Accepting risk in finance refers to an individual's or organization's willingness to assume a certain level of uncertainty and potential loss when making investment decisions. It is a critical component of financial planning, as it influences the choice of investment instruments, asset allocation, and overall investment strategy. Embracing risk is vital in the world of finance because it determines the potential returns an investor can expect. Generally, the higher the risk, the higher the potential rewards. By acknowledging and accepting risks, investors can make informed decisions that balance potential gains against potential losses, ultimately optimizing their investment portfolios. Risk tolerance is the degree to which an investor is comfortable with the possibility of losing money on their investments. It is influenced by numerous factors, such as an individual's financial situation, age, and investment objectives. 1. Financial Resources: Investors with more disposable income or higher net worth are likely to have a higher risk tolerance. 2. Age: Younger investors typically have a higher risk tolerance because they have more time to recover from potential losses. 3. Investment Objectives: Individuals with aggressive financial goals may be more willing to take on higher risks. 4. Past Experiences: Investors who have experienced significant losses in the past may have a lower risk tolerance. Short-term financial goals are objectives that an investor aims to achieve within a few months or years. Examples include saving for a vacation, building an emergency fund, or paying off a specific debt. These goals typically require less risk-taking, as investors need to preserve their capital and ensure liquidity. Long-term financial goals are objectives that an investor aims to achieve over several years or even decades. Examples include saving for retirement, funding a child's education, or purchasing a home. These goals often necessitate a higher degree of risk-taking, as investors must account for factors such as inflation and seek higher returns to meet their objectives. The time horizon, or the period between the initial investment and the point at which an investor needs to access their funds, plays a significant role in risk acceptance. A longer time horizon allows investors to take on more risk, as they have more time to recover from potential losses and capitalize on the compounding effect of their investments. Different investment strategies are suitable for different time horizons. For instance, investors with a short time horizon may prioritize capital preservation and opt for low-risk investments, such as bonds or money market funds. Conversely, investors with a long time horizon may seek growth and invest in higher-risk assets, such as stocks or real estate. Diversification is a risk management technique that involves spreading investments across various asset classes, industries, and geographical regions. By doing so, investors can minimize the impact of poor-performing investments and reduce the overall risk of their portfolios. 1. Asset Allocation: Distributing investments across different asset classes, such as stocks, bonds, and cash. 2. Sector Diversification: Investing in various industries to reduce the impact of sector-specific risks. 3. Geographic Diversification: Investing in different countries or regions to mitigate the effects of regional economic fluctuations. 4. Investment Style Diversification: Allocating funds to different investment styles, such as growth, value, or income-oriented investments. Market risk, also known as systematic risk, refers to the potential for an investment to lose value due to broad market factors, such as economic conditions, interest rates, or political events. Market risk is inherent to all investments and cannot be eliminated through diversification. 1. Economic Conditions: Recessions, inflation, and changes in consumer sentiment can affect market performance. 2. Interest Rates: Fluctuations in interest rates can impact the value of fixed-income investments and influence the cost of borrowing for companies. 3. Political Events: Government policies, elections, and geopolitical tensions can create uncertainty and affect market performance. 4. Market Sentiment: Investor confidence and behavioral factors can lead to market volatility. Credit risk, also known as default risk, is the possibility that a borrower will fail to repay a loan or meet their financial obligations, resulting in a loss for the lender or investor. 1. Individual Credit Risk: The risk that a specific borrower will default on their obligations. 2. Portfolio Credit Risk: The risk that multiple borrowers within a portfolio will default, leading to significant losses. 