Social Security, a crucial component of the American safety net, provides financial benefits to individuals who are retired or disabled. Established in 1935 and funded by payroll taxes, the program offers monthly payments based on an individual's lifetime earnings once they reach eligibility. It serves as an indispensable part of retirement plans for many Americans, with nearly 90% of those aged 65 and older relying on these benefits. Notably, these payments form approximately 33% of the elderly's income, and for about half of married couples and 70% of unmarried individuals, Social Security contributes to at least 50% of their retirement income. Thus, Social Security plays an essential role in ensuring financial stability for millions of retirees. In unequivocal terms, Social Security is indeed considered retirement income. It is one of the most reliable and consistent sources of income for retirees. Social Security operates as a pay-as-you-go system where current workers pay into the system via payroll taxes, and these funds are then distributed to current retirees as monthly benefits. The amount an individual receives in retirement is calculated based on their 35 highest-earning years in the workforce. Moreover, the age at which an individual decides to begin claiming Social Security also impacts the amount of monthly benefit they receive. If you claim Social Security before your full retirement age (which is between 66 and 67 for people born after 1943), your benefits will be permanently reduced. Conversely, if you delay claiming past your full retirement age, your benefits increase until you reach the age of 70. The timing of retirement significantly influences Social Security benefits. By waiting until your full retirement age or even delaying until you're 70, you can increase the size of your monthly benefit. For example, if your full retirement age is 67, claiming at 62 would reduce your benefits by 30%, while waiting until 70 could increase your benefits by 24%. This is a critical consideration for those relying heavily on Social Security for their retirement income. Your Social Security benefits are based on your lifetime earnings. Specifically, the Social Security Administration calculates your average indexed monthly earnings during the 35 years in which you earned the most. So, the more you earn (up to the taxable maximum), and the longer you work, the higher your benefits will be. One of the unique features of Social Security is that the benefits are adjusted for inflation. Each year, the Social Security Administration applies a cost-of-living adjustment (COLA) to benefits to ensure they maintain their buying power. The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), and can significantly impact the amount of retirement income received over time. While Social Security benefits provide a crucial income source for many retirees, it's also important to understand the potential tax implications. Depending on your total income and marital status, a portion of your Social Security benefits may be taxable. At the federal level, up to 85% of your benefits could be subject to income tax. Furthermore, some states also tax Social Security benefits, adding another layer of complexity to retirement income planning. By postponing the claim of your Social Security benefits past your full retirement age, you can receive a larger monthly benefit. For each year you delay, up to age 70, your monthly benefits can increase by about 8%. Married individuals are entitled to receive either benefits based on their own work record or 50% of their spouse's full retirement benefit, whichever is higher. Understanding these spousal benefits can provide a significant boost to your retirement income. If your spouse passes away, you may be eligible for survivor benefits. Depending on various factors, including your age and the age of your deceased spouse at the time of passing, you could receive 100% of your deceased spouse's benefit. Proactive income planning can help minimize the portion of your Social Security benefits subject to tax. By managing other sources of income and timing your benefit claims wisely, you could potentially reduce or even eliminate tax on your Social Security benefits. Pension plans provide a monthly income in retirement and are typically funded by employers. They differ from Social Security as their payouts are often based on your salary and years of service, rather than your lifetime earnings. 401(k) plans are a popular employer-sponsored retirement savings vehicle. Unlike Social Security, these plans allow individuals to contribute a portion of their pre-tax salary, which can then grow tax-deferred until retirement. IRAs are retirement accounts that you set up and manage yourself. They offer more control over your investments than Social Security and can provide additional tax advantages. Personal savings and investments can provide a flexible supplement to your Social Security benefits. These might include income from rental properties, dividend-paying stocks, or interest from savings accounts. Social Security serves as a crucial pillar of retirement income for many Americans, providing a safety net through guaranteed, inflation-adjusted payments that counter the risk of outliving one's savings. This program, which for many represents a significant or even majority share of retirement income, requires strategic planning to fully leverage. The complexities of Social Security, including determining the optimal time to claim benefits, comprehending tax implications, and grasping potential spousal and survivor benefits, necessitate informed decision-making for maximum income during retirement. Beyond Social Security, a comprehensive retirement plan should incorporate other income sources like personal savings, pension plans, 401(k)s, IRAs, and other investments, fostering financial stability and resilience against unforeseen economic changes. Professional guidance can be invaluable in navigating Social Security rules and maximizing your benefits and overall retirement income.Overview of Social Security

Is Social Security Considered Retirement Income?

