The 401(k) plan, primarily sponsored by employers, allows employees to save and invest a piece of their paycheck before taxes are taken out. When withdrawals begin, typically in retirement, these amounts are taxed. On the other hand, Roth IRAs are individual retirement accounts where contributions are made with post-tax dollars, but the withdrawals, including gains, are generally tax-free in retirement. Roth IRAs offer a refreshing twist. Instead of getting the tax break when you put the money in as you do with 401(k)s, Roth IRAs provide the benefit when the money is taken out. This shift in tax advantage is what makes them enticing, especially for those who anticipate being in a higher tax bracket in their golden years. Both 401(k)s and Roth IRAs offer tax breaks, either upfront or down the line, that can significantly amplify your savings growth over time. Peel back the layers of 401(k) plans and you'll find a subset: the after-tax 401(k). Unlike the traditional pre-tax 401(k) where contributions reduce taxable income, after-tax 401(k)s don't provide that immediate tax benefit. Instead, they behave somewhat like Roth IRAs, though with a twist. The contributions are post-tax, but the earnings on those contributions are subject to tax upon withdrawal. However, there's a silver lining. Those after-tax contributions can be rolled over into a Roth IRA, where all future earnings can grow and be withdrawn tax-free. The magic lies in converting those after-tax dollars and their potential taxable earnings into completely tax-free growth. So, why would anyone consider rolling their after-tax 401(k) contributions to a Roth IRA? First and foremost, the power of tax-free withdrawals is tantalizing. By doing this rollover, not only do the contributions continue to grow tax-free, but so do their earnings, something not guaranteed in an after-tax 401(k). Additionally, Roth IRAs come with more flexible withdrawal rules. Unlike 401(k)s, which mandate withdrawals at a certain age, Roth IRAs have no such requirement. This can be a boon for individuals aiming for specific estate planning goals or simply wishing to pass on assets to heirs tax-free. Timing is key in the financial world, and this rollover process is no exception. One needs to consider market conditions, personal financial circumstances, and anticipated tax changes. For instance, in a bear market, assets might be undervalued, which could be an advantageous time for a rollover. This means less taxable income is generated during the conversion. Conversely, if tax rates are set to rise in the near future, initiating a rollover sooner rather than later might be beneficial. This is because the rollover itself can be a taxable event, depending on the specific circumstances and proportion of pre-tax versus post-tax amounts in the 401(k). Before embarking on any financial endeavor, it's crucial to understand your starting point. Obtain a clear picture of your 401(k) account, detailing your total balance, pre-tax contributions, any employer match, and, most importantly, your after-tax contributions. Knowing these details helps ensure you only roll over the appropriate amounts and avoid unnecessary tax consequences. Further, most providers will offer an account statement or summary that delineates these figures. Sometimes, it might be a separate category or even a different account altogether. Regardless, clarity here is paramount. An error in this initial step can ripple through the entire process, causing confusion and potential tax snafus. Once you have a clear snapshot of your 401(k), the next move is toward the Roth IRA. If you don’t have a Roth IRA already, it's time to shop around. Numerous financial institutions offer them, so it's about finding one that aligns with your needs. Factors to consider include fees, investment options, and customer service. If you already have a Roth IRA, reach out to the provider and inquire about their rollover process. Some might have specific forms or procedures. Additionally, ensure that your Roth IRA accepts rollovers from after-tax 401(k) accounts. While most do, it’s always best to confirm beforehand. With a Roth IRA in place and ready, it's time to trigger the rollover. Contact your 401(k) provider and explicitly express your desire to roll over your after-tax contributions to a Roth IRA. Here, precision is vital. The goal is to ensure that only the after-tax portion is moved to the Roth IRA. Each provider might have a distinct process, so follow their instructions meticulously. Often, they will issue a check (payable to the Roth IRA provider for your benefit) or facilitate a direct transfer. After initiating the rollover, your role is far from over. Stay engaged and monitor the transition. Track the funds as they move from your 401(k) to the Roth IRA. Given the importance of this process, it's worth the extra effort to ensure everything goes smoothly. Remember, financial institutions process multitudes of transactions daily. Errors, while uncommon, can happen. By actively monitoring the transfer, you can spot and address any discrepancies immediately. This proactive approach can save you a lot of potential headache in the future. The rollover, once complete, still has a final step: addressing it on your tax return. It’s vital to accurately report the rollover to the IRS. Specifically, you'll