Yes, a 401(k) is indeed considered an asset. A 401(k) is a retirement savings account offered by many employers, and it allows employees to contribute a part of their salary, typically on a pre-tax basis. The money in this account is then invested, often in a mix of stocks, bonds, and mutual funds. Over time, these investments can grow, thereby increasing the value of the 401(k) account. Therefore, a 401(k) is an asset because it holds a monetary value that contributes to your overall net worth. This account becomes particularly significant as a long-term asset aimed at providing income during your retirement years. Its importance in personal finance and retirement planning cannot be overstated. The value of a 401(k) as an asset is determined by several factors, including the amount contributed by the individual (and potentially their employer), the performance of the investments within the account, and the duration of the investment. Within personal finance and retirement planning, a 401(k) is seen as a long-term asset. It's a tool used to prepare for retirement by accumulating wealth over time. The importance of this asset grows as one gets closer to retirement, as it will likely become a primary source of income during those years. A traditional 401(k) provides tax-deferred growth. This means the contributions made into the account are pre-tax dollars, reducing taxable income for the year in which the contributions were made. Taxes are not paid until funds are withdrawn, usually during retirement when many individuals are in a lower tax bracket. One of the main benefits of a 401(k) as an asset is the potential for growth and compounding. Compounding occurs when the returns generated by the investments in your 401(k) begin to generate their own returns. Over time, this can result in exponential growth of your asset. Many employers offer to match the contributions their employees make into their 401(k) accounts up to a certain percentage. This essentially amounts to free money, further increasing the value of the 401(k) as an asset. As previously mentioned, the contributions to a traditional 401(k) are made with pre-tax dollars. This can lower your taxable income for the year. Furthermore, the growth within the account is tax-deferred, meaning you won’t pay taxes on the growth until you start making withdrawals in retirement. While a 401(k) is a powerful asset, it does come with certain restrictions. One of these is the penalty for early withdrawal. If funds are withdrawn before the age of 59.5, a 10% penalty is typically applied, on top of the regular income tax that will be due. Starting at age 72, account holders are required to start taking minimum distributions from their 401(k). This means that each year, a certain minimum amount must be withdrawn. For those hoping to leave their 401(k) untouched for later years or to pass on to heirs, this can be a limitation. Compared to a brokerage account, a 401(k) usually has limited investment choices. While the options typically include a range of mutual funds covering different asset classes and sectors, the selection may not be as broad or flexible as some investors would like. Diversification is a key investment strategy that involves spreading investments across a variety of assets to manage risk. In a 401(k), this could involve a mix of stock and bond funds, for example. The aim is to balance the potential for high returns with the need for security. Strategies for diversifying within a 401(k) might include investing in a mix of funds representing different asset classes, sectors, and geographical regions. Some 401(k) plans also offer target-date funds, which automatically adjust the mix of investments over time based on your projected retirement date. Making regular contributions and gradually increasing the amount you contribute over time can significantly grow your 401(k) asset. Most financial advisors recommend contributing at least enough to get any employer match. Asset allocation – deciding what percentage of your portfolio to dedicate to different types of investments – is a fundamental investment strategy. A well-thought-out asset allocation strategy can help you balance risk and reward within your 401(k). Employer match programs can greatly enhance the value of a 401(k) as an asset. Make sure you understand your employer's 401(k) match program and aim to contribute at least enough to receive the full match. Just like any investment, a 401(k) should be regularly monitored and adjusted as necessary. This can help ensure that the investment strategy remains aligned with changing financial goals and market conditions. 401(k)s offer strong legal protections. They are typically protected from creditors in the event of bankruptcy, providing security for this asset. Understanding the rules around early withdrawals can help protect your 401(k) asset. By avoiding unnecessary early withdrawals, you can keep your asset growing and avoid penalties. A 401(k) is a valuable asset that significantly contributes to one's net worth and provides financial security during retirement. Its value is determined by factors such as individual contributions, potential employer matching, investment performance, and time. These funds offer the potential for compounded growth and tax-deferred advantages and are often augmented by employer-matching contributions. However, it's crucial to understand their restrictions, including penalties for early withdrawal, required minimum distributions after age 72, and limited investment choices. Ensuring diversification within the 401(k) is key to balancing risk and maximizing potential returns. Regular contributions, strategic asset allocation, and leveraging employer match programs are strategies to optimize this asset. Regular monitoring and understanding of the legal protections and rules around 401(k)s further safeguard this crucial retirement asset. Thus, a 401(k) is not only an asset but an essential part of sound financial planning.Is a 401(k) An Asset?

