Capital gains for companies refer to the profit earned when a business sells a capital asset, such as real estate, stocks, bonds, or machinery, for a higher price than its original purchase cost or cost basis. The difference between the selling price and the cost basis is the capital gain. This financial outcome is pivotal for companies as it can significantly contribute to their overall profitability and liquidity. Moreover, capital gains can provide businesses with the necessary funds for expansion, debt reduction, or further investment. It's crucial to note that capital gains are subject to taxation, known as capital gains tax. The purpose of this tax is to generate revenue for the government from the economic growth reflected in the increased value of capital assets. Companies must strategically manage their capital gains to maximize profits and ensure regulatory compliance. Ordinary income and capital gains are different forms of income taxed at distinct rates. Ordinary income refers to earnings derived from a company's core business activities, including sales revenue, services rendered, or other routine operations. On the other hand, capital gains result from the sale of a capital asset. The tax rates applied to these income types vary, with capital gains often taxed at a lower rate. Typically, any asset owned by a company may be subject to capital gains tax upon sale. This includes tangible assets like buildings, machinery, and vehicles, as well as intangible assets like stocks, bonds, and intellectual property. The capital gain is calculated as the difference between the sale price and the cost basis of the asset. The length of time a company holds an asset before selling it can significantly impact the amount of capital gains tax owed. Assets held for over a year may qualify for lower long-term capital gains tax rates, while assets sold within a year of purchase are typically subject to higher short-term capital gains rates. Unlike individuals, corporations do not benefit from preferential tax rates on long-term capital gains. They are taxed at the regular corporate tax rate, which can be as high as 28% in the United States. This rate applies to both short-term and long-term capital gains. The capital gains tax calculation for a company is based on two main elements: the cost basis and adjustments to the cost basis. The cost basis of an asset is its original purchase price plus any associated acquisition costs. For example, if a company buys a piece of equipment for $500,000 and spends an additional $50,000 on transportation and installation, the cost basis would be $550,000. In some cases, the cost basis may need adjustment. For instance, capital improvements that add value to an asset can increase the cost basis, thereby reducing the capital gain when the asset is sold. Similarly, depreciation can decrease the cost basis, potentially increasing the capital gain. Certain provisions and exemptions in tax law can reduce a company's capital gains tax liability. In some jurisdictions, small businesses may qualify for a capital gains exemption. For example, the U.S. provides a 100% capital gains exclusion for Qualified Small Business Stock held for more than five years. Rollover provisions allow companies to defer capital gains tax if the proceeds from the sale of a business asset are used to purchase a similar asset within a specified period. Qualified Small Business Stock (QSBS) exemptions are another potential avenue for companies to reduce capital gains tax. They allow shareholders of eligible small businesses to exclude a portion, or in some cases, all of their capital gains from income, subject to certain conditions. Form 8949 is used by companies to report the sale and disposition of capital assets. It provides detailed information about each transaction, including the description of the asset, dates of acquisition and sale, proceeds from the sale, cost basis, and capital gain or loss. Schedule D is used to summarize and report the overall capital gains and losses for the tax year. It incorporates data from Form 8949 and calculates the net capital gain or loss to be reported on the corporation's income tax return. Companies are required to report and pay capital gains tax as part of their annual income tax filing. The specific deadlines vary by jurisdiction and the type of tax return the company is required to file. Failure to file on time can result in penalties and interest charges. Strategic Timing of Asset Sales: This can be a potent tool for minimizing capital gains tax. By delaying the sale of an asset until it qualifies for long-term capital gains treatment, a company may reduce its tax liability. Utilizing Capital Losses to Offset Gains: Companies can also use capital losses to offset capital gains. This practice involves selling assets at a loss to counterbalance gains from the sale of other assets, thus reducing the overall capital gains tax liability. Considering Tax-Advantaged Accounts: Companies can consider using tax-advantaged accounts like retirement accounts or health savings accounts, which can provide tax-free or tax-deferred growth of investments. Charitable Donations and Capital Gains Tax: In some cases, donating appreciated assets to a charitable organization can allow companies to avoid capital gains tax on those assets while also benefiting from a charitable deduction. Companies operating internationally need to be aware of capital gains tax laws in foreign jurisdictions. These laws vary widely and can significantly impact the tax liability of a company's foreign operations. Tax treaties between countries can affect the taxation of cross-border capital gains. These treaties can provide for reduced rates or exemptions from capital gains tax, particularly for specific types of income or entities. To avoid double taxation, many jurisdictions offer foreign tax credits for taxes paid to foreign governments on income earned abroad. This credit can be used to offset the company's domestic tax liability. Importance of Accurate Reporting: Accurate reporting of capital gains and losses is crucial for maintaining compliance with tax laws. Errors in reporting can result in audits, penalties, and interest charges and can damage a company's reputation. Common Pitfalls and Mistakes to Avoid: Common mistakes in capital gains taxation include inaccurately calculating the cost basis, failing to account for capital improvements or depreciation, and not correctly applying rollover provisions or exemptions. Penalties for Non-compliance: Non-compliance with capital gains tax laws can result in severe penalties, including monetary fines and interest charges. Capital gains tax is an intricate area of corporate finance and taxation, impacting the strategic decisions of companies across a spectrum of industries. The understanding and effective management of capital gains and associated tax implications are crucial for maintaining a company's profitability and ensuring regulatory compliance. Various strategies can be employed to mitigate the impact of capital gains tax, including strategic timing of asset sales, utilizing capital losses, considering tax-advantaged accounts, and making charitable donations. For companies with international operations, understanding the tax laws of foreign jurisdictions, treaty provisions, and double taxation avoidance mechanisms is essential. Lastly, accurate reporting, avoiding common pitfalls, and understanding the repercussions of non-compliance underline the importance of a robust capital gains tax strategy. Given the complexity and potential impacts, professional advice is often warranted to navigate this challenging landscape successfully.Capital Gains for Companies Overview

