Downside risk is a crucial aspect of investing and financial planning. It encompasses various forms, such as market risk, credit risk, liquidity risk, operational risk, and model risk. Economic factors, market conditions, company-specific factors, and investor behavior all contribute to downside risk, making it a complex concept. Measuring downside risk involves using metrics like Value at Risk (VaR), Conditional Value at Risk (CVaR), Sortino Ratio, Omega Ratio, downside deviation, and maximum drawdown. To manage downside risk, strategies such as diversification, hedging, stop-loss orders, and portfolio insurance can be employed, each with its own advantages and considerations. Downside risk plays a significant role in modern portfolio theory, influencing concepts like the Efficient Frontier, the Capital Asset Pricing Model (CAPM), and Beta. Behavioral finance also recognizes its importance, with concepts such as Prospect Theory, loss aversion, and mental accounting impacting investment decision-making. Systematic risk, also known as market risk or non-diversifiable risk, refers to the risk associated with broad market movements that affect all investments in the market. This type of risk is caused by factors such as economic conditions, interest rates, and geopolitical events that are beyond the control of individual investors. Systematic risk cannot be eliminated through diversification, but it can be mitigated through hedging strategies or by investing in assets with low correlations. Unsystematic risk, also known as specific risk or diversifiable risk, refers to the risk associated with a specific investment or industry. This type of risk arises from factors unique to a particular company or sector, such as management decisions, product launches, or regulatory changes. Unsystematic risk can be reduced through diversification by investing in a broad range of assets or industries. Credit risk, also known as default risk, is the potential loss resulting from a borrower's failure to repay a loan or meet their contractual obligations. Credit risk affects investors in fixed-income securities, such as bonds and loans, where the risk of default can directly impact the value of their investments. Investors can manage credit risk by conducting thorough credit assessments, diversifying their fixed-income holdings, and investing in credit protection instruments, such as credit default swaps. Liquidity risk refers to the risk that an investor might not be able to quickly sell an asset at a fair price due to a lack of buyers or sellers in the market. Illiquid assets can be more susceptible to price fluctuations, making it challenging for investors to exit their positions without incurring significant losses. To manage liquidity risk, investors can focus on investing in liquid assets, maintain a cash reserve, or use limit orders when trading illiquid securities. Operational risk is the risk of loss resulting from inadequate or failed internal processes, people, systems, or external events. This type of risk can arise from various sources, such as technology failures, human errors, fraud, or natural disasters. Operational risk can be managed through robust internal controls, regular audits, employee training, and effective risk management systems. Model risk refers to the potential losses resulting from the use of financial models that fail to accurately predict market behavior or capture the complexity of financial instruments. Model risk can lead to incorrect investment decisions, valuation errors, and risk management failures. Investors and financial institutions can mitigate model risk by validating and testing their models, incorporating multiple approaches, and maintaining a comprehensive understanding of the underlying assumptions and limitations. Interest rate fluctuations can have a significant impact on downside risk. Rising interest rates can negatively affect the value of fixed-income securities and increase borrowing costs for companies, potentially leading to reduced profits and lower stock prices. Investors should monitor changes in interest rates and adjust their portfolios accordingly to manage downside risk. Inflation erodes the purchasing power of money, potentially reducing the real returns on investments. High inflation can lead to increased input costs for companies, negatively impacting their profitability and stock prices. To protect their portfolios from inflation risk, investors can consider investing in inflation-protected securities or assets with a strong track record of outpacing inflation, such as stocks and real estate. Exchange rate fluctuations can introduce downside risk for investors with exposure to foreign currencies or assets denominated in foreign currencies. A weakening domestic currency can lead to increased import costs, while a strengthening domestic currency can negatively impact export-driven companies. Investors can manage currency risk by