need to document the amount that was converted, especially if there were any earnings on your after-tax contributions. The IRS provides Form 8606 to help you navigate this. This form tracks non-deductible contributions to traditional IRAs and distributions from Roth accounts. If you've only rolled over the after-tax portion, there should be no tax due. However, if any earnings or pre-tax amounts were inadvertently included, you may owe tax on those amounts. When transitioning funds from an after-tax 401(k) to a Roth IRA, the goal is to shift the after-tax contributions. These have already been taxed, so moving them to the Roth IRA should not incur additional taxes. However, any earnings on those after-tax contributions in the 401(k) are a different story. If you roll over these earnings, they are taxable. It’s a fine balance. If done correctly, the tax hit can be minimal or even non-existent. But if mistakes creep in, the tax consequences can be substantial. It's always recommended to consult with a tax professional to understand and navigate these waters with confidence. The IRS operates under the "pro-rata" rule when it comes to distributions from 401(k) plans that have both pre-tax and after-tax contributions. This rule stipulates that any distribution from such a 401(k) is deemed to be composed of both pre-tax and post-tax money in the same proportion as found in the account. This can complicate rollovers. For example, if 20% of your 401(k) consists of after-tax contributions, and you decide to roll over some funds to a Roth IRA, the IRS views 20% of that rollover amount as after-tax money and the remaining 80% as pre-tax money. It's this 80% that could lead to unexpected tax consequences. Despite the immediate tax considerations, the long-term benefits of converting to a Roth IRA can be remarkable. Imagine a scenario where your Roth IRA grows substantially over decades. When retirement arrives, all those gains, in addition to your original after-tax contribution, can be withdrawn tax-free. Additionally, the Roth IRA structure may shield you from potential future tax rate hikes. If tax rates climb in the coming decades, having a pool of tax-free money to draw from can be a significant advantage. You're essentially locking in today's rates on the growth of your investment. The magic of the Roth IRA lies in its growth potential coupled with tax-free withdrawals. Unlike traditional retirement accounts, where taxes are deferred until withdrawal, Roth IRAs flip the script. You pay taxes upfront, but in exchange, the account grows tax-free. By the time retirement rolls around, both the contributions and the earnings can be accessed without any tax liability. This structure offers peace of mind. Withdrawing from retirement savings without worrying about tax calculations or unexpected bills offers a simplicity many retirees cherish. Another feather in the Roth IRA's cap is the absence of Required Minimum Distributions (RMDs). Traditional retirement accounts, like 401(k)s or traditional IRAs, come with this pesky requirement. Once you reach a certain age (currently 72), you're mandated to start withdrawing a specific minimum amount annually, regardless of whether you need the money. Roth IRAs have no such constraint. If you don’t need the money, you can let it continue to grow, tax-free. This makes it an excellent tool for estate planning, allowing individuals greater control over their wealth distribution. Speaking of estate planning, Roth IRAs offer unparalleled flexibility for heirs. Should you pass away with funds still in your Roth IRA, these can be passed on to beneficiaries. These beneficiaries can stretch out the tax-free withdrawals over their lifetimes, benefiting from prolonged tax-free growth. Contrast this with inheriting a traditional IRA or 401(k). The latter often comes with tax bills for the beneficiaries. Roth IRAs remove this complication, ensuring the legacy left behind is as beneficial as possible. Consolidation can be a guiding principle as one inches closer to retirement. Managing multiple accounts can become tedious. By rolling over after-tax 401(k) funds to a Roth IRA, you're reducing the number of accounts to monitor. A singular, consolidated view of retirement assets can make planning easier. It's about streamlining, reducing administrative burden, and having a clearer picture of your financial health. With fewer accounts, it becomes simpler to strategize withdrawals, manage investments, and maintain an optimal asset allocation. Financial transactions often come with costs. When considering a rollover, it's essential to be aware of any fees or penalties that might apply. Some 401(k) providers might charge a fee for the rollover process. On the Roth IRA side, there might be account opening or maintenance fees. These costs, while they might seem trivial in the short term, can add up, especially when considering the lost potential growth on those amounts over time. Before initiating a rollover, understand the full scope of associated charges. Comparing different providers can sometimes result in significant savings. Every financial move has ripple effects. Rolling over after-tax 401(k) funds to a Roth IRA is no exception. Such a move could impact other retirement strategies in play. For instance, if you're aiming for specific income thresholds