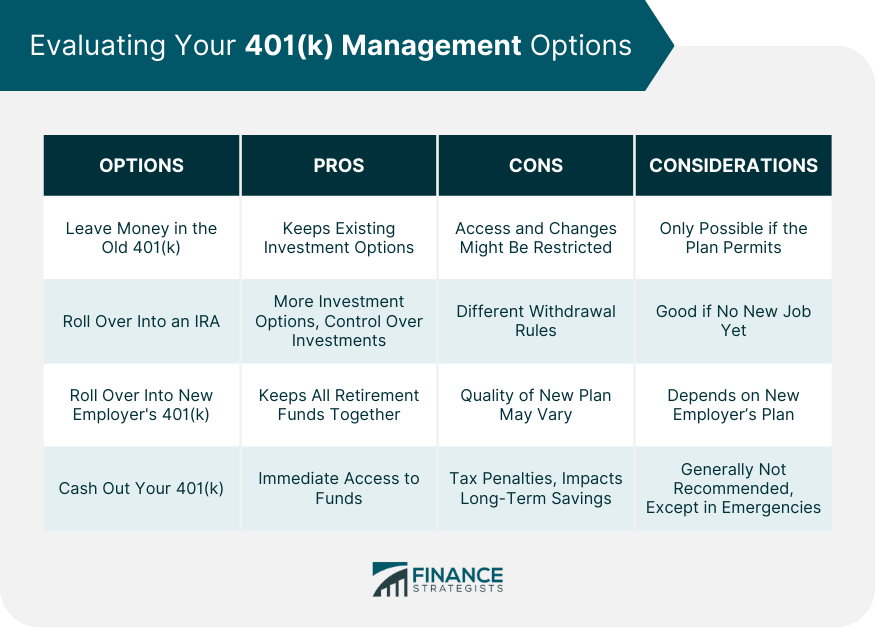

When your company closes, managing your 401(k) effectively is crucial. You essentially have four main options. First, if permitted, you could leave your funds in your old 401(k). Secondly, you can roll over your 401(k) into an Individual Retirement Account (IRA), offering potentially more control and a wider range of investments. If you secure a new job with a 401(k) plan, you might roll over your old 401(k) into your new employer's plan. Lastly, cashing out is an option, though usually not recommended due to tax penalties and their impact on your long-term savings. It's important to understand each option's implications, consult a financial advisor if necessary, and make an informed decision to ensure your retirement savings remain on track. There are a few paths you can take when managing your 401(k) after your company closes. In some cases, you can leave your money in the old 401(k) plan, especially if it has solid, low-cost investment options. It's important to note that this might not always be possible, depending on the specifics of your plan and the circumstances of your company's closure. Moving your 401(k) funds to an IRA can be a good option. IRAs often offer more flexibility and investment options than 401(k) plans, and this can be a suitable strategy if you don't immediately have a new employer's plan to move to. If you have found new employment and your new employer offers a 401(k) plan, you can consider rolling your old 401(k) into this new plan. However, this depends on the quality of the new plan and whether it accepts rollovers. While it's generally not recommended due to tax implications and potential penalties, in some scenarios, cashing out your 401(k) might be considered. It's important to understand the ramifications fully before opting for this route. There are several potential benefits to consider when thinking about rolling your old 401(k) into your new employer's plan. One key advantage is simplicity. By consolidating your retirement savings into a single account, you'll have fewer balances and statements to monitor. This can make it easier to manage your overall retirement strategy. Rolling over to a new 401(k) allows for the continuity of tax-deferred growth of your retirement savings, ensuring that you keep the momentum without losing out on potential gains. 401(k) plans often offer loan options that IRAs do not. If you anticipate needing to borrow against your retirement savings, this could be an advantage. While there are benefits, there are also some potential downsides to rolling over into a new 401(k). Unlike an Individual Retirement Account, 401(k) plans often have a more limited selection of investment options. If your new employer's plan doesn't offer the investment choices you prefer, this could be a significant disadvantage. Some 401(k) plans have high administrative and investment fees. If your new employer's 401(k) has higher fees than an IRA or your old 401(k), it could erode your retirement savings over time. Having your retirement funds tied to your employer brings an element of risk. If the company goes under, it could be a hassle to reclaim