diversifying their portfolios across different currencies or using currency hedging strategies. Market sentiment, or the collective attitude of investors toward a particular asset or market, can significantly influence downside risk. Negative market sentiment can lead to selling pressure and falling asset prices, while positive sentiment can drive prices higher. Investors should be aware of prevailing market sentiment and consider its potential impact on their investments. Market cycles, or the recurring periods of expansion and contraction in financial markets, can contribute to downside risk. During market downturns, asset prices tend to decline, increasing the likelihood of losses for investors. By understanding market cycles and their potential impact on investments, investors can develop strategies to navigate different market environments and manage downside risk. The financial health of a company can directly impact its downside risk. Companies with weak financials, high debt levels, or poor cash flow may be more vulnerable to market downturns or adverse events, potentially leading to significant losses for investors. By conducting thorough financial analysis and selecting financially strong companies, investors can reduce downside risk in their portfolios. Effective corporate governance can help mitigate downside risk by promoting transparency, accountability, and ethical behavior within a company. Companies with poor corporate governance practices may be more susceptible to fraud, mismanagement, and regulatory penalties, potentially leading to substantial losses for investors. Investors should assess a company's corporate governance practices and prioritize investments in companies with strong governance structures. Emotional biases, such as fear or greed, can lead investors to make irrational decisions that increase downside risk. For example, investors may panic sell during market downturns or chase overvalued assets during market upswings. By recognizing and managing their emotional biases, investors can make more informed decisions and better manage downside risk. Cognitive biases, such as overconfidence or confirmation bias, can also contribute to downside risk by causing investors to overlook important information or make incorrect assumptions about their investments. To minimize the impact of cognitive biases, investors should maintain a disciplined investment process, seek diverse perspectives, and regularly review their investment assumptions. Value at Risk (VaR) is a widely-used measure of downside risk that estimates the maximum potential loss an investment portfolio could face over a specified period, given a specific confidence level. VaR helps investors quantify their exposure to market risk and make informed decisions about risk management strategies. Conditional Value at Risk (CVaR), also known as Expected Shortfall, is an extension of VaR that estimates the average loss an investment portfolio could experience during extreme market events, beyond the VaR threshold. CVaR provides a more comprehensive assessment of downside risk, as it considers the severity of potential losses in addition to their likelihood. The Sortino Ratio is a performance metric that evaluates an investment's risk-adjusted return by considering downside risk instead of total risk. The Sortino Ratio adjusts an investment's return for downside deviation, which measures the volatility of negative returns. A higher Sortino Ratio indicates better risk-adjusted performance. The Omega Ratio is another downside risk-adjusted performance metric that compares an investment's potential gains to its potential losses. The Omega Ratio takes into account the entire distribution of returns, making it more sensitive to the shape of the return distribution than other risk-adjusted metrics. A higher Omega Ratio indicates a more favorable risk-reward profile. Downside deviation is a measure of downside risk that focuses on the volatility of negative returns, providing a more targeted assessment of an investment's potential for losses. Downside deviation can be used to calculate other downside risk-adjusted performance metrics, such as the Sortino Ratio, and to compare the riskiness of different investments. Maximum drawdown is the largest peak-to-trough decline in the value of an investment portfolio over a specified period. This measure of downside risk reflects the worst possible loss an investor could have experienced during the period, providing insight into the potential impact of market downturns on a portfolio's value. Asset allocation is the process of spreading investments across different asset classes, such as stocks, bonds, and cash, to manage downside risk. By allocating assets according to their risk and return characteristics, investors can create portfolios that balance risk and reward, reducing the impact of any single asset class's poor performance. Geographic diversification involves