Convertible bonds, a unique blend of bonds and stocks, offer strategic investors the option to convert their bonds into a set number of company shares at chosen points during their lifespan. As a bond, it pays periodic interest and repays the principal at maturity, but it can also be converted into equity, providing potential upside in a rising market. If the company's stock price is low, investors can opt not to convert, thus minimizing risk. Key features of convertible bonds include the conversion ratio, conversion price, and conversion premium. Offering a distinctive risk-return profile, convertible bonds protect falling markets, as investors will receive at least the bond's par value at maturity and have the potential for profit in rising markets. Understanding these features is essential for investors considering these bonds for their portfolio diversification. The conversion ratio of a convertible bond refers to the number of common shares that each bond can be converted into. This ratio is fixed at the time of issuance and is a key factor in determining the value of the bond. The conversion ratio directly affects the upside potential for the bondholder, should they decide to convert the bond into shares. A higher conversion ratio means more shares per bond, offering greater potential profit if the company's stock performs well. The conversion price is the nominal or face value price per share at which the bond can be converted into shares. It's usually set at a premium above the prevailing market price at the time of the bond's issuance. This premium incentivizes the bondholder to opt for conversion only when the company's share price appreciates significantly. This represents the difference between the current share price and the conversion price, expressed as a percentage of the current share price. The conversion value is the market price of the shares into which the bond can be converted. The conversion premium represents the difference between the current share price and the conversion price, expressed as a percentage of the current share price. This premium indicates the additional amount an investor will pay for the convertible bond over the cost of buying the common stock directly. A lower conversion premium might make the convertible bond more attractive, as it suggests a lower threshold for profitability upon conversion. In their initial life stage, convertible bonds act just like regular bonds. The issuing company pays the bondholder periodic interest, known as coupon payments, to use the funds. These payments are typically made semi-annually based on the bond's stated interest rate and face value. This phase benefits bondholders because they receive a steady income stream regardless of the company's share price performance. It also offers a security measure, as bondholders have a higher claim on the company's assets than shareholders in case of liquidation. The second phase of a convertible bond's life kicks in when the company's share price appreciates significantly. At this point, the bondholder may choose to convert their bonds into a predetermined number of the company's shares. The number of shares each bond can be converted into is determined by the conversion ratio, which is set when the bond is issued. For instance, if the conversion ratio is 20:1, each bond can be converted into 20 shares of the issuing company. When the company's share price is higher than the bond's conversion price, it may be advantageous for bondholders to convert their bonds into shares. They can either hold these shares and benefit from any further price appreciation and dividends or sell them to realize the profit. If the company's share price does not appreciate as expected, the bondholder can choose not to convert their bonds into shares. They can continue to hold the bond, receive periodic interest payments, and get back the bond's face value at maturity. Thus, the flexibility of convertible bonds allows bondholders to benefit from both the stability of fixed-income securities and the growth potential of equities. One of the distinguishing features of convertible bonds is the inclusion of call and put options. Understanding these features helps investors determine the potential risks and rewards associated with owning a convertible bond. The call feature gives the issuer, usually a corporation, the right to redeem the convertible bond before its maturity date. This typically happens when the interest rates have fallen significantly since the issuance of the bond, allowing the issuer to refinance its debt at a lower rate. The call feature is a risk for the bondholder because it forces early redemption, potentially at an unfavorable time. When a bond is called, the investor must relinquish the bond, and in return, the issuer pays the call price, which is usually the bond's face value plus accrued interest. However, the call feature has in-built protection for the investor - call protection. It is a period after the bond's issuance during which the issuer cannot call the bond. This period typically lasts several years. On the other hand, a put option gives the bondholder the right to sell the bond back to the issuer before its maturity date at a predetermined put price. The put feature provides bondholders a safeguard against a significant rise in interest rates