In the realm of retirement planning, IRAs stand as pivotal instruments, offering a blend of flexibility, tax advantages, and investment growth potential. Navigating through the myriad of options, from traditional IRAs to their more nuanced cousins, Roth, and SIMPLE IRAs, is crucial for crafting a retirement strategy that aligns with individual financial goals and circumstances. Understanding the various IRA types is more than a mere exercise in financial literacy; it's a cornerstone of sound retirement planning. With each type governed by distinct rules and benefits, a clear comprehension can unlock pathways to optimized savings and tax strategies, ensuring a more secure and comfortable retirement. Roth IRAs emerge as a unique choice in the retirement savings landscape, primarily due to their distinct tax treatment. Unlike traditional IRAs, where contributions may be tax-deductible, Roth IRAs feature after-tax contributions. This means that while there's no immediate tax benefit, the trade-off comes in the form of tax-free growth and withdrawals, a compelling advantage, especially for those anticipating higher tax brackets in the future. The Roth IRA is not just an account; it's a long-term strategy. Its design caters to those who envision their retirement years in a higher tax bracket than their current one. It's a commitment to pay taxes now and reap the benefits of tax-free withdrawals later, a feature that sets it apart in the retirement planning toolkit. Roth IRAs come with specific eligibility criteria, primarily based on income levels. These criteria are periodically adjusted, making it essential for potential contributors to stay informed. For individuals and married couples, the ability to contribute to a Roth IRA reduces and eventually phases out as income rises. This phase-out range varies based on tax filing status, making it crucial for investors to consult the latest guidelines or a financial advisor to determine their eligibility. Navigating the Roth IRA eligibility maze requires a keen eye on income thresholds. These thresholds are not static; they evolve, reflecting economic changes and inflation adjustments. For those hovering near the upper limits, planning contributions can become a delicate balance, sometimes necessitating strategic income adjustments or alternate retirement savings routes. The contribution limits for Roth IRAs are another vital aspect to consider. These limits are subject to annual adjustments, reflecting changes in the economy and cost of living. For most investors, the limits provide ample room for significant retirement savings, but for those who are particularly investment-savvy or high earners, these caps might necessitate supplementary retirement strategies. It's also noteworthy that individuals aged 50 and over can make additional "catch-up" contributions, offering a valuable opportunity to bolster their retirement savings as they near retirement age. For 2026, the Roth IRA contribution limit is set at $7,500 for those under 50, and an additional $1,100 catch-up contribution for those 50 and older. Understanding and adhering to these limits is crucial. Exceeding them can lead to tax complications and penalties, underscoring the importance of meticulous planning and tracking of contributions. For those navigating the complexities of retirement savings, staying informed about these limits and strategically planning contributions can make a significant difference in the long-term growth of their retirement funds. The tax treatment of Roth IRA contributions and withdrawals is a defining feature that sets it apart from other retirement savings options. Since contributions are made with after-tax dollars, they do not reduce your taxable income in the year of contribution. However, the real benefit of a Roth IRA unfolds over time - as investments grow, that growth is tax-free, and so are qualified withdrawals during retirement. This tax-free growth and withdrawal aspect of Roth IRAs can be particularly advantageous for those who expect to be in a higher tax bracket in retirement. It offers a form of tax diversification, allowing retirees to manage their taxable income in retirement more effectively. However, it's essential to comply with the rules regarding withdrawal timelines to avoid penalties and ensure the tax benefits are fully realized. Choosing a Roth IRA can offer several benefits, particularly for certain demographics and financial situations. For younger investors, who are typically in a lower tax bracket, paying taxes upfront at a lower rate can yield significant long-term benefits. Moreover, Roth IRAs do not have Required Minimum Distributions (RMDs) during the account owner's lifetime, offering more flexibility in retirement planning and for legacy planning purposes. Another benefit lies in the Roth IRA’s flexibility regarding withdrawals. Contributions (but not earnings) can be withdrawn tax and penalty-free at any time, offering a safety net in case of financial emergencies. This flexibility, combined with the tax-free growth potential, makes Roth IRAs a powerful tool in a diverse retirement strategy. SIMPLE IRAs (Savings Incentive Match Plan for Employees) are designed specifically for small businesses and self-employed individuals. They offer a simpler and less costly retirement plan option compared to 401(k)s. The SIMPLE IRA allows both employees and employers to contribute, with the employer either matching employee contributions or making non-elective contributions on behalf of all eligible employees. This type of IRA is particularly attractive for small businesses seeking a straightforward, cost-effective way to offer retirement benefits. The simplicity of the plan's administration is a key feature, making it a popular choice for businesses with fewer resources to manage more complex retirement plans. The eligibility criteria for SIMPLE IRAs are straightforward, primarily focusing on the employer aspect. Employers who choose to offer a SIMPLE IRA must have 100 or fewer employees who received at least $5,000 in compensation in the previous year. There is no requirement for employers to file annual financial reports, which is often a significant administrative burden with other retirement plans. For employees, eligibility to contribute to a SIMPLE IRA typically requires earning a minimum amount in the previous two years and expecting to earn at least that amount in the current year. This inclusivity allows a broader range of employees to participate, making it a beneficial tool for both employee retention and