investing in assets from various countries and regions to reduce downside risk. By spreading investments across different economies, investors can mitigate the impact of regional economic downturns, political instability, or currency fluctuations on their portfolios. Options are financial contracts that give investors the right, but not the obligation, to buy or sell an underlying asset at a specified price before a specific expiration date. Options can be used to hedge downside risk by allowing investors to lock in potential profits or protect against potential losses. Futures are standardized contracts that obligate the buyer to purchase and the seller to sell, a specific asset at a predetermined price and date in the future. Futures can be used to hedge downside risk by allowing investors to lock in a future price for an asset, reducing the uncertainty associated with market fluctuations. Swaps are financial contracts that involve the exchange of one set of cash flows for another. Swaps can be used to hedge downside risk by allowing investors to manage their exposure to interest rates, currency fluctuations, or credit risk. Stop-loss orders are instructions to sell an investment if its price falls below a specified level. By using stop-loss orders, investors can limit their downside risk by automatically exiting a position if the market moves against them, preventing further losses. Portfolio insurance is a risk management strategy that uses derivatives to protect a portfolio against market downturns. By dynamically adjusting a portfolio's asset allocation or using options to create a protective floor, portfolio insurance can help limit downside risk while preserving the potential for upside gains. The Efficient Frontier is a concept in MPT that represents the set of optimal portfolios offering the highest expected return for a given level of risk. Portfolios on the Efficient Frontier are diversified to minimize downside risk and maximize return, providing the best possible risk-reward trade-off for investors. The Capital Asset Pricing Model (CAPM) is a model in MPT that calculates an investment's expected return based on its systematic risk, represented by its beta. The CAPM suggests that the only way to achieve higher returns is to accept more downside risk, reinforcing the importance of understanding and managing downside risk in investing. Beta is a measure of an investment's sensitivity to market movements, reflecting its systematic risk. A beta greater than one indicates that the investment is more volatile and has higher downside risk than the market, while a beta less than one indicates lower volatility and downside risk. Investors can use beta to assess an investment's downside risk and choose investments that align with their risk tolerance. Prospect Theory, a cornerstone of behavioral finance, suggests that people make decisions based on the potential value of losses and gains rather than the final outcome. This theory highlights the importance of understanding downside risk, as losses are often perceived as more significant than equivalent gains. Loss aversion, a concept related to Prospect Theory, suggests that people prefer to avoid losses more than they enjoy gains. This behavioral bias can lead investors to hold onto losing investments for too long or sell winning investments too quickly, highlighting the importance of managing downside risk and maintaining a disciplined investment approach. Mental accounting refers to the tendency for people to categorize and treat money differently depending on where it comes from, where it is kept, or how it is spent. This cognitive bias can affect investors' perceptions of downside risk and influence their investment decisions, underscoring the need for a comprehensive understanding of downside risk. Downside risk is a crucial factor in investing and financial planning, encompassing various forms such as market risk, credit risk, liquidity risk, operational risk, and model risk. Economic, market, company-specific factors, and investor behavior all contribute to downside risk, making it a complex concept. Measuring downside risk involves metrics like Value at Risk (VaR), Conditional Value at Risk (CVaR), Sortino Ratio, Omega Ratio, downside deviation, and maximum drawdown. Strategies to manage downside risk include diversification, hedging, stop-loss orders, and portfolio insurance, each with its own advantages and considerations. Downside risk is significant in modern portfolio theory, influencing concepts like the Efficient Frontier, the Capital Asset Pricing Model (CAPM), and Beta. Behavioral finance also recognizes its importance with concepts such as Prospect Theory, loss aversion, and mental accounting impacting investment decision-making. Consider professional wealth management services to navigate its complexities and align your financial plans with your risk tolerance and objectives.What Is Downside Risk?

