The division of retirement assets is an essential aspect of financial planning, particularly during major life events such as divorce or separation. Understanding the process and implications of dividing retirement assets is critical for ensuring equitable distribution and protecting one's financial future. Navigating the division of retirement assets can be complex, and understanding the various factors affecting the process is crucial to ensuring a fair and accurate distribution of assets while minimizing tax liabilities and other potential complications. Marital status plays a significant role in determining the division of retirement assets. In cases of divorce or separation, retirement assets accumulated during the marriage are often considered marital property and subject to division. Premarital and postnuptial agreements can affect the division of retirement assets by specifying how these assets will be divided in the event of divorce or separation. The division of retirement assets is also influenced by state laws governing marital property. Some states follow community property laws, while others adhere to equitable distribution principles, which can result in different approaches to dividing retirement assets. Defined benefit plans, such as traditional pensions, provide a specific monthly benefit at retirement and can be subject to division during divorce or separation. Defined contribution plans, such as 401(k)s and 403(b)s, are retirement accounts funded by employee and employer contributions. These accounts can also be divided during divorce or separation. IRAs, including traditional and Roth IRAs, are personal retirement accounts funded by individual contributions and can be subject to division in divorce or separation proceedings. Annuities are financial products designed to provide a stream of income during retirement and can also be divided during divorce or separation. Stock options and deferred compensation plans, such as employee stock purchase plans (ESPPs) and non-qualified deferred compensation (NQDC) plans, may also be subject to division during divorce or separation. The immediate offset method involves calculating the present value of retirement assets and offsetting that value against other marital assets, resulting in a one-time division of assets. Deferred division involves waiting until the retirement assets are paid out to divide them, with each spouse receiving a share of the benefits as they are distributed. A Qualified Domestic Relations Order (QDRO) is a court order used to divide specific types of retirement assets, such as 401(k)s and pensions, during divorce or separation. The QDRO directs the retirement plan administrator to distribute a portion of the account to an alternate payee, typically the non-employee spouse. If retirement assets are divided using a qualified domestic relations order (QDRO), the recipient spouse will typically receive a portion of the assets as a taxable distribution. The recipient spouse will owe ordinary income tax on the distribution, but will not be subject to the 10% early withdrawal penalty if they are under age 59 ½. Alternatively, if the retirement assets are divided through a tax-free transfer, such as a trustee-to-trustee transfer or direct rollover, the recipient spouse will not owe tax on the distribution at the time of the transfer. If a non-working spouse is awarded a portion of a working spouse's IRA, they may be able to contribute the assets to a spousal IRA. This allows them to maintain the tax-deferred status of the assets and potentially defer taxes until withdrawal in retirement. The cost basis of retirement assets can impact the tax implications of dividing these assets. For example, if the cost basis of a 401(k) is lower than the current value, the recipient spouse may owe more in taxes when they withdraw the assets in retirement. The tax implications of dividing retirement assets may differ depending on whether the assets are held in a qualified plan, such as a 401(k), or an IRA. It is important to consult with a financial advisor or tax professional to understand the specific tax implications of dividing retirement assets in your individual situation. Prenuptial and postnuptial agreements can be used to protect retirement assets by specifying how these assets will be divided in the event of divorce or separation. These agreements can provide clarity and security for both parties involved. Maintaining separate and marital assets separately and clearly documenting asset transfers can help protect retirement assets during the division process. Properly documenting asset transfers, such as rollovers and account divisions, can help protect retirement assets and ensure that both parties are in compliance with tax laws and regulations. Working with financial advisors can help individuals navigate the complex process of dividing retirement assets and ensure that their financial interests are protected during the division process. Divorce attorneys can provide valuable legal guidance and representation during the division of retirement assets, ensuring that the process is equitable and in accordance with applicable laws and regulations. Tax professionals can provide advice and guidance on the tax implications of dividing retirement assets, helping individuals minimize tax liabilities and avoid potential penalties. Dividing retirement assets is a complex and critical aspect of financial planning during major life events such as divorce or separation. Understanding the factors affecting the division of these assets, the types of retirement assets subject to division, and the various methods and tax implications of dividing these assets is essential to ensuring an equitable distribution and protecting one's financial future. By seeking professional guidance from financial advisors, divorce attorneys, and tax professionals, individuals can navigate this complex process with confidence and secure their financial well-being during these challenging times.Division of Retirement Assets: Overview