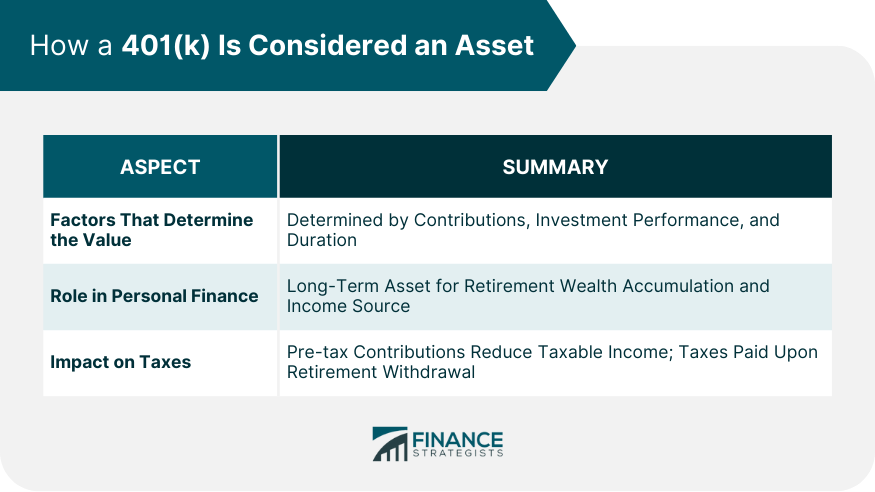

How a 401(k) Is Considered an Asset

Factors That Determine Value

Role in Personal Finance and Retirement Planning

Impact on Taxes

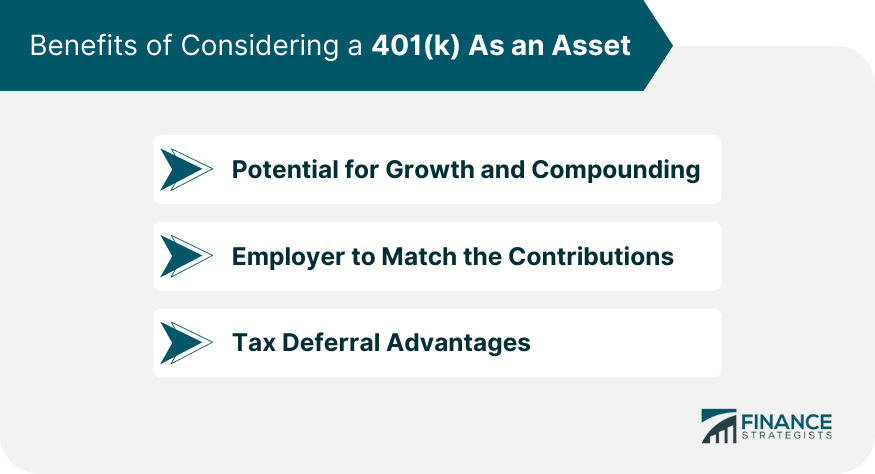

Benefits of Considering a 401(k)As an Asset

Potential for Growth and Compounding

Employer to Match the Contributions

Tax Deferral Advantages

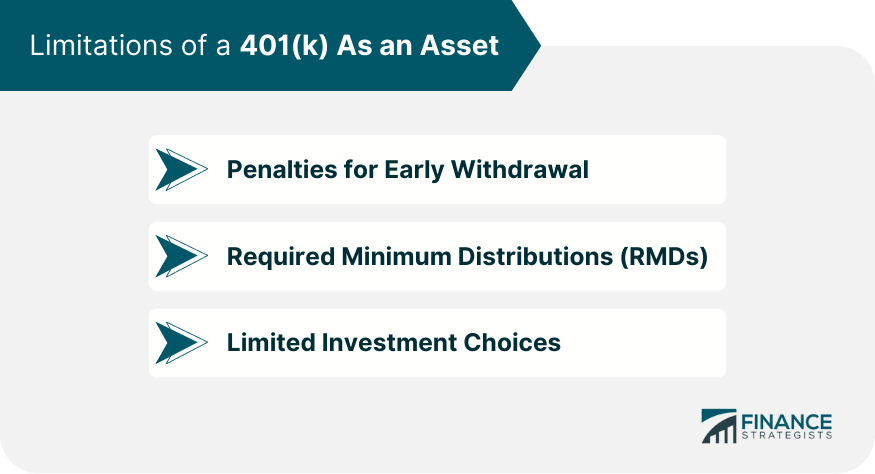

Limitations of a 401(k) As an Asset

Penalties for Early Withdrawal

Required Minimum Distributions (RMDs)

Limited Investment Choices

Role of Diversification in a 401(k)

Importance of Diversification

Strategies for Diversifying Within a 401(k)

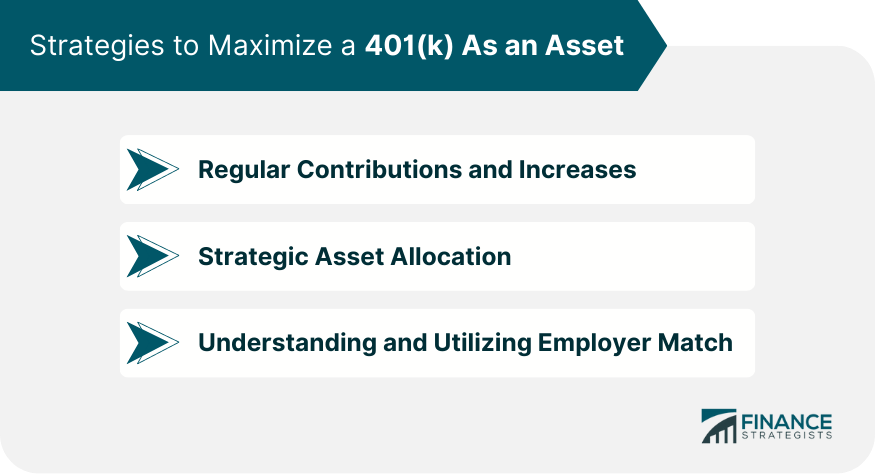

Strategies to Maximize a 401(k) As an Asset

Regular Contributions and Increases

Strategic Asset Allocation

Understanding and Utilizing Employer Match

Safeguarding a 401(k) Asset

Importance of Regular Account Monitoring

Legal Protections for 401(k) Assets

Measures to Avoid Early Withdrawal Penalties

Bottom Line

Is a 401(k) An Asset? FAQs

Yes, a 401(k) is considered an asset because it holds a value that can grow over time, contributing to your overall net worth.

The value of a 401(k) is determined by several factors, including the amount you and possibly your employer contribute, the performance of the investments within the account, and the duration of the investment.

The advantages of a 401(k) as an asset include the potential for growth and compounding, the possibility of employer matching contributions, and the benefits of tax deferral on both contributions and investment returns.

The limitations of a 401(k) as an asset include penalties for early withdrawal, required minimum distributions after age 72, and a typically limited choice of investment options compared to other investment accounts.

You can maximize the growth of your 401(k) by making regular contributions, taking full advantage of any employer matching contributions, strategically allocating your assets within the account, diversifying your investments, and regularly reviewing and adjusting your account as necessary.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.