to qualify for tax breaks or medical subsidies, a rollover might push you beyond those limits. Additionally, large rollovers could bump you into a higher tax bracket, even if temporarily. Understanding these interplays is vital before making a decision. With multiple retirement accounts in play, there's a risk of over-contributing. The IRS sets clear contribution limits for retirement accounts. Surpassing these can result in penalties. When rolling over funds, ensure that you're not inadvertently exceeding these limits. It might seem straightforward, but with multiple transactions, especially if you're also making regular contributions, it's an area where errors can creep in. One compelling reason many individuals hesitate to roll over funds is the potential loss of employer matches. Some companies offer match contributions to employee 401(k)s. If your 401(k) still has an active match and you initiate a rollover, you might forgo future matches. Before making a move, understand the terms of your employer's match. Sometimes, the benefit of continued employer contributions might outweigh the advantages of a Roth IRA rollover. One of the foundational decisions in retirement planning revolves around tax brackets. If you anticipate being in a higher tax bracket in retirement, a Roth IRA, with its tax-free withdrawals, becomes more appealing. Conversely, if you expect to be in a lower bracket during retirement, the immediate tax hit of a rollover might not be as beneficial. Projecting your future tax situation, while challenging, is crucial in this decision-making process. Your income trajectory can also influence the rollover decision. If you're early in your career and anticipate significant income growth, your future self might land in higher tax brackets. In such scenarios, the Roth IRA's tax-free withdrawals become increasingly valuable. However, if you're nearing retirement and expect a drop in income, the immediate tax implications of a rollover might outweigh the potential future benefits. The horizon matters. If retirement is decades away, the compounded, tax-free growth in a Roth IRA has ample time to work its magic. But if retirement is imminent, there might not be enough growth potential to offset the immediate tax hit from the rollover. Your retirement goals also play a part. If you aim for early retirement, the flexibility and tax advantages of a Roth IRA might be more beneficial. But if you're looking to work well into your 70s, other factors might take precedence. Liquidity is the ease with which an asset can be quickly converted into cash. In retirement, unexpected expenses can pop up, be it medical emergencies, home repairs, or even unique travel opportunities. Having quick access to funds without tax implications can be invaluable. Roth IRAs, with their tax-free withdrawals, offer superior liquidity compared to traditional retirement accounts. If you foresee a need for increased liquidity in retirement, the Roth IRA becomes a compelling choice. Sometimes, the best move is to do nothing. Leaving funds in a 401(k), especially if it has low fees and excellent investment choices, can be a viable strategy. You maintain the tax-deferred growth and might still benefit from employer matches or other perks. However, 401(k)s come with RMDs and lack the flexibility of Roth IRAs. It's a trade-off. Understand the pros and cons, and align them with your personal retirement goals. Another option is to sidestep the Roth IRA and roll over to a traditional IRA. This move retains the tax-deferred nature of your savings, potentially avoiding immediate tax consequences. Traditional IRAs also offer broader investment choices compared to many employer-sponsored 401(k)s. Yet, they come with their own set of challenges, including RMDs and potential tax bills upon withdrawal. While it's generally not recommended, some might consider withdrawing funds, paying the penalties and taxes, and then investing elsewhere. This strategy might make sense in specific scenarios, especially if the 401(k) has high fees or poor investment choices. However, the immediate tax hit and potential penalties can significantly erode the principal. It's a risky move and should be approached with caution and ideally, under the guidance of a financial advisor. After-tax 401(k) contributions present an opportunity to roll over into Roth IRAs, unlocking the potential for tax-free growth and withdrawals in retirement. Unlike 401(k)s, which offer tax benefits upfront, Roth IRAs give tax advantages upon withdrawal. This is particularly appealing for those foreseeing a higher tax bracket in retirement. The after-tax 401(k) contributions differ from traditional 401(k)s, as they lack immediate tax benefits but can be transferred to a Roth IRA to enjoy tax-free growth. This conversion combines the lure of tax-free withdrawals and flexibility, especially for estate planning. Timing, however, is crucial, considering market conditions and anticipated tax changes. Although the process involves steps from reviewing account details to reporting on tax returns, the potential long-term tax benefits are substantial. However, careful consideration of one's current and expected tax brackets, future income, retirement goals, and need for liquidity is essential before deciding on the rollover.Overview 401(k)s and Roth IRAs

