The Mega Backdoor Roth IRA (Individual Retirement Arrangement) Strategy is a financial planning technique that enables eligible individuals to contribute substantially larger amounts to a Roth IRA than the standard annual limits permit. This strategy involves making after-tax contributions to an eligible employer-sponsored retirement plan, such as a 401(k), 403(b), or 457(b) plan and subsequently rolling those funds into a Roth IRA through in-service distributions. The Mega Backdoor Roth IRA Strategy offers several benefits, including tax-free growth on investments, tax-free withdrawals during retirement, and increased flexibility in investment options. However, the strategy also involves potential risks and complexities, making it crucial for individuals to fully understand the process and consult with a financial advisor to determine if it suits their financial goals. For an individual to take advantage of the Mega Backdoor Roth IRA Strategy, they must participate in one of the following retirement plans: In addition to participating in an eligible retirement plan, individuals must meet the following requirements: The plan allows after-tax contributions. The plan offers in-service distributions. The participant follows the plan-specific guidelines. The Mega Backdoor Roth IRA Strategy involves making after-tax contributions to an eligible retirement plan, taking in-service distributions, and rolling over the funds into a Roth IRA. The frequency and timing of implementing the Mega Backdoor Roth IRA Strategy depend on individual circumstances and plan guidelines. Consult a financial advisor for personalized guidance. The Mega Backdoor Roth IRA Strategy allows individuals to contribute significantly more to a Roth IRA than traditional methods, potentially leading to higher retirement savings. Tax-Free Growth: Investments within a Roth IRA grow tax-free. Tax-Free Withdrawals: Qualified withdrawals from a Roth IRA are tax-free during retirement. Roth IRAs can be a valuable estate planning tool, as they do not require minimum distributions and can be passed on to beneficiaries tax-free. Roth IRAs offer a wide range of investment options, providing more flexibility compared to many employer-sponsored retirement plans. Laws and regulations governing retirement plans and the Mega Backdoor Roth IRA Strategy may change, impacting the strategy's effectiveness or availability. Not all retirement plans allow for in-service distributions, which is a crucial strategy component. Pro-rata rule: If rolling over funds from a traditional IRA to a Roth IRA, the pro-rata rule may apply, causing unexpected tax consequences. Five-year Rule: Roth IRA withdrawals must meet the five-year rule to qualify for tax-free treatment. Implementing the Mega Backdoor Roth IRA Strategy may impact your ability to contribute to other retirement accounts. The Mega Backdoor Roth IRA Strategy can be complex, and individuals may need professional guidance to execute it properly. Both the Mega Backdoor Roth IRA and the Traditional Backdoor Roth IRA strategies allow individuals to contribute to a Roth IRA through alternative means, bypassing income limits. However, there are key differences between the two strategies: The Mega Backdoor Roth IRA Strategy involves making after-tax contributions to an eligible employer-sponsored retirement plan. In contrast, the Traditional Backdoor Roth IRA Strategy involves contributing to a traditional IRA. The Mega Backdoor Roth IRA Strategy allows for significantly higher contributions than the Traditional Backdoor Roth IRA Strategy. Each strategy has its advantages and disadvantages, depending on individual circumstances and financial goals. The Mega Backdoor Roth IRA Strategy allows for larger contributions, but may be more complex and have limited availability. The Traditional Backdoor Roth IRA Strategy is simpler but has lower contribution limits. Individuals should evaluate their financial goals, retirement plan options, and tax implications to determine which strategy is best suited for their circumstances. Consulting with a financial advisor can provide personalized guidance. To get the most out of the Mega Backdoor Roth IRA Strategy, individuals should: Contribute the maximum allowable amount to their retirement plan. Be proactive in tracking contributions and growth. Follow plan-specific guidelines and IRS regulations. Keeping up-to-date on legislative changes and IRS regulations can help individuals adapt their strategy as needed and minimize potential risks. A financial advisor can provide personalized guidance and support in implementing the Mega Backdoor Roth IRA Strategy, helping individuals navigate complexities and make informed decisions. Mega Backdoor Roth IRA Strategy is a powerful financial planning technique that allows eligible individuals to contribute significantly larger amounts to a Roth IRA than the standard annual limits permit. By making after-tax contributions to an eligible employer-sponsored retirement plan and subsequently rolling those funds into a Roth IRA through in-service distributions, individuals can benefit from tax-free growth on investments, tax-free withdrawals during retirement, increased flexibility in investment options, and potential estate planning advantages. The process involves confirming eligibility, making after-tax contributions, tracking contributions and growth, requesting in-service distributions, executing a Roth IRA rollover, and managing investments within the Roth IRA. The frequency and timing of implementing the strategy depend on individual circumstances and plan guidelines. While the Mega Backdoor Roth IRA Strategy offers numerous benefits, there are potential risks and drawbacks to consider. Legislative changes, limited availability of in-service distributions, tax implications such as the pro-rata rule and the five-year rule, the impact on other retirement contributions, and the complexity and administrative burden are factors that individuals should carefully evaluate. To maximize the benefits of the Mega Backdoor Roth IRA Strategy, individuals should contribute the maximum allowable amount, track contributions and growth, follow plan-specific guidelines and regulations.What Is the Mega Backdoor Roth IRA Strategy?