Factors Influencing Social Security as Retirement Income

Age of Retirement and Social Security Benefit Amounts

Lifetime Earnings and Social Security Benefit Calculation

Inflation and Cost-Of-Living Adjustments

Tax Implications of Social Security Benefits

Strategies to Maximize Social Security Benefits for Retirement

Delaying Benefit Claiming

Understanding the Spousal Benefits

Taking Advantage of Survivor Benefits

Income Planning to Minimize Tax on Benefits

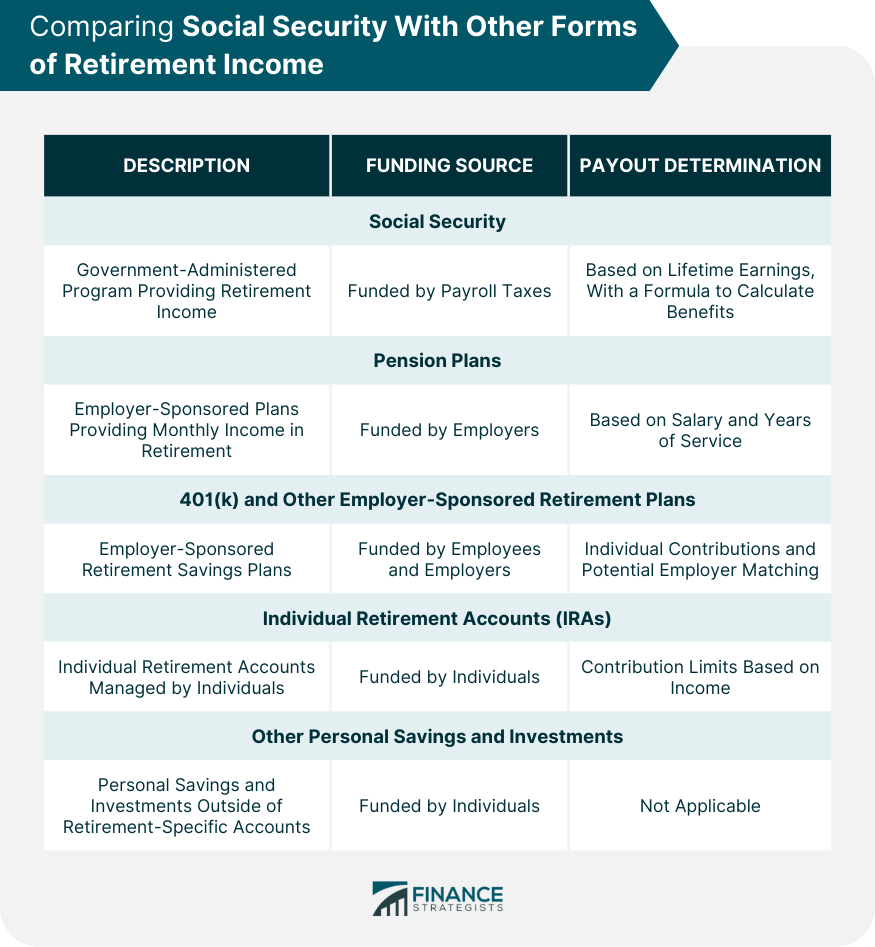

Comparing Social Security With Other Forms of Retirement Income

Pension Plans

401(k) and Other Employer-Sponsored Retirement Plans

Individual Retirement Accounts (IRAs)

Other Personal Savings and Investments

The Bottom Line

Is Social Security Considered Retirement Income? FAQs

Yes, Social Security is indeed considered retirement income. It is a consistent and reliable source of income for many retirees.

Social Security provides monthly benefits to retirees based on their lifetime earnings, the age at which they begin claiming benefits, and yearly cost-of-living adjustments.

While Social Security can be a substantial part of retirement income, it's often not enough to cover all expenses. Hence, it's beneficial to have additional sources of retirement income like personal savings, pensions, or investments.

The age at which you begin claiming Social Security can significantly impact your retirement income. Benefits are reduced if you claim before your full retirement age and increased if you delay until after.

Yes, there are several strategies such as delaying benefit claims, understanding spousal and survivor benefits, and income planning to minimize tax on benefits.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.