Withdrawal strategies refer to the methods used by retirees to access their savings and investment accounts to provide income during retirement. These strategies can have a significant impact on the sustainability of a retiree's financial resources, as well as their overall financial well-being. Choosing an appropriate withdrawal strategy can help maximize the longevity of one's retirement funds and minimize the risk of outliving one's savings. Several factors play a role in determining the most suitable withdrawal strategy for an individual, including their financial goals, risk tolerance, and investment portfolio. The retiree's age, health, and expected retirement duration should also be considered. Understanding these factors and their interplay can help retirees create a tailored withdrawal strategy that ensures financial security throughout their retirement years. There are various types of withdrawal strategies that retirees can adopt, each with its own set of advantages and drawbacks. The following sections describe some common approaches to retirement income withdrawal. Systematic withdrawal strategies involve regular withdrawals from a retiree's investment accounts to provide a steady stream of income. These strategies can be categorized into fixed-dollar, inflation-adjusted, and fixed-percentage withdrawals. Fixed-dollar withdrawals involve withdrawing a predetermined dollar amount annually, whereas inflation-adjusted withdrawals increase the withdrawal amount each year based on inflation. Fixed-percentage withdrawals, on the other hand, involve withdrawing a set percentage of the portfolio's value each year. The Required Minimum Distribution (RMD) strategy is based on the minimum amounts that retirees must withdraw from their tax-advantaged accounts, such as 401(k)s and IRAs, starting at age 72. This approach ensures that retirees take the necessary distributions to avoid tax penalties and meet their living expenses. However, RMD-based strategies may not provide the most optimal income stream, depending on an individual's specific circumstances. The bucket strategy divides a retiree's investment portfolio into separate "buckets," each with a different time horizon and investment objective. Typically, the first bucket contains conservative investments designed to provide income for the initial years of retirement, while subsequent buckets hold more aggressive investments intended for later years. Annuity-based strategies involve purchasing an annuity product from an insurance company to guarantee a fixed income stream during retirement. Annuities can be immediate or deferred, and they can provide income for a fixed period or for the retiree's entire lifetime. Although annuities can offer financial security and predictability, they may also be less flexible than other withdrawal strategies and can come with high fees. Dynamic withdrawal strategies adjust withdrawal amounts based on market conditions and changes in a retiree's financial circumstances. This approach seeks to preserve retirement funds during periods of market downturns and may involve reducing spending or adjusting asset allocations. While potentially more complex than other strategies, dynamic withdrawal approaches can help retirees maintain financial stability in the face of market volatility. When selecting a withdrawal strategy, several factors should be taken into account to ensure a comfortable and sustainable retirement. A retiree's financial goals and needs should be the primary considerations when choosing a withdrawal strategy. Factors such as desired lifestyle, expected expenses, and potential financial commitments should be assessed to determine the most suitable approach. A comprehensive understanding of one's financial objectives can help create a withdrawal strategy that meets both short-term and long-term needs. The investment time horizon, or the length of time a retiree expects to rely on their retirement funds, is a critical factor in selecting a withdrawal strategy. A longer time horizon may require a more conservative approach to preserve assets, while a shorter time horizon may allow for greater flexibility in withdrawals. Retirees should consider their life expectancy and retirement duration when developing their withdrawal plan. A well-diversified investment portfolio can help reduce risk and ensure a more stable income stream during retirement. Retirees should review their asset allocation to ensure it aligns with their risk tolerance and financial objectives. A balanced portfolio that includes a mix of stocks, bonds, and cash investments can help manage market fluctuations and minimize the impact of market downturns on retirement income. The tax implications of different withdrawal strategies can significantly impact a retiree's net income. Retirees should consider the tax treatment of their various income sources, such as tax-deferred accounts, taxable accounts, and Social Security benefits, when developing their withdrawal strategy. A tax-efficient withdrawal plan can help minimize tax liabilities and maximize after-tax income. The sequence of returns risk refers to the impact of market fluctuations on a retiree's portfolio during the early years of retirement. If a retiree experiences significant market losses early on, their portfolio may not recover in time to provide the necessary income for the remainder of their retirement. To mitigate this risk, retirees should consider incorporating strategies that protect their portfolio from market volatility, such as asset allocation adjustments or dynamic withdrawal approaches. Implementing various strategies can help retirees minimize withdrawal risk and ensure a more secure retirement. One way to minimize withdrawal risk is to delay retirement, allowing for additional time to save and invest. Working longer can also help retirees maintain their standard of living by reducing the number of years they need to rely on their retirement savings. Lowering withdrawal rates can help preserve retirement funds and mitigate the risk of outliving one's savings. Retirees should carefully assess their withdrawal rates to ensure they strike a balance between maintaining their desired lifestyle and preserving their financial resources. Having multiple income sources, such as Social Security, pensions, rental income, or part-time work, can help reduce the reliance on withdrawals from retirement accounts. Diversifying income sources can provide additional financial stability and minimize the impact of market fluctuations on a retiree's overall financial well-being. Tax-advantaged accounts, such as IRAs and 401(k)s, can help retirees save for retirement more efficiently and minimize tax liabilities during the withdrawal phase. By strategically withdrawing from these accounts, retirees can optimize their after-tax income and preserve their financial resources. Regular reviews and adjustments are essential to ensure that a withdrawal strategy remains effective and aligned with a retiree's financial goals. Retirees should periodically review their withdrawal strategy to assess its effectiveness and make any necessary adjustments. Factors such as changes in the market, personal circumstances, or financial goals may necessitate modifications to the withdrawal plan. Market conditions can have a significant impact on a retiree's portfolio and withdrawal strategy. Retirees should be prepared to adapt their withdrawal approach in response to market fluctuations, whether by adjusting asset allocations, withdrawal rates, or other aspects of their strategy. Life events, such as changes in health, family circumstances, or unexpected expenses, can affect a retiree's financial needs and goals. It is essential to reevaluate and adjust the withdrawal strategy to accommodate these changes, ensuring that the plan remains aligned with the retiree's evolving financial objectives and requirements. By understanding the various types of withdrawal strategies and considering key factors such as retirement goals, investment time horizon, and tax implications, retirees can develop a tailored plan that meets their needs. Regularly monitoring and adjusting the strategy in response to changing market conditions and personal circumstances can help maintain financial stability throughout retirement. A well-planned withdrawal strategy is crucial for ensuring a comfortable and sustainable retirement. In conclusion, a comprehensive and adaptable withdrawal strategy is essential for maximizing the longevity of retirement funds and securing a retiree's financial well-being.What Are Withdrawal Strategies?