Eligibility and Requirements for the Mega Backdoor Roth IRA Strategy

Eligible Retirement Plans

Key Requirements

Process for Implementing Mega Backdoor Roth IRA Strategy

Overview of the Process

Step-By-Step Guide

1. Confirm Eligibility: Ensure you participate in an eligible retirement plan and meet the requirements.

2. Make After-Tax Contributions: Contribute after-tax dollars to your eligible retirement plan, up to the annual limit set by the IRS.

3. Track Contributions and Growth: Keep track of your retirement plan after-tax contributions and any growth.

4. Request In-Service Distributions: Request a distribution of your after-tax contributions and associated growth from your retirement plan.

5. Execute Roth IRA Rollover: Roll over the distributed funds into a Roth IRA, following IRS guidelines.

6. Manage Investments Within Roth IRA: Choose and manage investments within your Roth IRA to maximize growth potential.

Frequency and Timing Considerations

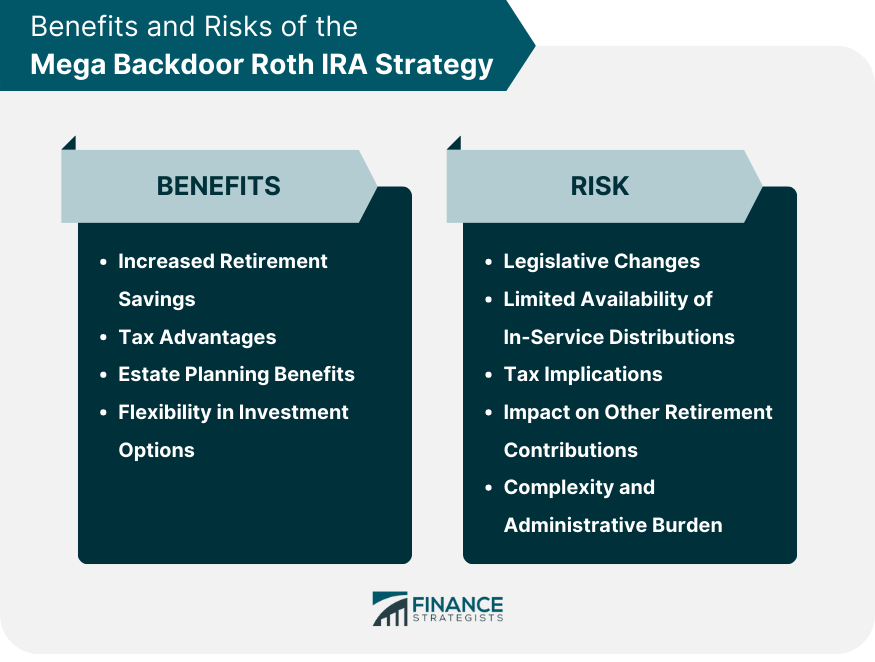

Benefits of the Mega Backdoor Roth IRA Strategy

Increased Retirement Savings

Tax Advantages

Estate Planning Benefits

Flexibility in Investment Options

Potential Risks of the Mega Backdoor Roth IRA Strategy

Legislative Changes

Limited Availability of In-Service Distributions

Tax Implications

Impact on Other Retirement Contributions

Complexity and Administrative Burden

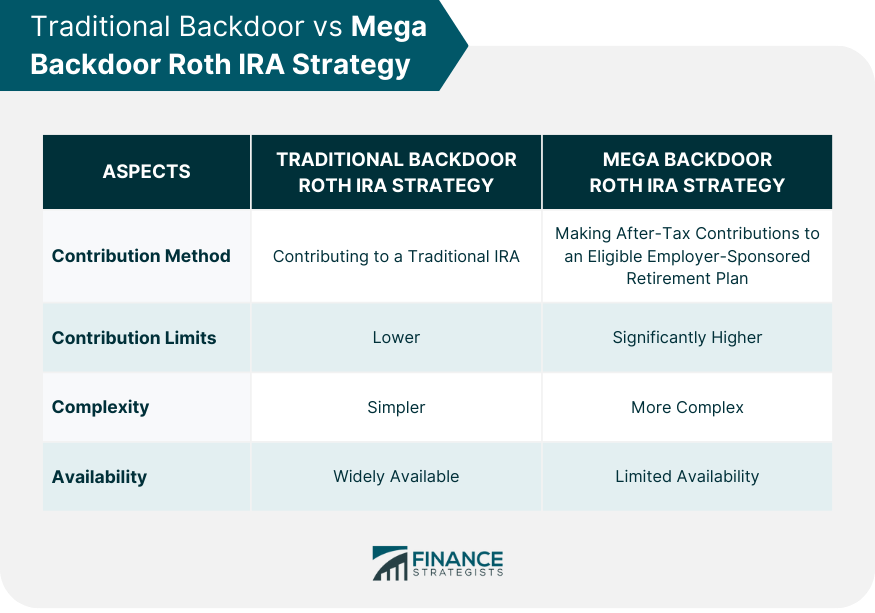

Traditional Backdoor vs. Mega Backdoor Roth IRA Strategy

Pros and Cons of Each Strategy