3. Sovereign Credit Risk: The risk that a government will default on its debt obligations or restructure its debt, affecting bondholders and other creditors. Liquidity risk refers to the potential difficulty of converting an asset into cash quickly and without significant loss in value. This risk is particularly relevant for investments in illiquid assets, such as real estate or thinly traded securities. Liquidity risk can affect an investor's ability to access funds when needed or to exit an investment at a fair price. Understanding and accepting this risk is essential when selecting investments and managing a portfolio, as it can have a significant impact on overall performance and financial flexibility. Operational risk is the potential for loss resulting from inadequate or failed internal processes, people, systems, or external events. This type of risk can affect the performance of individual investments or the functioning of the financial system as a whole. 1. Human Error: Mistakes or misconduct by employees can lead to financial losses or reputational damage. 2. System Failures: Technical issues, such as hardware or software malfunctions, can disrupt operations and result in losses. 3. External Events: Natural disasters, terrorist attacks, or cyber threats can negatively impact businesses and financial institutions. 4. Regulatory and Legal Risks: Changes in regulations or legal disputes can have significant financial and operational consequences. Risk assessment is the process of identifying, analyzing, and evaluating the potential risks associated with investment decisions to make informed choices and implement effective risk management strategies. 1. Quantitative Analysis: Utilizing statistical measures, such as standard deviation or beta, to gauge investment risk. 2. Qualitative Analysis: Assessing factors like management quality, competitive advantages, and industry trends to evaluate investment risk. 3. Scenario Analysis: Exploring potential outcomes under various market conditions to understand the possible impact on investments. Hedging involves taking positions in financial instruments designed to offset potential losses in an investment portfolio. Examples include using options, futures, or inverse ETFs. Insurance products, such as annuities or life insurance policies, can help protect against certain financial risks, such as longevity risk or the loss of income due to disability. Allocating investments across different asset classes can help manage risk by diversifying a portfolio and balancing the potential for growth and capital preservation. Regularly reviewing an investment portfolio helps ensure that risk levels remain aligned with an investor's objectives, risk tolerance, and time horizon. Changes in market conditions or personal circumstances may necessitate adjustments to maintain an appropriate risk profile. Investors can adjust their risk exposure by rebalancing their portfolios, changing their asset allocation, or employing different risk management strategies, such as hedging or insurance. Fear and greed can drive investors to make irrational decisions, such as selling investments during market downturns or taking excessive risks in pursuit of high returns. Overconfidence can lead investors to underestimate risks, while loss aversion can cause them to hold onto losing investments for too long in the hope of a recovery. Confirmation bias is the tendency to seek out information that supports one's existing beliefs, potentially leading to a skewed perception of investment risks. Anchoring bias occurs when investors rely too heavily on an initial piece of information, such as a stock's historical price, when making investment decisions, potentially ignoring more relevant data. Increasing financial literacy and understanding the psychological factors that influence decision-making can help investors make more rational choices when accepting risk. Working with a financial advisor or wealth manager can provide valuable guidance and help investors navigate the complexities of risk acceptance and investment management. Accepting risk is a crucial aspect of investment decision-making. It involves embracing uncertainty and potential loss in order to achieve higher potential rewards. Risk acceptance is influenced by factors such as risk tolerance, financial goals, time horizon, and the use of diversification techniques. Understanding and measuring various types of financial risks, including market risk, credit risk, liquidity risk, and operational risk, is essential for effective risk management. Strategies like hedging, insurance, and asset allocation can help mitigate risk. Regular monitoring and adjustment of risk exposure are important to ensure that investment portfolios remain aligned with an individual's goals and risk tolerance. Additionally, being aware of the psychological factors that influence risk acceptance, such as fear, overconfidence, and cognitive biases, can help investors make more rational decisions. Seeking professional advice and increasing financial literacy are valuable strategies for overcoming psychological barriers.What Is Accepting Risk?

