because their principal and interest payments are adjusted for inflation, reducing the impact of inflation-related fluctuations on their market value. This lower volatility can make IPS an attractive option for conservative investors or those seeking to preserve capital. While IPS offer protection against inflation, they are still subject to interest rate risk. When interest rates rise, the market value of existing bonds typically falls, including inflation-protected securities. Although the impact of interest rate changes on IPS may be less severe compared to conventional bonds, it is still an important risk factor for investors to consider. Inflation-protected securities can be less liquid than other fixed-income investments, particularly those issued by corporations or foreign governments. This means that it might be more difficult to buy or sell these securities in the secondary market at a desirable price. Investors should be aware of the liquidity risk associated with certain types of IPS and factor this into their investment decisions. Although the interest payments from IPS are adjusted for inflation, the inflation adjustment to the principal amount can be subject to taxes. This means that investors may owe taxes on the "phantom income" resulting from the inflation adjustment, even though they have not yet received any cash from the investment. Investors should consult with a tax professional to understand the tax implications of investing in IPS. IPS generally offer lower nominal interest rates compared to conventional bonds, reflecting their built-in inflation protection. While this can be an advantage during periods of high inflation, it can also result in lower total returns compared to other investments during periods of low inflation or deflation. Investors should weigh the potential trade-offs between inflation protection and return potential when considering IPS. Investors who prefer fixed-income investments but are not concerned about inflation protection might consider conventional bonds. These securities offer regular interest payments and are issued by governments, corporations, or other entities. Although they do not adjust for inflation, conventional bonds can provide investors with a stable source of income and potential capital gains. Real estate investments, such as rental properties or real estate investment trusts (REITs), can serve as an alternative to inflation-protected securities. Real estate can act as a hedge against inflation because property values and rental income often rise with inflation. However, real estate investments can be more complex and illiquid compared to IPS and may require additional management and expertise. Dividend-paying stocks can offer investors a source of income and potential capital appreciation. Some companies regularly increase their dividend payments, which can help protect investors from the effects of inflation. However, dividend-paying stocks can be more volatile than IPS and carry the risk of capital loss if the stock price declines. Investing in commodities, such as gold, oil, or agricultural products, can offer some protection against inflation. Commodities often perform well during periods of high inflation because their prices tend to rise with the general increase in the cost of goods and services. However, commodities can be more volatile and speculative compared to IPS, and their performance can be affected by various factors, such as supply and demand dynamics or geopolitical events. Inflation-protected securities can play a valuable role in a long-term investment strategy, particularly for those seeking a reliable source of income that maintains its purchasing power over time. By offering protection against inflation and diversification benefits, IPS can help investors preserve capital and enhance overall portfolio performance. When deciding whether to invest in inflation-protected securities, individual investors should consider factors such as their investment objectives, risk tolerance, and time horizon. IPS may be more suitable for conservative investors or those with a longer time horizon, as they can help protect against the erosion of purchasing power caused by inflation over time. Investing in inflation-protected securities involves a trade-off between inflation protection and return potential. While IPS offer protection against rising prices, they typically provide lower nominal interest rates compared to other investments. Investors should carefully weigh these trade-offs and consider diversifying their portfolio with a mix of assets to achieve their desired risk and return objectives.Definition of Inflation-Protected Securities

How Inflation-Protected Securities Work

Bond Structure and Mechanics

Adjustments for Inflation

Real Interest Rates and Returns

Types of Inflation-Protected Securities

Treasury Inflation-Protected Securities (TIPS)

Series I Savings Bonds

Inflation-Linked Corporate Bonds

International Inflation-Protected Securities

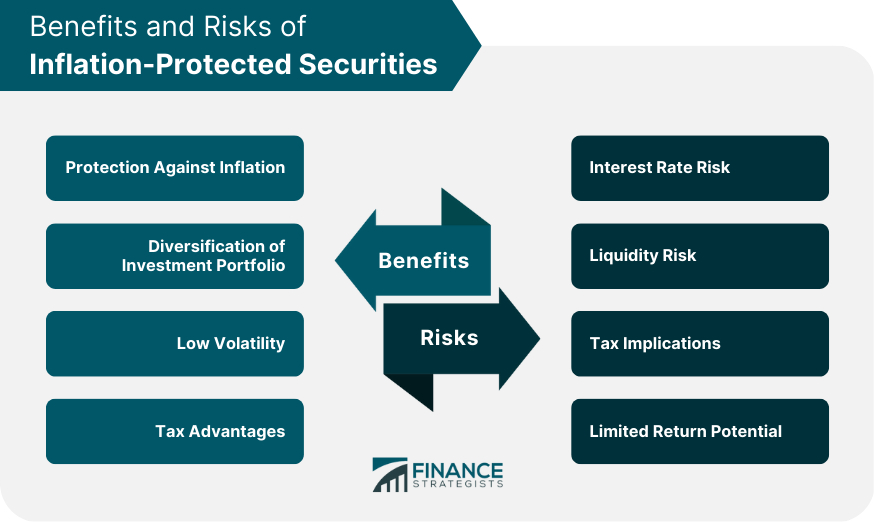

Benefits of Inflation-Protected Securities

Protection Against Inflation

Diversification of Investment Portfolio

Low Volatility

Risks Associated with Inflation-Protected Securities

Interest Rate Risk

Liquidity Risk

Tax Implications

Limited Return Potential

Alternatives to Inflation-Protected Securities

Conventional Bonds

Real Estate Investments

Dividend-Paying Stocks

Commodities

Final Thoughts

Inflation-Protected Securities FAQs

Inflation-protected securities (IPS) are investment instruments that provide protection against inflation by adjusting their principal value based on changes in the Consumer Price Index (CPI).

The most common type of inflation-protected securities are Treasury Inflation-Protected Securities (TIPS), issued by the US government. Other types include inflation-linked bonds issued by corporations and inflation-indexed annuities.

Investing in IPS can provide protection against inflation, diversify an investment portfolio, offer low volatility, and provide tax advantages.

IPS can carry risks such as interest rate risk, liquidity risk, and limited return potential. They can also have tax implications, which investors should consider.

Investors can invest in IPS through various avenues, including mutual funds, exchange-traded funds (ETFs), or by purchasing IPS directly from the US Treasury through TreasuryDirect.gov. It's important to do your research and consult with a financial advisor before making any investment decisions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.