Intangible assets are those assets which have no physical substance but have future economic benefits based on rights or benefits accruing to the asset's owner. Intangible assets are noncurrent assets that have no physical properties. They generate revenues because they offer a firm value in future revenue production or exchange because of the right of ownership or use. However, there generally is a higher degree of uncertainty concerning the benefits generated from intangible assets than that concerning tangible assets. In addition, intangible assets are differentiated from nonphysical assets, such as accounts receivable or prepayments, because intangible assets are long-term in nature and contribute to the production or operating cycle of a business. Intangible assets generally are divided into two categories: those that are specifically identifiable and those that are not. Specifically identifiable intangible assets are those intangibles whose costs can easily be identified as part of the cost of the asset and whose benefits generally have a determinable life. Examples include patents, trade-marks, franchises, and leasehold. Conversely, intangibles that are not specifically identifiable represent some right or benefit that has an indeterminate life and whose cost is inherent in continuing business. The primary example of such an intangible is goodwill. While the term intangible could be used to describe all types of assets that lack physical form, it is used in accounting for dealing with certain operating assets. Accountants are not concerned with the lack of physical form of assets such as checking account balances, receivables, investments in securities, and prepaid expenses. Intangibles can be classified according to their identifiability and method of acquisition. That is, they are considered to be identifiable or unidentifiable and purchased or internally generated. The below example presents types of intangibles that fall into these various categories. Purchased identifiable intangible assets Purchased unidentifiable intangible assets Internally generated identifiable intangible assets Internally generated unidentifiable intangible assets The below example contains a list of the most common intangible assets. The accounting treatment of intangible assets parallels the accounting treatment of tangible noncurrent assets. Thus it is necessary to: Intangible assets arc originally recorded at cost. As with tangible assets, cost includes all the expenditures necessary to get the intangible asset ready for its intended use. Included in the acquisition cost are the purchase price and any fees. If an intangible asset such as a trademark or goodwill is acquired without a cost, it is not shown on the balance sheet. Subsequent valuation of intangibles is at net book value, that is, at cost less accumulated amortization to date. Because intangible assets are characterized by a lack of physical qualities, it is difficult to determine their existence, the value of their future benefits, and the life of these benefits. As a consequence, it is difficult to separate expenditures that are essentially operating expenses from those that give rise to intangible assets. For example, advertising and promotion campaigns and training programs provide future benefits to the firm. If this were not the case, firms would not spend millions of dollars on these programs that they do. However, it is extremely difficult to measure the amount and life of the benefits generated by these programs. As a result, expenditures for these and similar items are written off as an expense in the period incurred. When recurring expenditures are made for these items in approximately equal amounts, the effect on periodic income is not much different than if they were capitalized and then amortized over their estimated life. Research and development costs are expenditures incurred in discovering, planning, designing, and implementing a new product or process. Accounting for these costs has presented the accounting profession with significant problems. They clearly provide the firm with some future benefits. The billions of dollars spent by firms such as IBM result in new successful products but also in products that never reach the marketplace or are unsuccessful in the marketplace. Thus, it is difficult to measure the ultimate benefits that accrue from research and development expenditures that are made in 1982 but that may not result in a product until 1990. Furthermore, in today's highly competitive world economy, it is almost impossible to measure how long any of the benefits produced by research and development expenditures will last. The failure of IBM's PC Jr. is a good example of this. Because of these problems and the diversity of accounting practices that existed, the FASB now requires that all research and development costs be expensed in the period incurred. The above example listed some of the more common intangible assets. In the following section, we will outline the accounting for the more significant intangible assets. A patent is an exclusive right to use, manufacture, process, or sell a product that is granted by the U.S. Patent Office. Patents can either be purchased from the inventor or holder or be generated internally. When a patent is purchased from the inventor, its capitalized cost includes its acquisition cost and other incidental costs, such as legal fees. The legal costs of successfully defending a patent are also capitalized as part of its cost. If a patent results from successful research and development efforts, its cost is only the legal or other fees necessary to patent the invention, product, or process. This is because all the research and development costs expended to develop the patent, including those in the year the patent is obtained, must be written Off to expense in the period incurred. A patent has a legal life of 17 years. In many cases, however, its useful economic life is less than 17 years. As a result, patents should be amortized over their remaining legal life or economic life, whichever is shorter. For example, assume that a patent is purchased from its inventor for $240,000. At that time the patent has a remaining legal life of 10 years but has an estimated economic life of 8 years. In this case, the patent should be amortized on a straight-line basis over 8 years, with the following journal entry each year: Copyrights are the exclusive right of the creator or his or her heirs to reproduce and/or sell an artistic or published work. The copyright is granted by the U.S. government for the life of the creator plus 50 years. The cost to the creator of obtaining copyright from the government is the modest sum of $10. For this reason, the cost to the creator to obtain copyright is usually charged to an expense account when incurred. But when copyright is purchased by someone other than the creator, its cost may be substantial and should be capitalized. The capitalized cost should then be amortized over its remaining economic life, which is usually substantially shorter than its original legal life. A lease is a contractual agreement between the lessor (the owner of the property) and the lessee (the user of the property) that gives the lessee the right to use the lessor's property for a specific period of time in exchange for stipulated cash payments. The rights contained in this agreement usually are called leaseholds. Leases are classified into two types: operating leases and capital leases. Capital leases, which are complex financing arrangements. Operating leases usually require regular monthly payments by the lessee, but the lessor retains control and ownership of the property. The property or equipment always reverts to the lessor at the end of the lease term. Renting office space on a monthly or yearly basis is an example of an operating lease. Leases of this type do not result in a leasehold. The lessee records the lease by debiting Rent or Lease Expense and crediting Cash. The leased property remains on the books of the lessor. Some operating lease payments require the prepayment of the final month's rent. When this occurs, this payment is classified as a prepaid expense and remaining on the books until the lease is terminated. Leases may require a lump-sum rental payment that represents additional rent over the life of the lease. This is usually a significant amount in relation to the monthly payment and should be written off over the life of the lease. These are the improvements made by the lessee to the leased property. They consist of such items as air conditioning, partitioning, and elevators. These improvements are permanent in nature and become the property of the lessor when the leased property reverts to the lessor at the termination of the operating lease. These expenditures should be recorded in an asset account called Leasehold Improvements and amortized over the shorter of their useful life or the remaining term of the lease. A franchise is a right to use a formula, design, or technique or the right to conduct business in a certain territory. Franchises can be granted by either a business enterprise or a governmental unit. Many businesses, such as fast-food restaurants and convenience markets, are operated as franchises. For example, the parent company of 7—Eleven Markets sells franchises to individual owner-operators. Cities and municipalities also often grant franchises, such as taxi franchise that allows a company to operate in a specified territory for a designated period of time. If the cost of a franchise is substantial, it should be capitalized and amortized over its useful life, not to exceed 40 years. If the cost is insignificant, the expenditure can be treated as an expense and immediately written off. Goodwill has a specific meaning in accounting. It represents the value today of the excess earnings of a particular enterprise. Excess earnings represent earnings above the normal earnings of an industry. That is, the firm is able to earn a rate of return on its recorded net assets above the industry average rate of return. These excess earnings are the result of a number of factors, including superior management, well-trained employees, good location, monopolies, and manufacturing efficiencies. Unlike the other intangible assets we have discussed, goodwill is not specifically identifiable and is not separable from the firm. Thus, goodwill can be recorded only when purchased. The existence of internally generated goodwill is verified only when a firm is purchased by another party, and it is at that time that the goodwill, if any, is recorded. To illustrate the concept of goodwill, assume that a group of investors purchased an electronic components manufacturing business. At the time of the purchase, the fair market value of the firm's net assets totaled $1 million and consisted of the following: The agreed purchase price is $1,250,000; this implies goodwill of $250,000, or the purchase price of $1,250,000 less the identifiable net assets acquired of $1 million. The entry to record the purchase is: As this Journal entry shows, the purchase price is first allocated to the identifiable net assets based on their fair market value. Any remaining portion is considered goodwill and is recorded by debit to the Goodwill account. Subsequently, goodwill is amortized over a period not exceeding 40 years.What Are Intangible Assets? - Definition