or a drop in the creditworthiness of the issuer. The putability feature is especially beneficial to investors during times of economic uncertainty. If the issuer's creditworthiness falls or market interest rates rise, causing the bond's value to decrease, the bondholder can exercise the put option, forcing the issuer to repurchase the bond at the put price. Both callability and putability significantly influence a bondholder's decision to convert their bonds into shares. If an issuer calls its convertible bonds, investors may decide to convert their bonds into shares rather than accepting the call price, especially if the shares are trading at a higher price. On the other hand, if the issuer's stock is not performing well, but the issuer's bonds are, investors may choose to exercise the put option. This option allows them to exit their position and recover a part or all of their initial investment. Convertible bonds also have unique yield and income features that can offer investors a consistent income stream and potential for capital appreciation. Like traditional bonds, convertible bonds make regular interest payments to bondholders. The bond yield, or the return a bondholder gets from these interest payments relative to the bond's price, is usually lower for convertible bonds compared to similar non-convertible bonds. The lower yield is because investors are willing to accept a lower return for the potential to benefit from the underlying stock's price appreciation. Yield-to-maturity (YTM) is a concept that applies to all bonds, not just convertible ones. It is the total return a bondholder can expect if they hold the bond until maturity and the issuer makes all scheduled interest payments. YTM is a useful measure for comparing bonds as it considers both the bond's current market price and its interest payments. Yield-to-Call (YTC), on the other hand, is specific to callable bonds, including many convertible bonds. YTC is the total return a bondholder can expect if the bond is called by the issuer. As with YTM, YTC considers the bond's current market price, its interest payments, and the call price. Convertible bonds are hybrid securities that combine features of bonds and equities, which makes them versatile investment tools. The equity component of a convertible bond gives the bondholder the right to convert their bond into a predetermined number of the issuer's common shares. The presence of this conversion option is what gives convertible bonds their potential for price appreciation. When the issuer's stock price rises significantly, converting the bond into shares may yield a higher return than holding the bond until maturity. Moreover, as a shareholder, the investor can benefit from dividends and has voting rights in the company. The bond component of a convertible bond provides investors with regular interest payments and the return of the bond's face value at maturity, assuming the issuer does not default. This bond feature offers downside protection as it guarantees a minimum return, unlike equities that do not have a predetermined return and can lose value. Owing to their dual nature, convertible bonds offer a balance between risk and reward. When the issuer's stock price is high, the equity component becomes more valuable, and the convertible bond behaves more like a stock. Conversely, when the stock price is low, the bond component provides a safety net, and the convertible bond acts more like a traditional bond. While straight bonds offer a fixed interest payment and return of principal at maturity, convertible bonds offer a lower interest rate but the potential for conversion into equity. This can offer greater returns if the company's stock performs well. Convertible bonds offer less upside potential and downside risk than common stocks. They offer the security of a bond with the opportunity for capital appreciation through conversion into stock. Like preferred stocks, convertible bonds offer a fixed income stream. However, they also allow converting into common stock, offering potentially higher returns. In the event of a company's liquidation, convertible bonds have higher seniority than preferred stocks, making them less risky. Convertible bonds present a compelling investment opportunity that combines the characteristics of both bonds and equities. Offering a unique risk-return profile, they provide investors with downside protection and the potential for appreciable returns in rising markets. The conversion ratio, conversion price, conversion premium, conversion value, and conversion parity are key features that investors need to understand before investing. Furthermore, these bonds go through distinct phases, namely the bond and conversion phases, giving investors different options based on market performance. Callability and putability features, as well as yield and income aspects, add additional layers of flexibility and security to the investment. Lastly, the hybrid nature of convertible bonds, integrating both equity and bond components, allows investors to balance between risk and reward effectively. Compared to straight bonds, common stocks, and preferred stocks, convertible bonds offer a unique set of advantages, positioning them as an attractive instrument for portfolio diversification.Overview of the Features of Convertible Bonds