Understanding the After-Tax 401(k) Rollover to Roth IRA Process

What Is an After-Tax 401(k)?

Rationale for Rolling Over to a Roth IRA

Timing Considerations

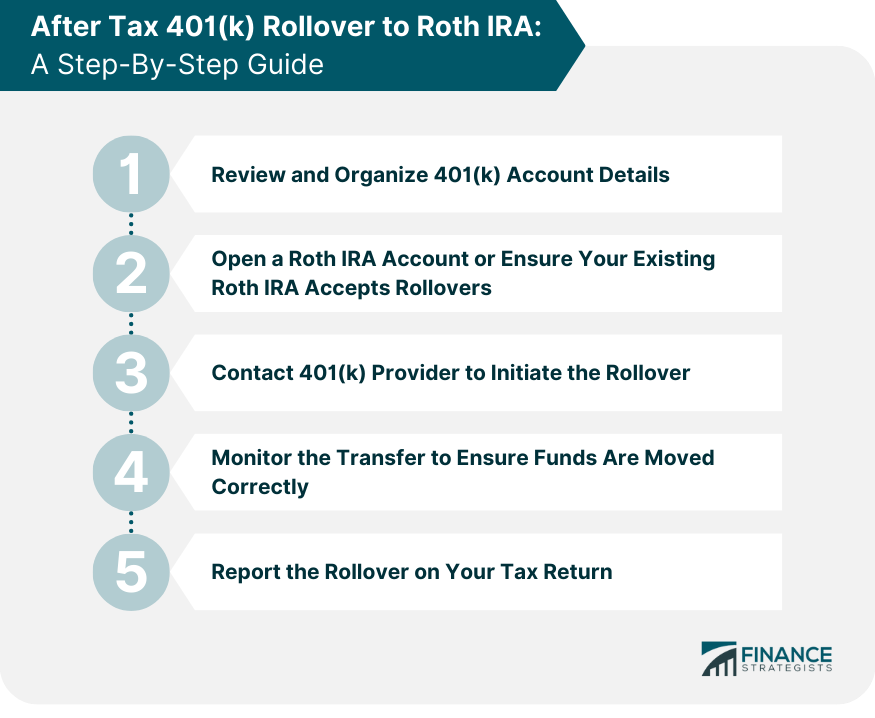

After Tax 401(k) Rollover to Roth IRA: A Step-By-Step Guide

Step 1: Review and Organize 401(k) Account Details

Step 2: Open a Roth IRA Account or Ensure Your Existing Roth IRA Accepts Rollovers