Explanation

Types of Intangible Assets

Example

Purchased intangible assets

Internally generated intangible assets

Common Intangible Assets

Type of Intangible Assets

Description

Specifically Identifiable

Patent

An exclusive right to use, manufacture, process, or sell a product granted by the U.S. Patent Office. Patents have a legal life of 17 years; however, their economic life may be shorter.

Copyright

The exclusive right of the creator or heirs to reproduce and/or sell an artistic or published work. Granted by the U.S. government for the period of the life of the creator plus 50 years.

Leaseholds

A contractual agreement between a lessor (owner of the property) and a lessee (user of the property) that gives the lessee the right to use the lessor's property for a specific period of time in exchange for cash payments.

Leasehold Improvements

Improvements that are made by the lessee that at the end of the lease term revert to the ownership of the lessor.

Trademark and Trade Name

A symbol or name that allows the holder to use it to identify or name a specific product or service. A legal registration system allows for an indefinite number of 20-year renewals.

Organization Cost

Costs incurred in the creation of a corporation, including legal fees, registration fees, and fees to underwriters.

Franchise

An exclusive right to use a formula, design, technique, or territory.

Not Specifically Identifiable

Goodwill

The present value of expected excess earnings of a business above the average industry earnings. Recorded only when a business is purchased at a price above the market value of the individual net assets of the business.

Accounting problems related to Intangible Assets

(1) measure and capitalize their acquisition cost;

(2) amortize their cost over the shorter of their legal life, if any, or their economic life (in no case can the amortization period exceed 40 years); and

(3) account for any gain or loss on their disposition.Determining Acquisition Cost

Operating Expenses and Intangible Assets

Research and Development Costs

Accounting for specific intangible assets

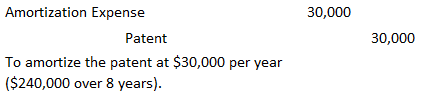

Patents

Copyrights

Leaseholds and Leasehold Improvements

Leasehold improvements

Franchises

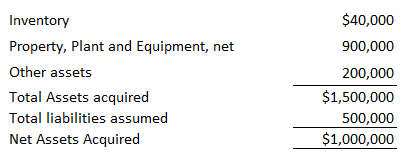

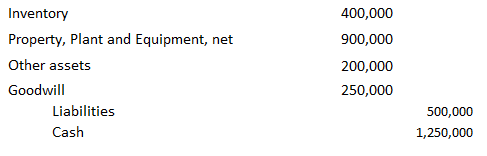

Goodwill

Intangible Assets FAQs

Intangible assets are non-physical assets that have long-term value to a company, such as patents, copyrights, trademarks, and customer relationships.

An intangible asset can be identified by its likelihood to generate future economic benefits, its ability to be separated from the entity (i.e., sold or transferred), and its useful life which is greater than one year.

The most commonly found intangible assets include patents, copyrights, trademarks, trade secrets, customer relationships, brand recognition and goodwill.

Intangible assets are valued based on their expected future economic benefits, the cost to acquire or develop them, or the going market rate for similar assets.

Tangible assets are physical assets such as land, buildings, and equipment. Intangible assets are non-physical assets that have long-term value to a company, such as patents, copyrights, trademarks, customer relationships, brand recognition, and goodwill. Tangible assets can be depreciated over time while intangible assets cannot.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.