retirement savings. The contribution limits for SIMPLE IRAs are notably different from those of Roth IRAs. These limits are higher than traditional and Roth IRAs, reflecting the plan's aim to facilitate more robust retirement savings for small business employees. Additionally, similar to Roth IRAs, there is a provision for catch-up contributions for individuals aged 50 and over, allowing older employees an opportunity to accelerate their retirement savings as they approach retirement age. The amount an employee contributes from their salary to a SIMPLE IRA cannot exceed $17,000 in 2026 ($16,500 in 2025). If permitted by the SIMPLE IRA plan, participants who are age 50 or over at the end of the calendar year can also make catch-up contributions. The catch-up contribution limit for SIMPLE IRA plans is $4,00 for 2026. For small business owners and employees alike, understanding and maximizing these contribution limits can significantly impact retirement preparedness. Unlike Roth IRAs, the SIMPLE IRA contributions are pre-tax, reducing taxable income in the contribution year, which can be a decisive factor for many when choosing between different retirement savings options. The tax treatment of SIMPLE IRA contributions and withdrawals is straightforward yet distinct from Roth IRAs. Contributions to a SIMPLE IRA are made pre-tax, thereby reducing the taxable income for the year of contribution. Upon withdrawal during retirement, the distributions are taxed as ordinary income. This setup is particularly advantageous for employees who anticipate being in a lower tax bracket during retirement. However, it's crucial to note that early withdrawals, especially within the first two years of participation, can attract significant penalties. This stringent penalty structure underscores the importance of considering a SIMPLE IRA as a long-term commitment, aligning with the primary goal of ensuring a secure and stable financial foundation in retirement. When comparing SIMPLE IRAs to other employer-sponsored retirement plans like 401(k)s and SEP IRAs, several key differences emerge. The most striking is the ease of administration and lower costs associated with SIMPLE IRAs, making them particularly appealing for small businesses. However, this simplicity comes with trade-offs, such as lower contribution limits compared to 401(k) plans and less flexibility in plan design. For small business owners, the choice among these plans often boils down to balancing the need for simplicity and cost-effectiveness with the desire to provide a comprehensive retirement benefit. Employees, on the other hand, should weigh the benefits of higher contribution limits and potential employer matching against the plan's limitations and their personal retirement goals. Contributing to a Roth IRA is a straightforward process but requires adherence to guidelines to maximize its benefits. The first step involves selecting a financial institution that offers Roth IRA accounts. Once an account is set up, contributions can be made either as a lump sum or through regular contributions throughout the year. It's important to note the contribution limits and ensure that your income falls within the eligible range for contributing to a Roth IRA. The flexibility of Roth IRA contributions allows for strategic planning, especially for those anticipating fluctuations in income. Individuals can adjust their contributions year by year, taking advantage of lower income years to contribute more and thus leverage the tax-free growth potential of the Roth IRA. Additionally, for those with irregular income, setting up automatic contributions can ensure consistent savings without the need to actively manage the process. Contributing to a SIMPLE IRA typically involves coordination between the employee and the employer. For employees, the process starts by electing to participate in the employer’s SIMPLE IRA plan and then deciding on the contribution amount, which is usually a percentage of their paycheck. These contributions are then automatically deducted from each paycheck and deposited into the SIMPLE IRA account. For employers, setting up a SIMPLE IRA involves selecting a financial institution to administer the plan, setting up the plan documents, and then facilitating employee contributions. Employers are also responsible for making matching contributions or non-elective contributions, as per the plan’s terms. The ease of administration and the direct payroll deduction process make SIMPLE IRAs an attractive and efficient retirement savings option for both employers and employees in small businesses. Effectively managing contributions to either Roth or SIMPLE IRAs is a crucial aspect of retirement planning. For Roth IRAs, this means being mindful of income changes, as they directly affect eligibility and contribution limits. Regularly monitoring and adjusting contributions can optimize the tax benefits and growth potential of the IRA. For SIMPLE IRAs, it's essential to keep track of the employer's contributions alongside your own, ensuring that the total contributions don't exceed the annual limits. Account monitoring is not just about tracking contributions; it's also about investment performance and adjusting strategies as needed. Both Roth and SIMPLE IRAs offer a range of investment options, and choosing the right mix can significantly impact retirement savings growth. Regular reviews and adjustments to the investment portfolio, ideally with the guidance of a financial advisor, can help in aligning the investments with changing risk tolerances and retirement timelines. Roth IRAs, distinguished by their after-tax contributions and tax-free withdrawals, cater to those anticipating higher future tax rates, offering a unique long-term growth strategy. They require careful attention to contribution limits, and eligibility criteria based on income, and offer substantial benefits like flexibility in withdrawals and the absence of Required Minimum Distributions (RMDs). On the other hand, SIMPLE IRAs, designed for small businesses and their employees, offer a straightforward, cost-effective retirement plan option with higher contribution limits and immediate tax benefits. Their ease of administration and suitability for small-scale operations make them an attractive alternative to more complex plans like 401(k)s. Both Roth and SIMPLE IRAs necessitate diligent management, with a focus on aligning contributions and investment choices to individual retirement goals and financial circumstances. Overview of Individual Retirement Accounts (IRAs)