Choosing the Right Strategy Based on Individual Circumstances

Best Practices for the Mega Backdoor Roth IRA Strategy

Maximizing the Benefits of the Strategy

Staying Informed About Regulatory Changes

Working With a Financial Advisor

Conclusion

Mega Backdoor Roth IRA Strategy FAQs

The Mega Backdoor Roth IRA Strategy is a retirement savings strategy that allows high-income earners to contribute up to $72,000 as of 2026 ($70,000 in 2025) to a Roth IRA through after-tax contributions to a 401(k) plan.

The Mega Backdoor Roth IRA Strategy is available to individuals with a 401(k) plan that allows for after-tax contributions and in-service distributions, which means they can withdraw the after-tax contributions and convert them to a Roth IRA still employed.

The Mega Backdoor Roth IRA Strategy allows individuals to contribute more to their retirement savings, take advantage of tax-free growth, and lower their taxes in retirement.

Yes, there are limitations to the Mega Backdoor Roth IRA Strategy. Not all 401(k) plans allow after-tax contributions, and there are contribution limits and income limits for Roth IRA contributions.

Some key considerations when using the Mega Backdoor Roth IRA Strategy include understanding the tax implications, monitoring contribution limits, and ensuring that the 401(k) plan allows for in-service distributions. It is also important to consult with a financial advisor or tax professional before implementing the strategy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.