Factors Affecting the Division of Retirement Assets

Marital Status and Divorce

Premarital and Postnuptial Agreements

State Laws Governing Marital Property

Types of Retirement Assets Subject to Division

Defined Benefit Plans

Defined Contribution Plans

Individual Retirement Accounts (IRAs)

Annuities

Stock Options and Deferred Compensation

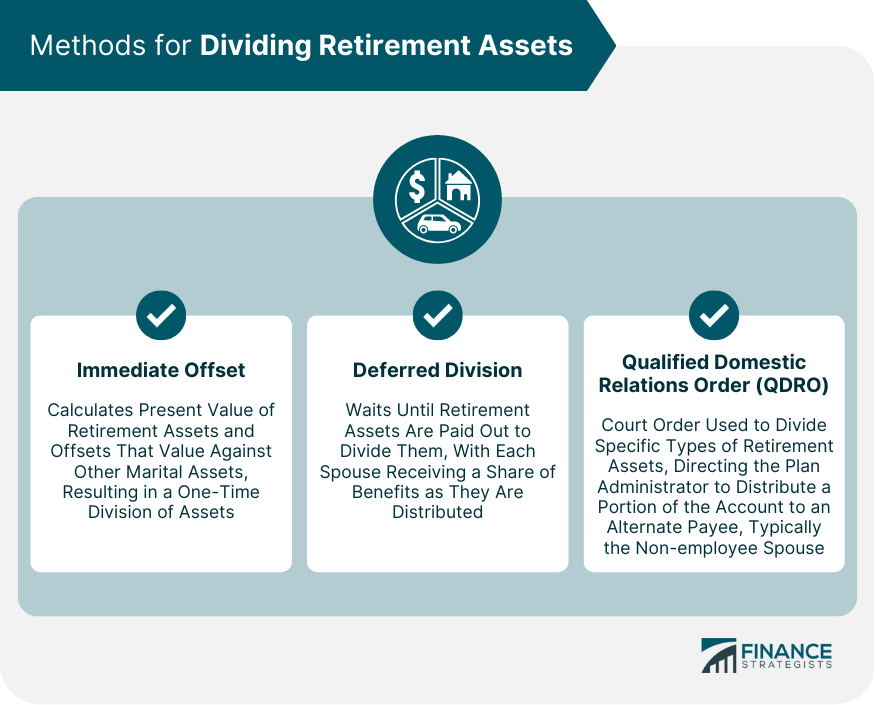

Methods for Dividing Retirement Assets

Immediate Offset

Deferred Division

Qualified Domestic Relations Order (QDRO)

Tax Implications of Dividing Retirement Assets

Taxable Distribution

Tax-Free Transfer

Spousal IRA

Cost Basis

Qualified Plan vs IRA

Strategies for Protecting Retirement Assets

Prenuptial and Postnuptial Agreements

Keeping Separate and Marital Assets Distinct

Carefully Documenting Asset Transfers

Seeking Professional Guidance

Importance of Working With Financial Advisors

Consulting With Divorce Attorneys

Collaborating With Tax Professionals

Conclusion

Division of Retirement Assets FAQs

Division of retirement assets refers to the process of dividing retirement savings or benefits between two parties as part of a divorce settlement.

The tax implications of the division of retirement assets in a divorce can vary depending on the specific type of asset and how it is divided. It is important to consult with a tax professional to understand the tax consequences of dividing retirement assets in a divorce.

Retirement assets that can be divided include pension plans, 401(k)s, IRAs, and other types of retirement accounts.

The division of retirement assets is typically handled through a court order or agreement between the parties involved. The amount of retirement benefits each party receives is usually determined by factors such as the length of the marriage and the contributions made by each party to the retirement accounts.

Yes, retirement assets can be divided between parties without penalty if the proper procedures are followed. Specifically, a Qualified Domestic Relations Order (QDRO) may be necessary to divide certain types of retirement accounts without triggering taxes or penalties.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.