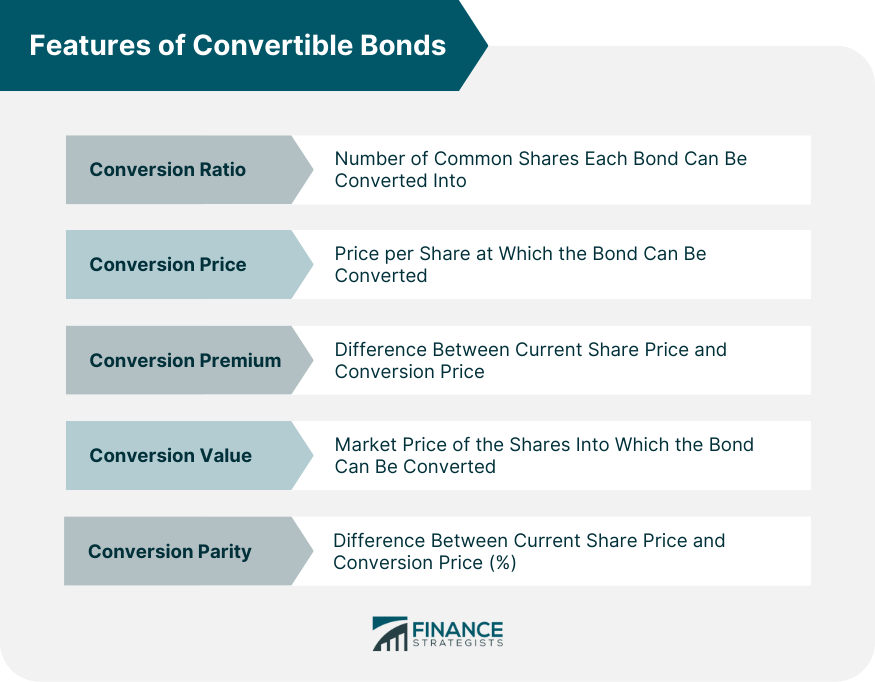

Features of Convertible Bonds

Conversion Ratio

Conversion Price

Conversion Premium

Conversion Value

Conversion Parity

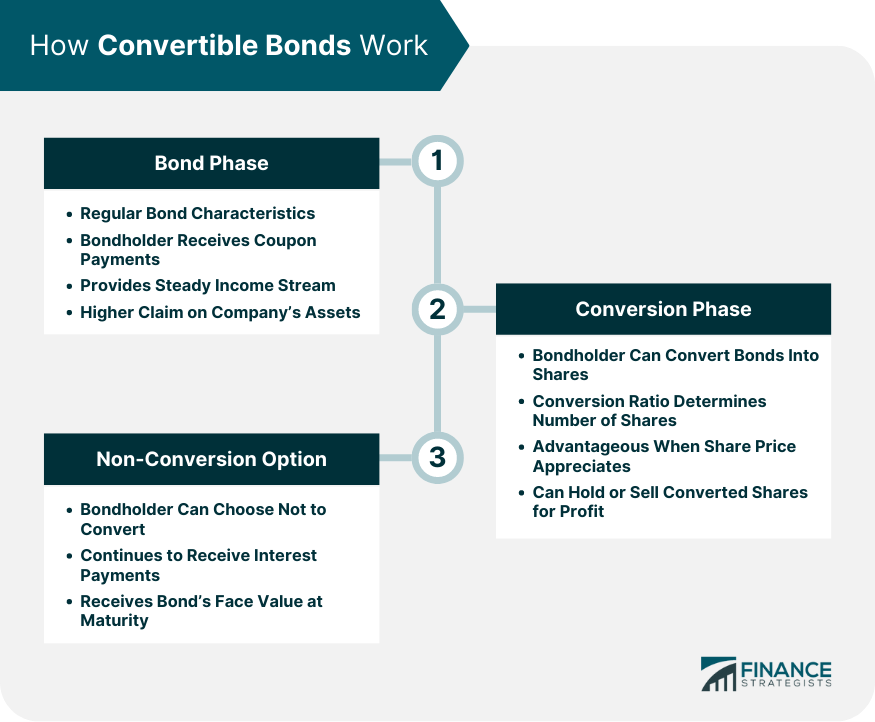

How Convertible Bonds Work

Bond Phase

Conversion Phase

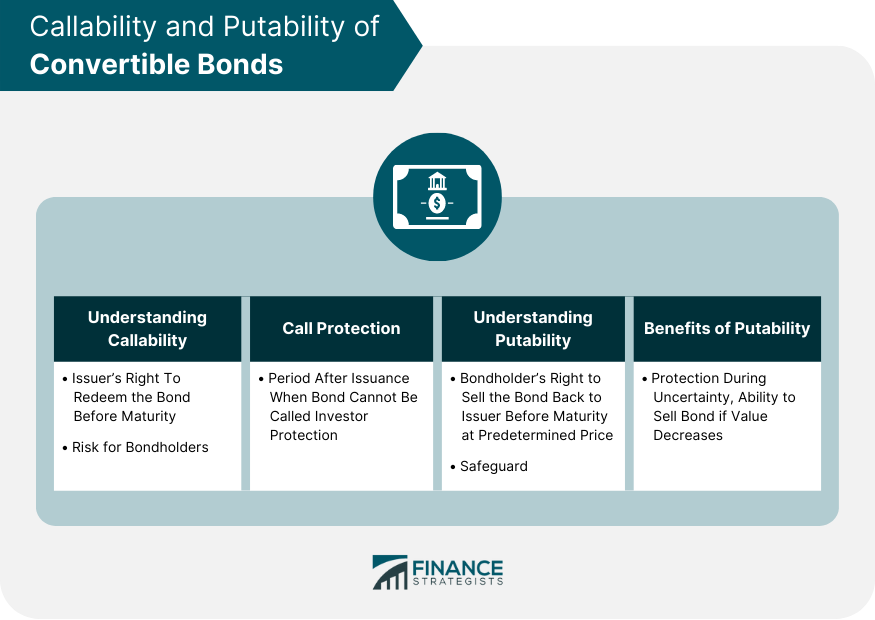

Callability and Putability of Convertible Bonds

Explanation of Callability

Understanding Putability

Impact on Conversion Decision

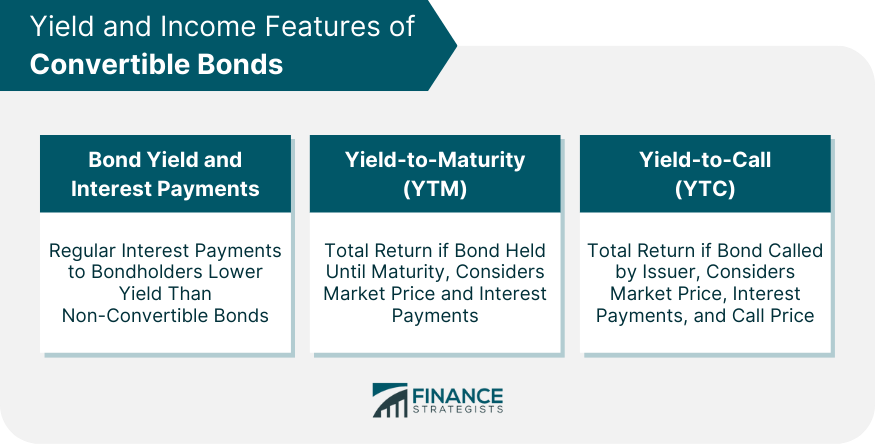

Yield and Income Features of Convertible Bonds

Bond Yield and Interest Payments

Yield-To-Maturity (YTM)

Yield-To-Call (YTC)

Hybrid Nature of Convertible Bonds: Equity and Bond Components

Equity Component and Its Implications

Bond Component and Its Advantages

Balancing Between the Two Components

Convertible Bonds vs Other Investment Instruments

Comparison With Straight Bonds

Comparison With Common Stocks

Comparison With Preferred Stocks

Conclusion

Features of Convertible Bonds FAQs

Convertible bonds have key features: conversion ratio (shares per bond), conversion price (price per share for conversion), conversion premium (difference between share price and conversion price), conversion value (market price of converted shares), and conversion parity (percentage difference between share price and conversion price).

Convertible bonds function in two phases: the bond phase and the conversion phase. During the bond phase, the issuing company pays the bondholder periodic interest. The conversion phase starts when the company's share price significantly appreciates, giving the bondholder an option to convert their bonds into shares.

Callability gives the issuer the right to redeem the bond before its maturity date, while putability gives the bondholder the right to sell the bond back to the issuer before its maturity at a predetermined price. These features can influence a bondholder's decision to convert their bonds into shares.

Convertible bonds make regular interest payments to bondholders, similar to traditional bonds, but at a lower yield due to the potential for stock price appreciation. Concepts like Yield-to-Maturity (YTM) and Yield-to-Call (YTC) apply to these bonds to measure potential returns.

Convertible bonds offer a lower interest rate but potential for conversion into equity compared to straight bonds. They provide less upside potential but more security than common stocks. Compared to preferred stocks, convertible bonds also allow conversion into common stock, offering potentially higher returns and less risk in case of liquidation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.