Step 3: Contact 401(k) Provider to Initiate the Rollover

Step 4: Monitor the Transfer to Ensure Funds Are Moved Correctly

Step 5: Report the Rollover on Your Tax Return

Tax Implications and Considerations After Tax 401(k) to Roth IRA Rollover

Immediate Tax Consequences

"Pro-Rata" Rule and Its Implications

Potential Long-Term Tax Benefits

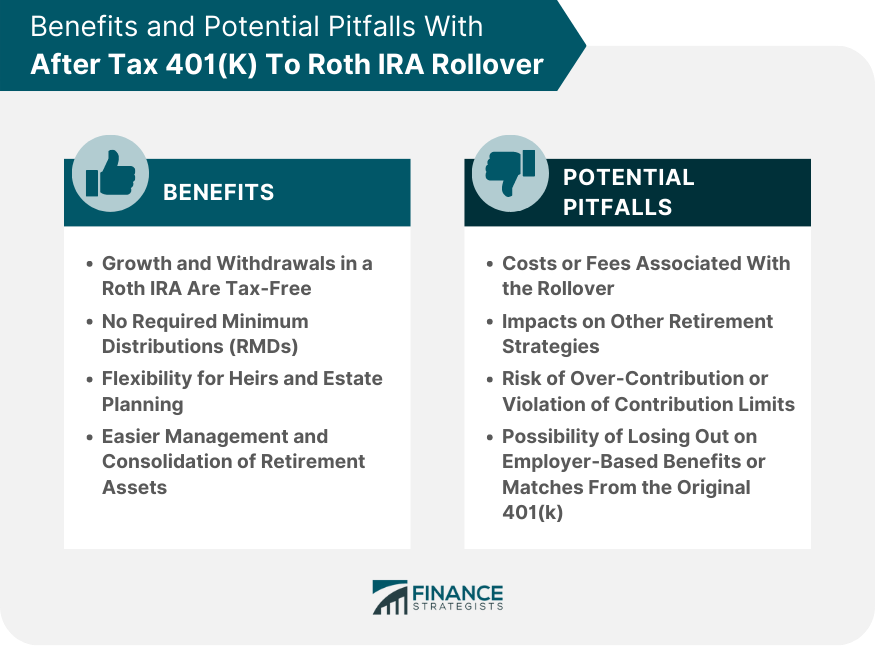

Benefits of Completing the After Tax 401(k) to Roth IRA Rollover

Growth and Withdrawals in a Roth IRA

No Required Minimum Distributions (RMDs)

Flexibility for Heirs and Estate Planning

Easier Management and Consolidation of Retirement Assets

Potential Pitfalls and Concerns With After Tax 401(k) to Roth IRA Rollover

Costs or Fees Associated With the Rollover

Impacts on Other Retirement Strategies

Risk of Over-Contribution or Violation of Contribution Limits

Possibility of Losing Out on Employer-Based Benefits or Matches From the Original 401(k)

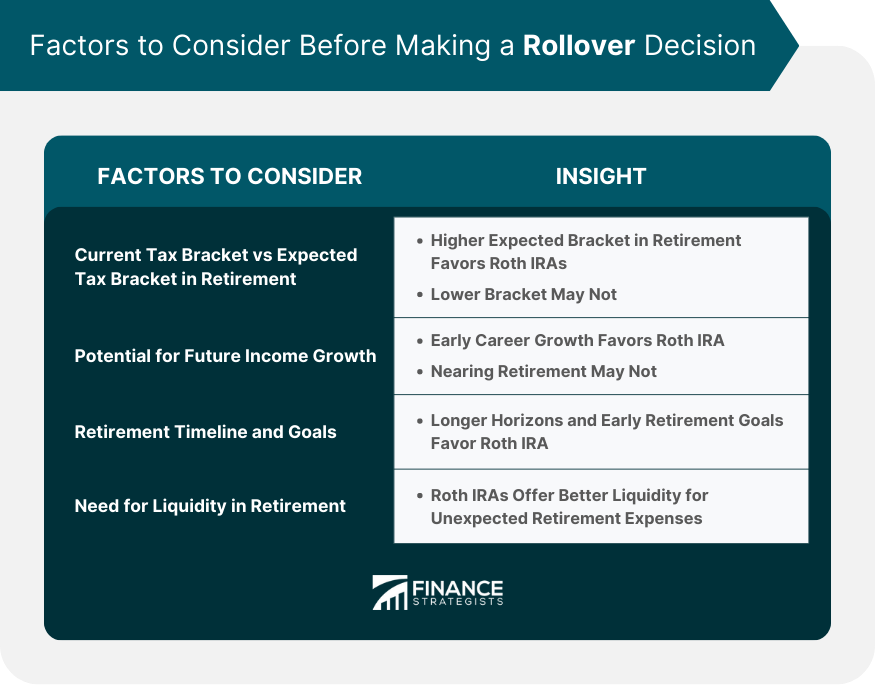

Factors to Consider Before Making a Rollover Decision

Current Tax Bracket vs Expected Tax Bracket in Retirement

Potential for Future Income Growth

Retirement Timeline and Goals

Need for Liquidity in Retirement

Comparing Alternatives to Rollovers

Leaving Funds in the 401(k)

Rolling Over to a Traditional IRA

Withdrawing and Facing Penalties

Bottom Line

After Tax 401(k) Rollover to Roth IRA FAQs

When you roll over after-tax 401(k) funds, you typically don't owe taxes on the after-tax contributions. However, earnings on those contributions may be taxable.

Roth IRAs allow tax-free withdrawals in retirement, provide more flexibility in terms of no RMDs, and can offer heirs tax-free distributions.

The "pro-rata" rule means that any distribution from a 401(k) with both pre-tax and after-tax funds is seen as a mix of both, potentially leading to tax implications.

Yes, some 401(k) providers might charge rollover fees, and Roth IRAs may have account opening or maintenance fees. It's crucial to understand these costs upfront.

It can be, especially if the 401(k) offers low fees, good investment choices, or continued employer matches. However, Roth IRAs provide more flexibility in withdrawals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.