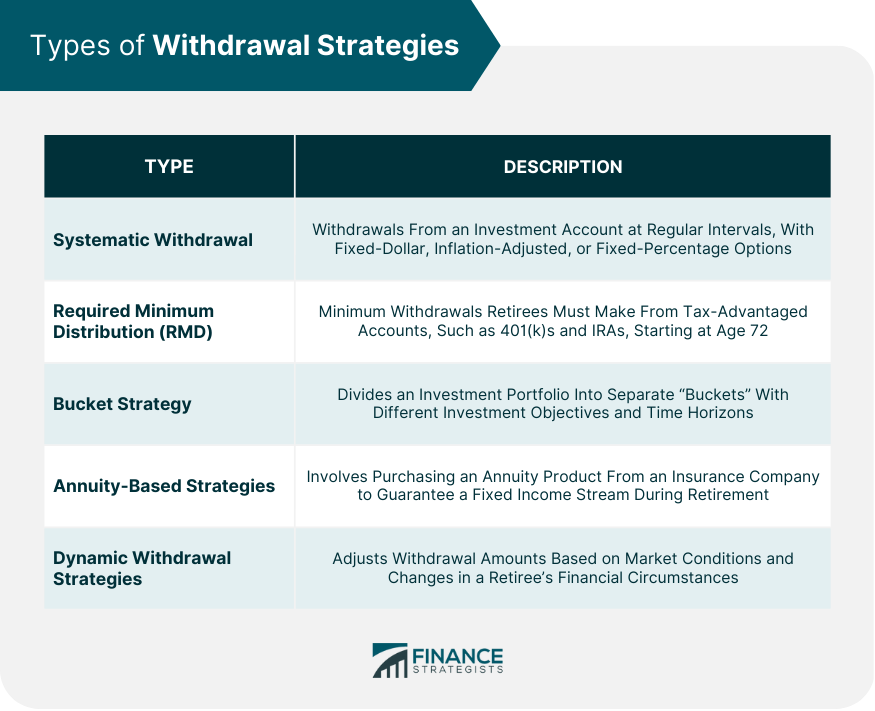

Types of Withdrawal Strategies

Systematic Withdrawal

Required Minimum Distribution (RMD)

Bucket Strategy

Annuity-Based Strategies

Dynamic Withdrawal Strategies

Key Considerations in Developing a Withdrawal Strategy

Retirement Goals and Needs

Investment Time Horizon

Asset Allocation and Diversification

Tax Implications

Sequence of Returns Risk

Strategies to Minimize Withdrawal Risk

Delaying Retirement

Reducing Withdrawal Rates

Diversifying Income Sources

Utilizing Tax-Advantaged Accounts

Monitoring and Adjusting Withdrawal Strategies

Regular Reviews and Adjustments

Adapting to Changing Market Conditions

Addressing Personal and Financial Changes

Conclusion

Withdrawal Strategies FAQs

Withdrawal strategies refer to the methods used to withdraw funds from an investment account or retirement savings plan.

Common types of withdrawal strategies include systematic withdrawals, required minimum distributions, and the 4% rule.

Considerations include your investment goals, risk tolerance, tax implications, and the amount of money you'll need to sustain your lifestyle in retirement.

The risks associated with withdrawal strategies include the potential for outliving your savings, market volatility, inflation, and changes in tax laws.

Yes, you can change your withdrawal strategy over time as your financial situation and goals evolve. However, it's important to carefully consider the implications of any changes you make to your strategy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.