Differences Between SIMPLE and Roth IRA Contributions

Understanding Roth IRAs

Definition and Key Characteristics of Roth IRAs

Eligibility Criteria for Roth IRA Contributions

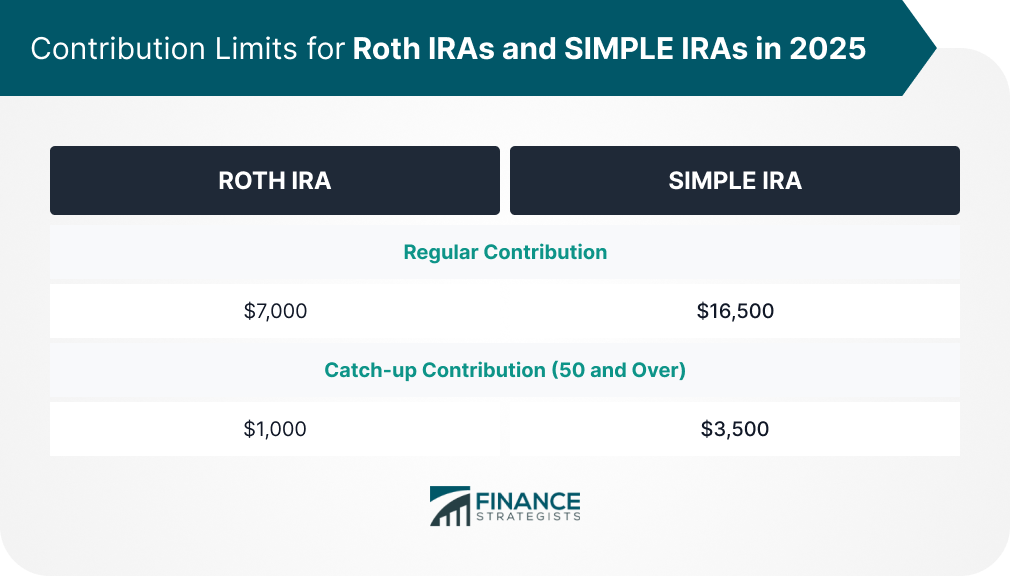

Contribution Limits for Roth IRAs

Tax Treatment of Roth IRA Contributions and Withdrawals

Benefits of Choosing a Roth IRA

Exploring SIMPLE IRAs

Definition and Basic Features of SIMPLE IRAs

Eligibility Criteria for SIMPLE IRA Contributions (Focus on Employer Aspect)

Contribution Limits for SIMPLE IRAs

Tax Treatment of SIMPLE IRA Contributions and Withdrawals

Comparison With Other Employer-Sponsored Retirement Plans

Making Contributions to SIMPLE and Roth IRAs: Step-By-Step Guide

How to Contribute to a Roth IRA

How to Contribute to a SIMPLE IRA

Managing SIMPLE and Roth IRA Contributions and Account Monitoring

Final Thoughts

Simple and Roth IRA Contributions FAQs

Simple IRA contributions are made pre-tax, benefiting employees of small businesses with higher contribution limits. Roth IRA contributions are post-tax, with tax-free growth and withdrawals, ideal for those expecting higher future tax rates.

Simple IRA contributions reduce taxable income in the year they are made, while Roth IRA contributions do not offer immediate tax deductions but provide tax-free growth and withdrawals in retirement.

Yes, you can contribute to both a Simple and a Roth IRA in the same year, as long as you meet the eligibility criteria and adhere to the respective contribution limits for each.

Eligibility for Simple IRA contributions primarily depends on being an employee of a small business. For Roth IRAs, eligibility is based on income levels, with contribution limits phased out at higher incomes.

There are no age limits for contributing to a Simple IRA. For Roth IRAs, contributions can be made at any age as long as you have earned income and meet the income eligibility criteria.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.