Understanding Capital Gains for Companies

Distinction Between Capital Gains and Ordinary Income

Assets Subject to Capital Gains Taxation

Holding Periods and Their Impact on Capital Gains Tax

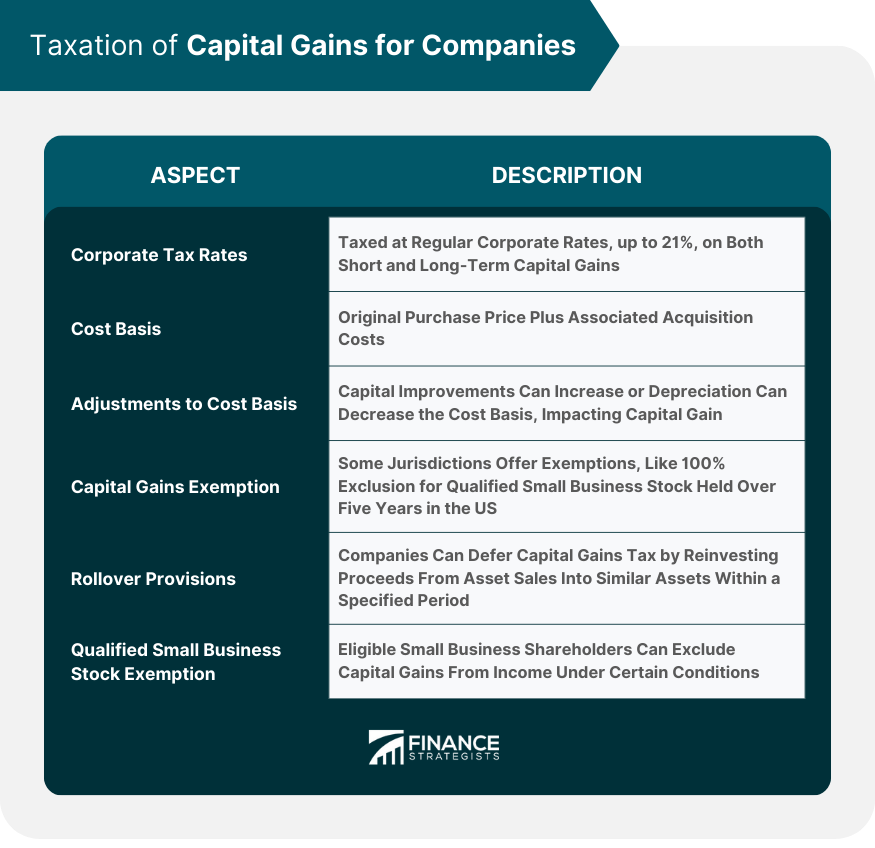

Taxation of Capital Gains for Companies

Corporate Tax Rates on Capital Gains

Calculation of Capital Gains for Companies

Determining the Cost Basis

Adjustments to the Cost Basis

Special Provisions and Exemptions

Capital Gains Exemption for Small Businesses

Rollover Provisions

Qualified Small Business Stock Exemption

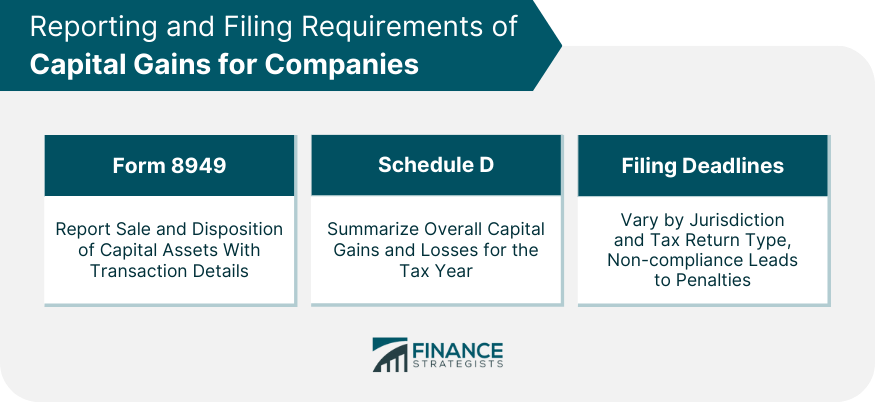

Reporting and Filing Requirements of Capital Gains for Companies

Form 8949: Sales and Other Dispositions of Capital Assets

Schedule D: Capital Gains and Losses

Deadlines for Filing Capital Gains Tax

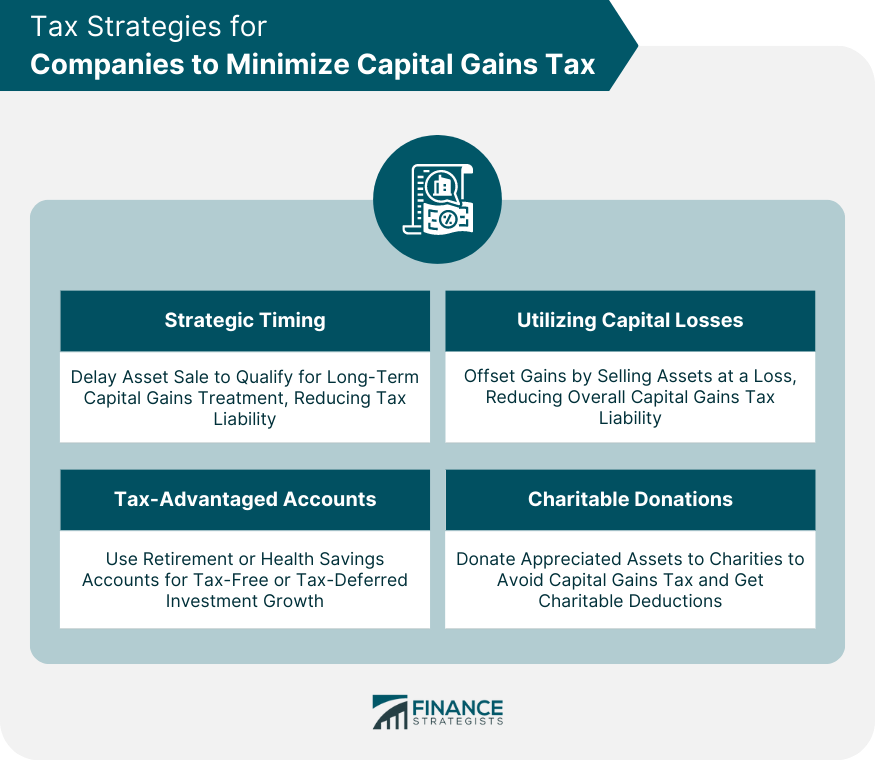

Tax Strategies for Companies to Minimize Capital Gains Tax

International Considerations of Capital Gains for Companies

Capital Gains Tax in Foreign Jurisdictions

Treaty Provisions and Impact on Cross-Border Capital Gains

Foreign Tax Credits and Double Taxation

Compliance and Avoiding Taxation Issues on Capital Gains for Companies

In serious cases, it could even lead to criminal charges. Therefore, it's essential for companies to maintain diligent record-keeping and seek professional advice when navigating complex tax issues.Bottom Line

Capital Gains for Companies FAQs

Ordinary income refers to earnings derived from a company's core business activities, such as sales revenue, services rendered, or other routine operations. Capital gains, on the other hand, result from the sale of a capital asset, like real estate, stocks, or equipment. These forms of income are taxed differently, with capital gains often taxed at lower rates.

The holding period, or the length of time a company holds an asset before selling it, can significantly influence the capital gains tax rate. Assets held for over a year often qualify for lower long-term capital gains tax rates, while those sold within a year of purchase are typically subject to higher short-term capital gains rates.

Strategies for minimizing capital gains tax include the strategic timing of asset sales, utilizing capital losses to offset gains, considering tax-advantaged accounts, and making charitable donations of appreciated assets.

Companies with foreign operations must account for capital gains tax laws in those jurisdictions. These laws can significantly impact the company's tax liability. Additionally, tax treaties between countries and foreign tax credits can affect the taxation of cross-border capital gains.

Non-compliance with capital gains tax laws can lead to penalties, including monetary fines and interest charges. In severe cases, it can even result in criminal charges. Therefore, it's crucial for companies to maintain accurate reporting and compliance with tax laws.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.