your funds or roll them over to a different plan. Cashing out your 401(k) before retirement age can lead to immediate financial consequences. If you're under the age of 59 ½, in addition to income tax, you could face a 10% early withdrawal penalty. Some exceptions apply, such as in the case of certain hardships, but in most cases, this penalty will apply. Cashing out your 401(k) early can also have long-term effects on your financial security. When you withdraw funds from your 401(k), you're not just losing the amount withdrawn. You're also losing potential earnings those funds could have generated if they were left invested. Over time, this could amount to a significant sum due to the power of compound interest. The primary purpose of a 401(k) is to provide income during retirement. By cashing out early, you reduce the funds available to you in your retirement years. This could mean having to work longer or adjust your lifestyle in retirement. While cashing out a 401(k) early is generally discouraged, there are situations where it might be the least bad option. If you're facing severe financial hardship, such as significant medical expenses or potential foreclosure, you may consider cashing out your 401(k). Cashing out should only be considered once all other options have been exhausted. This includes emergency savings, other less penalized assets, or even loans. The Employee Retirement Income Security Act (ERISA) provides protections for your 401(k). ERISA is a federal law that sets minimum standards for retirement plans, including 401(k)s, offered by private-sector employers. ERISA requires plans to provide participants with plan information, including important details about plan features and funding. It also establishes fiduciary responsibilities for those managing and controlling plan assets. If you believe your ERISA rights have been violated, such as if your 401(k) funds have been mishandled, you can file a claim with the U.S. Department of Labor's Employee Benefits Security Administration. It's essential to have all your plans and personal information at hand when making a claim. Navigating the management of your 401(k) after a company's closure can be complex, but understanding your options can lead to sound decisions. You could leave the funds in your old 401(k), roll them over into an IRA, a new employer's 401(k), or cash out. However, each of these options has its pros and cons. For instance, rolling over into a new employer's 401(k) simplifies management but might have limited investment choices. Conversely, cashing out can have substantial tax implications and erode your future retirement savings. Lastly, the protections under ERISA ensure your rights, allowing you to file claims if violated. Understanding these key aspects will enable you to manage your 401(k) or IRA effectively, ensuring your financial stability in the future.How to Manage a 401(k) If Your Company Closes Overview

Evaluate Your Options

Leave Money in the Old 401(k)

Roll Over Into an IRA

Roll Over Into a New Employer's 401(k) Plan

Cash Out Your 401(k)

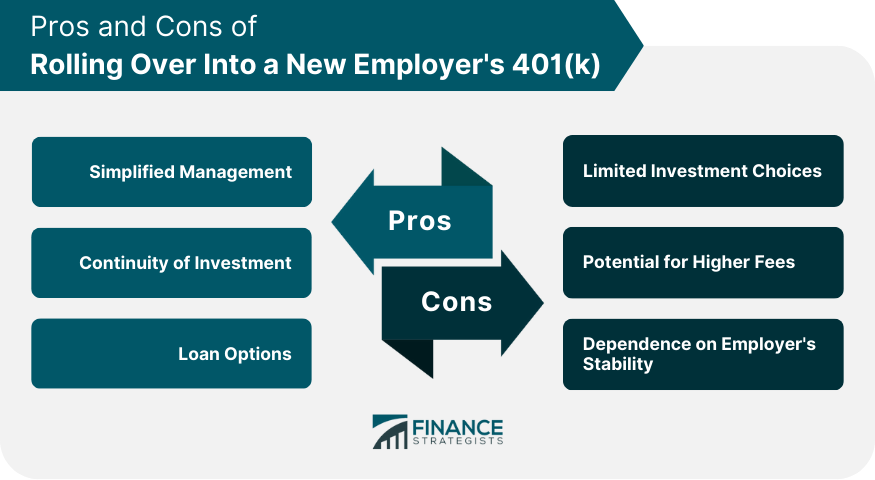

Pros of Rolling Over Into a New Employer's 401(k)