Different Types of Downside Risk

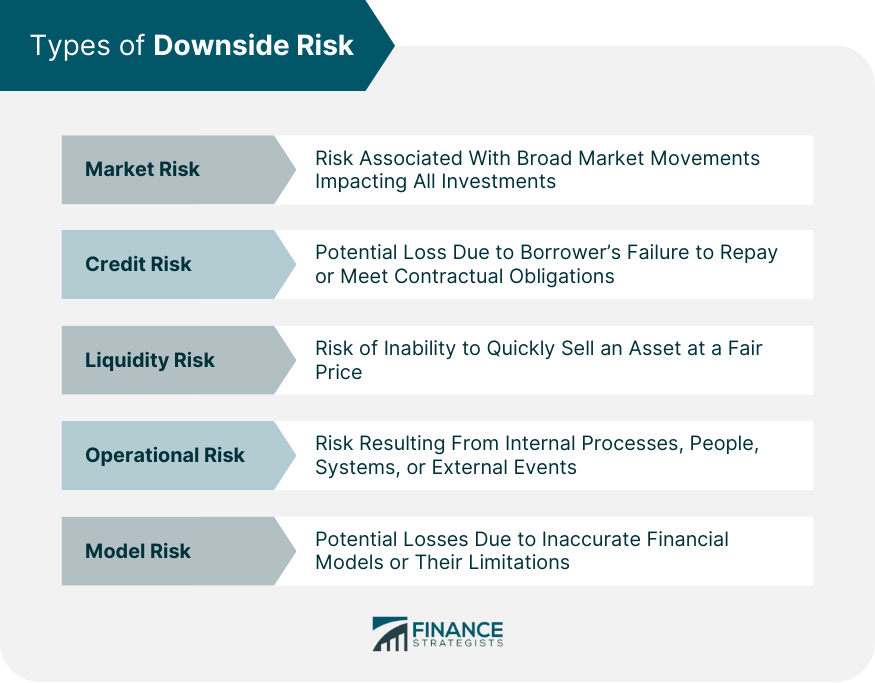

Market Risk

Systematic Risk

Unsystematic Risk

Credit Risk

Liquidity Risk

Operational Risk

Model Risk

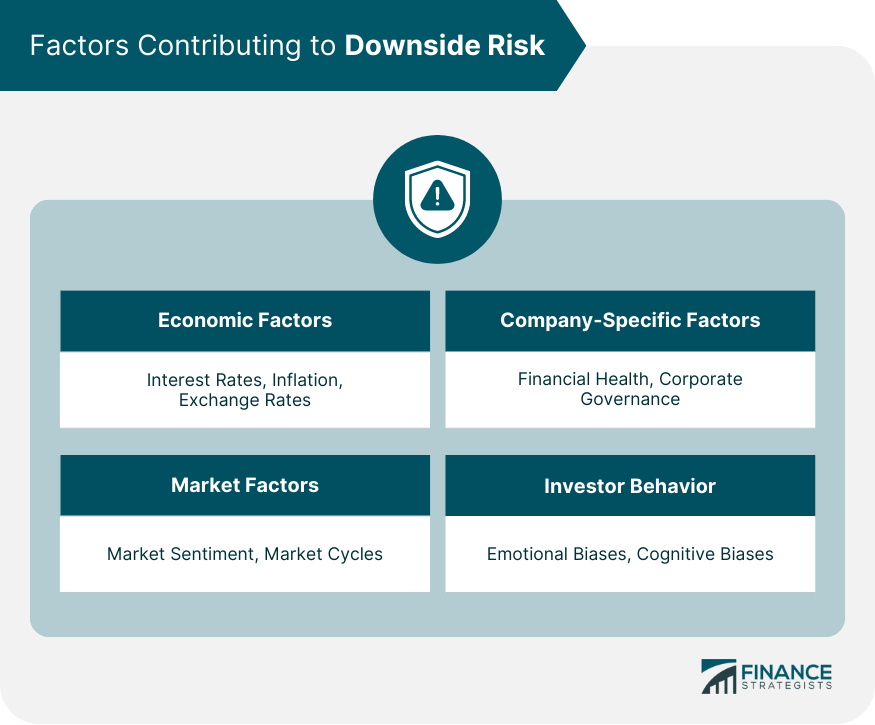

Factors Contributing to Downside Risk

Economic Factors

Interest Rates

Inflation

Exchange Rates

Market Factors

Market Sentiment

Market Cycles

Company-Specific Factors

Financial Health

Corporate Governance

Investor Behavior

Emotional Biases

Cognitive Biases

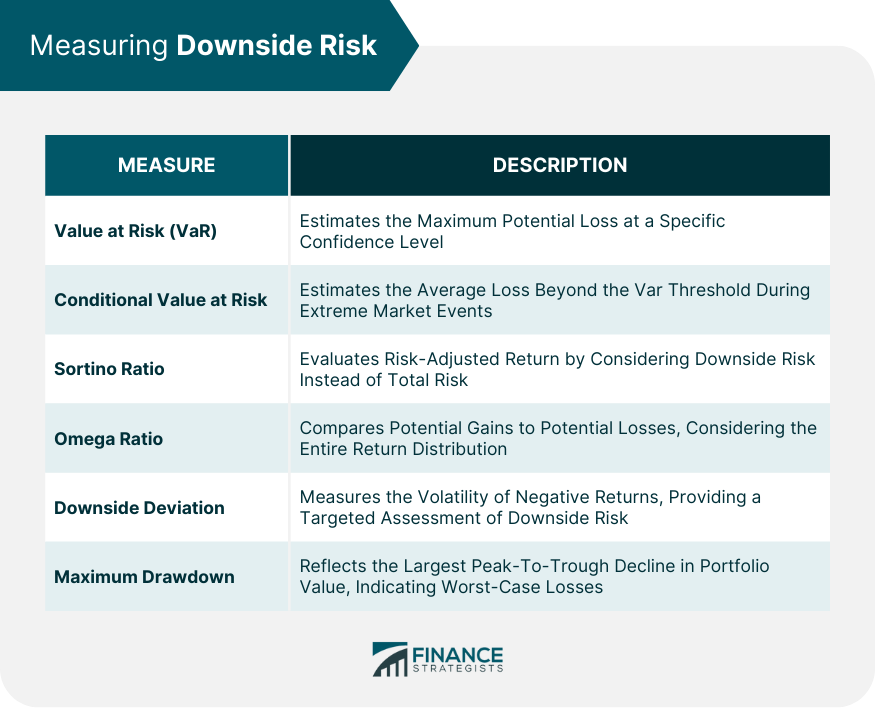

Measuring Downside Risk

Value at Risk (VaR)

Conditional Value at Risk (CVaR)

Downside Risk-Adjusted Performance Metrics

Sortino Ratio

Omega Ratio

Downside Deviation

Maximum Drawdown

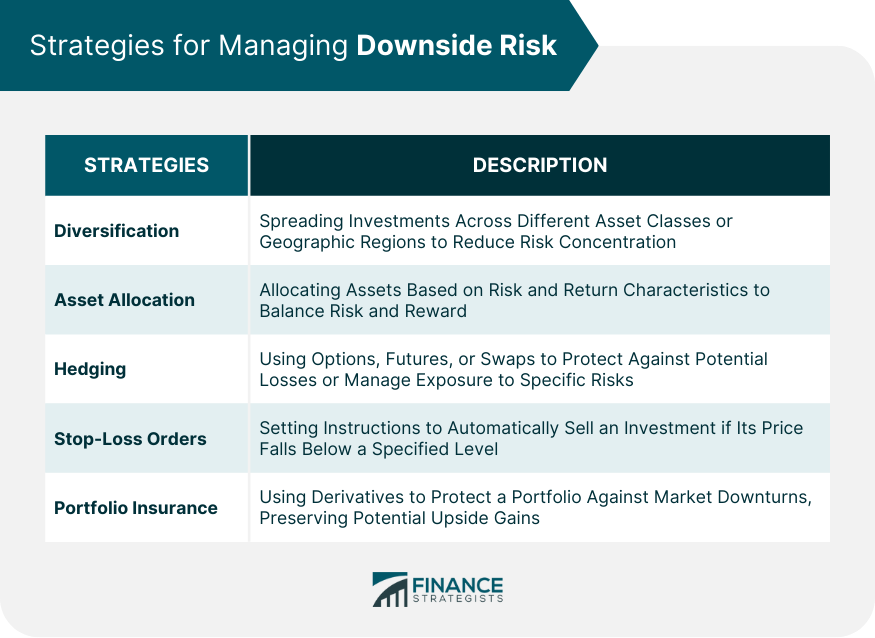

Strategies for Managing Downside Risk

Diversification

Asset Allocation

Geographic Diversification

Hedging

Options

Futures

Swaps

Stop-Loss Orders

Portfolio Insurance

Role of Downside Risk in Modern Portfolio Theory (MPT)

Efficient Frontier

Capital Asset Pricing Model (CAPM)

Concept of Beta

Downside Risk and Behavioral Finance

Prospect Theory

Loss Aversion

Mental Accounting

Final Thoughts

Downside Risk FAQs

Downside risk refers to the potential for negative outcomes or losses in an investment, often associated with factors such as market risk, credit risk, liquidity risk, operational risk, and model risk.

Investors can measure downside risk using various metrics, including Value at Risk (VaR), Conditional Value at Risk (CVaR), Sortino Ratio, Omega Ratio, downside deviation, and maximum drawdown.

Strategies for managing downside risk include diversification, hedging, stop-loss orders, and portfolio insurance, each offering unique advantages and considerations.

In modern portfolio theory, downside risk plays a crucial role in concepts such as the Efficient Frontier, the Capital Asset Pricing Model (CAPM), and Beta, emphasizing the importance of understanding and managing downside risk in investing.

Behavioral finance recognizes the significance of downside risk in investment decision-making, with concepts like Prospect Theory, loss aversion, and mental accounting highlighting its importance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.