Factors Influencing Risk Acceptance

Risk Tolerance

Factors Affecting Risk Tolerance

Financial Goals

Short-Term Goals

Long-Term Goals

Time Horizon

Importance in Risk Acceptance

Time Horizon and Investment Strategies

Diversification

Diversification Techniques

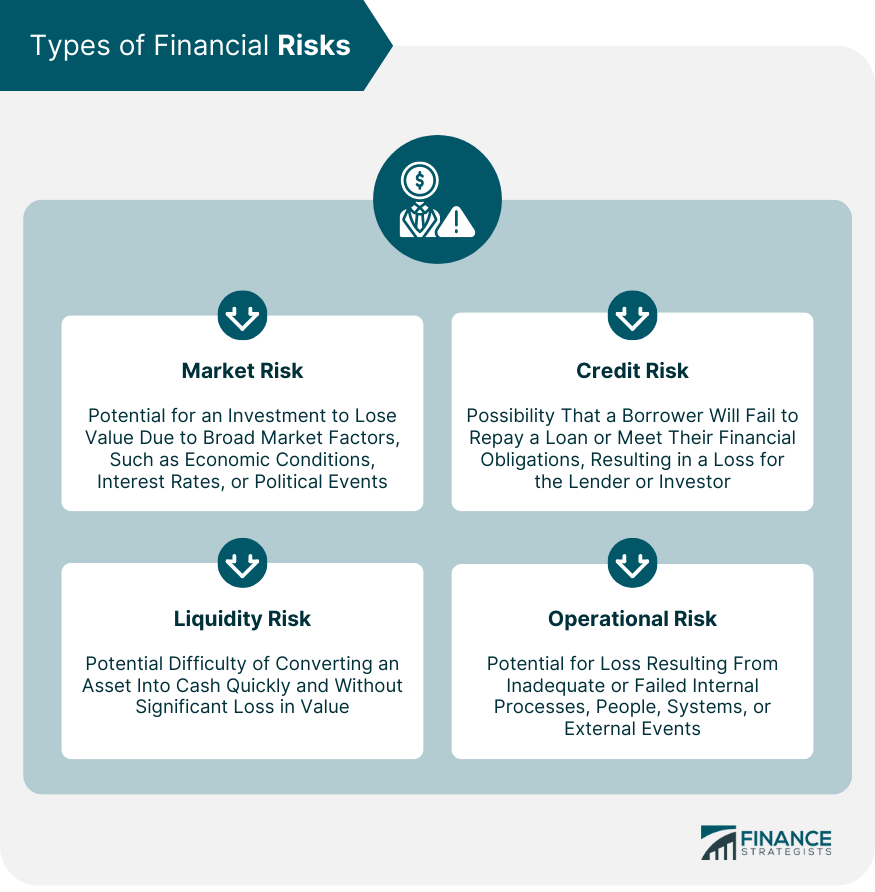

Types of Financial Risks

Market Risk

Factors Contributing to Market Risk

Credit Risk

Types of Credit Risk

Liquidity Risk

Operational Risk

Factors Contributing to Operational Risk

Measuring and Managing Risk

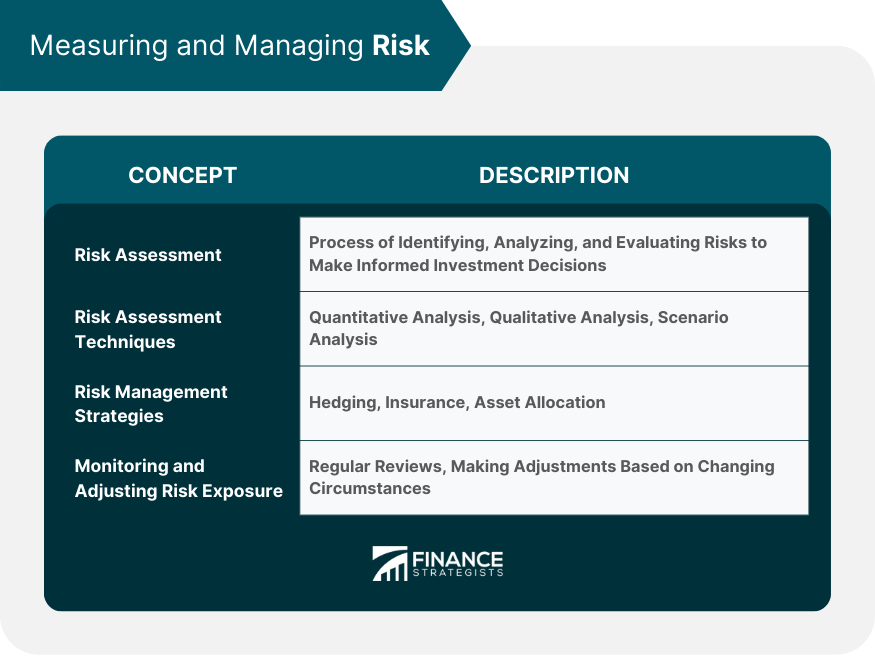

Risk Assessment

Risk Assessment Techniques

Risk Management Strategies

Hedging

Insurance

Asset Allocation

Monitoring and Adjusting Risk Exposure

Importance of Regular Reviews

Making Adjustments Based on Changing Circumstances

Psychology of Accepting Risk

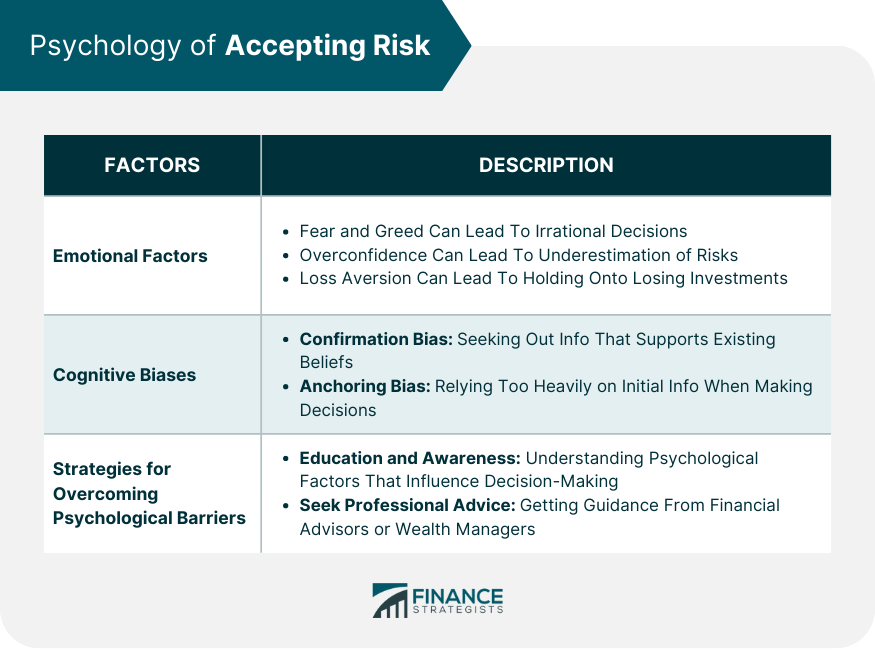

Emotional Factors

Fear and Greed

Overconfidence and Loss Aversion

Cognitive Biases

Confirmation Bias

Anchoring Bias

Strategies for Overcoming Psychological Barriers

Education and Awareness

Seeking Professional Advice

Final Thoughts

Accepting Risk FAQs

Accepting risk in finance refers to an investor's willingness to assume a certain level of uncertainty and potential loss when making investment decisions.

Accepting risk affects investment decisions by influencing the choice of investment instruments, asset allocation, and overall investment strategy.

Factors that influence risk acceptance include risk tolerance, financial goals, time horizon, and diversification.

Investors can measure and manage risk by conducting risk assessments, implementing risk management strategies like hedging or insurance, and regularly reviewing and adjusting their risk exposure.

Understanding the psychology of accepting risk is important because emotional factors and cognitive biases can influence investment decisions and potentially lead to suboptimal outcomes.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.