Simplified Management

Continuity of Investment

Loan Options

Cons of Rolling Over Into a New Employer's 401(k)

Limited Investment Choices

Potential for Higher Fees

Dependence on Employer's Stability

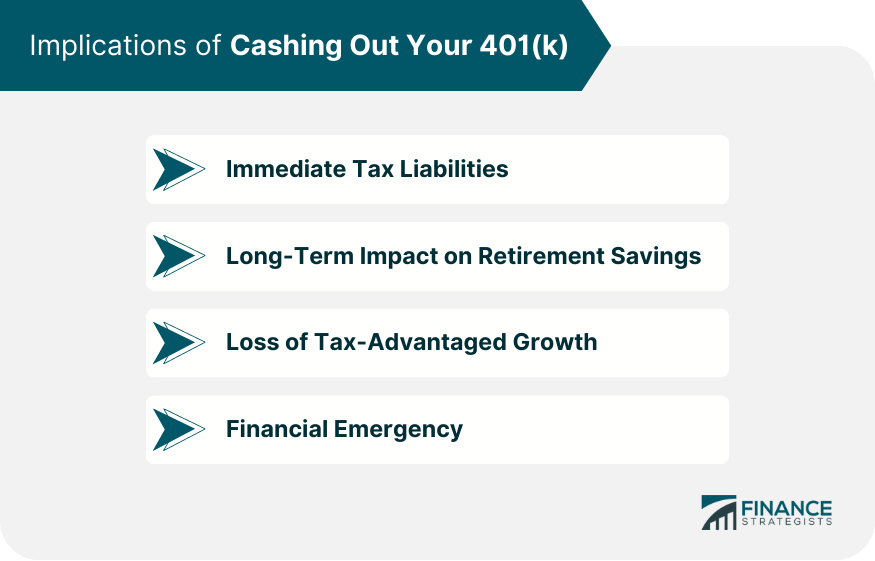

Implications of Cashing Out Your 401(k)

Immediate Tax Implications and Potential Penalties

Early Withdrawal Penalties

Long-Term Impact on Retirement Savings

Lost Growth Potential

Reduced Retirement Income

Scenarios Where Cashing Out May Be Considered

Financial Hardship

Exhaustion of Other Options

Legal Rights and Protections for Your 401(k) if Your Company Closes

Explanation of the Employee Retirement Income Security Act (ERISA)

How to File a Claim if Your Rights Have Been Violated

Conclusion

How to Manage a 401(k) If Your Company Closes FAQs

When your company closes, your 401(k) doesn't disappear. You still own these funds. However, the management of the account may change, and it may be up to you to decide what happens next. You typically have four options: leave the money in the old plan (if allowed), roll over the funds into an IRA, roll over the money into a new employer's 401(k), or cash out the funds.

If you're unemployed after your company closes, you can consider leaving the money in the old 401(k) if allowed, or rolling it over into an IRA. It's generally not recommended to cash out your 401(k) due to the tax implications and potential penalties, but it might be considered in some emergency situations.

Yes, you can roll over your 401(k) into an IRA if your company closes. This often gives you more control over your investments and may provide more options compared to a 401(k). However, you should also consider potential differences in rules around withdrawals and loans when making your decision.

If you cash out your 401(k) when your company closes, you'll likely owe income tax on the distribution. If you're under 59 1/2, you could also face an early withdrawal penalty of 10%. Before deciding to cash out, it's essential to fully understand these implications and consider other options.

Your 401(k) is protected by the Employee Retirement Income Security Act (ERISA), which sets minimum standards for most voluntarily established retirement plans in private industry to provide protection for individuals in these plans. If you believe your rights under ERISA have been violated, such as if your funds have been mishandled, you can file a claim with the U.S. Department of Labor's Employee Benefits Security Administration.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.