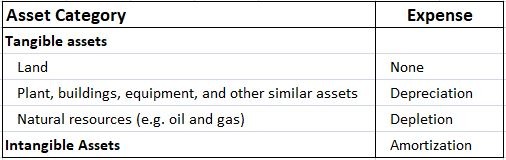

Nonmonetary assets are those assets other than cash are the rights to receive cash, that can generate future revenues, such as property, plant, and equipment. Noncurrent, nonmonetary assets are often broken down into two categories: tangible and intangible; Tangible assets include property, plant; and equipment and other similar productive assets acquired by a company. These assets have physical substance and capabilities. Natural resources also are considered tangible assets. Natural resources are physical substances that, when taken from the ground, produce revenues for a firm. Included in this category are oil, natural gas, coal, iron ore, uranium, and timber. Intangible assets have no physical substance or properties, They benefit a firm because they give to the enterprise the right of ownership or use. Included in this category are patents, copyrights, leaseholds, trademarks, franchises. All noncurrent, nonmonetary assets have the following common Characteristics: Property, plant, and equipment, as well as other noncurrent, nonmonetary assets, are acquired by an enterprise because of their ability to generate future revenues. In effect, these assets are viewed as bundles of future service potentials that are consumed in the firm's merchandising or production cycle. For example, accountants are not concerned with the physical properties of a lathe but rather with its ability to produce a product and thus provide future benefits. Assets that are not used in the merchandising or production process including assets that are held for resale are not included in this category. For example, a warehouse that is no longer being used or land held for speculation is not classified under the category of property, plant) and equipment. Rather, these assets are included in the long-term investment category of the balance sheet. Similarly, land held for resale by a real estate firm is shown in the inventory section of the balance sheet. The economic or service life of a noncurrent, nonmonetary asset is the period of time that a firm expects to receive benefits. from the asset and depends on economic and legal factors. A building generally has an economic life of at least 20 to 30 years; a delivery truck may have a life of 100,000 miles. Intangible assets have a legal life as well as an economic life. For example, a patent has a legal life of 17 years in addition to its economic life, which may be shorter than 17 years. Generally, any asset that has a life of over one year is included in the noncurrent section of the balance sheet. The matching convention requires that the cost of expired benefits be matched with the revenues they helped produce. Accountants do this for all nonmonetary assets (other than land), whether classified as current or noncurrent. For example, prepaid assets such as insurance are written off to ensure that as their benefits expire or are consumed, the asset is reduced and an expense is recorded. Further, various cost flow assumptions are used to allocate total goods available for sale to ending inventory and cost of goods sold. In this article, we will consider how the cost of noncurrent, nonmonetary assets, other than site land, is systematically allocated to future accounting periods. Land is not depreciable because its benefits are considered to last indefinitely. Property, Plant, and Equipment; Natural Resources, and Intangible Assets. Listed below are the major categories of noncurrent, nonmonetary assets and the expenses associated with the cost allocation process: The major Accounting issues related to noncurrent, nonmonetary assets include:What Are Nonmonetary Assets?

Explanation

Bundles of Future Services Not Held for Resale

Long-term Nature of the Nonmonetary Assets

Nonmonetary Assets Allocation of Benefits for Accounting Periods

Major Accounting Issues Associated With Noncurrent, Nonmonetary Assets

Nonmonetary Assets FAQs

Nonmonetary assets refer to items that have a value but do not have a fixed monetary value, such as intangible assets like intellectual property or brand recognition. These assets are used to generate economic benefits for the company and may be used in strategic planning and decision-making.

Nonmonetary assets are typically recorded in the general ledger at their fair market value or other cost basis. The asset should be amortized over its useful life to allocate any changes in value over time.

Examples of nonmonetary assets include patents, copyrights, trademarks, franchises, goodwill, contracts and customer lists.

Nonmonetary assets can have a significant effect on a company's profitability and competitive position in the marketplace. They are often used to generate revenue or as an important part of a company's intangible asset portfolio.

Nonmonetary assets are not typically considered to be liquid, as they have no set exchange rate. They can be sold or used as collateral, but their market value is difficult to determine and may vary depending on the market conditions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.