Capital gains and losses arise from the sale or disposition of assets, especially investments like stocks, bonds, and real estate. When an asset is sold for more than its purchase price, a capital gain is realized; conversely, when it's sold for less, a capital loss is incurred. These gains and losses can be classified as either short-term or long-term, depending on the holding period. Typically, assets held for one year or less result in short-term gains or losses, while assets held for more than a year yield long-term gains or losses. The distinction is important as they are often taxed at different rates. In many tax jurisdictions, long-term capital gains receive preferential tax rates compared to short-term gains. On the other hand, capital losses can offset gains, and any excess loss might be deductible against other forms of income, subject to specific limits and regulations. Capital gains arise when you sell a capital asset—such as stocks, bonds, precious metals, real estate, and collectibles—for more than its purchase price. This profit, known as the capital gain, is an essential element in investment and tax strategies. It's worth noting that a capital gain is only realized when the asset is sold. Merely seeing an increase in the value of your assets on paper does not constitute a capital gain until the asset is sold and the gain becomes a realized income. Capital gains are segmented into two types based on the length of time you've held the asset before selling it: short-term and long-term. Short-term capital gains are profits from the sale of assets held for a year or less. They're typically taxed as ordinary income, which means they can be subject to higher tax rates compared to long-term capital gains. Long-term capital gains are profits resulting from the sale of assets held for more than a year. These gains are generally taxed at a lower rate than short-term gains, which incentivizes investors to hold onto investments longer for financial benefit. The taxation rates for capital gains are contingent on your taxable income and the length of time you've held the asset. Short-term capital gains are taxed at the individual's ordinary income tax rate, which can be as high as 37% depending on the tax bracket. In contrast, long-term capital gains are typically taxed at 0%, 15%, or 20%, depending on your taxable income. This difference in rates can significantly impact your net investment returns. A capital loss occurs when you sell a capital asset for less than its original purchase price. This loss can have significant implications for your tax situation. Just like capital gains, a capital loss is only realized once the asset is sold. Until that point, any decrease in the value of an asset is only a potential loss. A benefit of capital losses is their ability to offset capital gains. If your capital losses exceed your capital gains, you can use the excess loss to offset other income on your tax return. This can be a strategic way to lower your taxable income and potentially drop into a lower tax bracket. Capital losses can help reduce your taxable income. If the total net capital loss is more than the yearly limit on capital loss deductions, you have the option to carry the unused part forward to future years until it's entirely used up. This carry forward option can be strategically beneficial, allowing you to offset gains in future years. Capital gains are determined by subtracting the purchase price of the asset, known as the basis, from the sale price. If you've made improvements to the asset—like home renovations—those costs can be added to the basis, which can reduce the taxable gain. This is why keeping detailed records of such improvements is critical. The holding period—the length of time you retain an asset—plays a significant role in the capital gains tax rate that will be applied. Assets held for over a year may qualify for the more favorable long-term capital gains tax rate. Therefore, considering your holding period before selling an asset can help in tax planning. Certain types of assets have special rules: Real Estate: The sale of a primary residence might qualify for an exclusion of up to $250,000 for single filers or $500,000 for married couples filing jointly, as long as specific conditions are met. Collectibles: The sale of collectibles like art, antiques, and precious metals might be subject to a higher long-term capital gains tax rate. Therefore, collectors need to consider these tax implications when buying or selling these items. Qualified Small Business Stock: A portion of the gain on the sale of qualified small business stock may be excluded from gross income if specific conditions are met. This benefit can be a great incentive for investing in small businesses. Capital losses, much like capital gains, are determined by subtracting the sale price of the asset from the basis. If the result is negative, you have a capital loss. Keeping accurate records of your transactions can help ensure you calculate these losses correctly. According to IRS rules, if your capital losses exceed your capital gains, you can use the loss to offset up to $3,000 of other income. If your total net capital loss is more than this limit, you can carry the loss forward to future years. This rule provides an opportunity to offset gains in future years and potentially lower your tax liability. The IRS permits taxpayers to carry forward unused capital losses indefinitely until they are entirely used up. However, carrying back losses—applying them to previous years' returns—is typically not allowed except in specific situations like a farming loss or a casualty or theft loss. Understanding these rules can be vital in developing a long-term tax strategy. Tax-loss harvesting involves selling securities at a loss to offset a capital gains tax liability. It is commonly used to limit the recognition of short-term capital gains. This strategy can be particularly beneficial in years when you have substantial capital gains, allowing you to reduce your tax liability. As long-term capital gains are generally taxed at a lower rate than short-term gains, holding onto investments for over a year before selling can result in tax savings. Therefore, considering your investment timeline and potential tax implications before selling can lead to significant benefits. Gifts and inheritances can be excellent strategies for avoiding capital gains tax. In most cases, the recipient of a gift or inheritance takes on the giver's basis. This stepped-up basis rule means the beneficiary's potential capital gains tax is minimized when they sell the asset. This can be a powerful way to transfer wealth while minimizing tax implications. Capital gains and losses are intrinsic facets of investing, playing pivotal roles in tax strategies. Realized when assets like stocks or real estate are sold, these gains and losses significantly influence the tax liabilities of an individual. The duration for which an asset is held determines its classification as short-term or long-term, each having distinct tax implications. While long-term gains often benefit from preferential tax rates, capital losses can strategically offset gains and further income, offering potential tax reductions. Special considerations exist for assets like real estate, collectibles, and small business stocks, underscoring the need for meticulous planning. Methods such as tax-loss harvesting, prolonged investment holding, and adept gift and inheritance planning can mitigate tax liabilities. Given the complexity and potential financial implications of capital gains tax, it's paramount to navigate it wisely. To optimize your investment returns and minimize tax-related challenges, consider seeking specialized tax planning services.Overview of Capital Gains and Losses

Understanding Capital Gains

What Are Capital Gains?

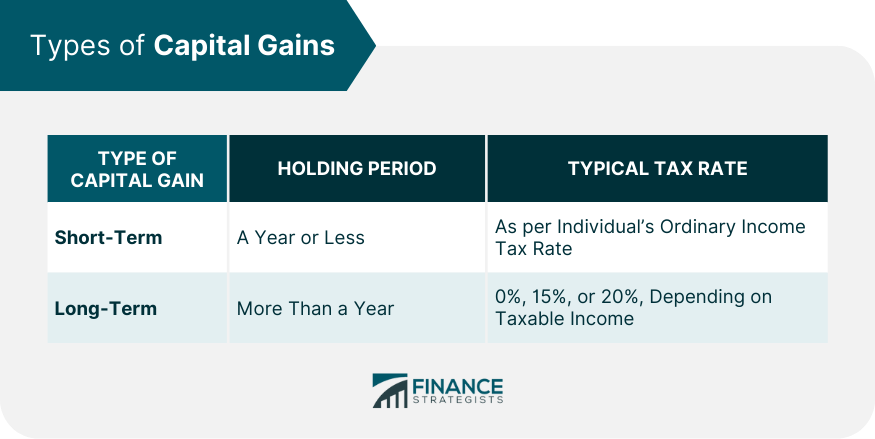

Types of Capital Gains

Taxing Capital Gains

Understanding Capital Losses

What Are Capital Losses?

Offsetting Capital Gains With Capital Losses

Tax Implications of Capital Losses

Navigating Capital Gains Tax

Calculating Capital Gains

Holding Period and Capital Gains Tax

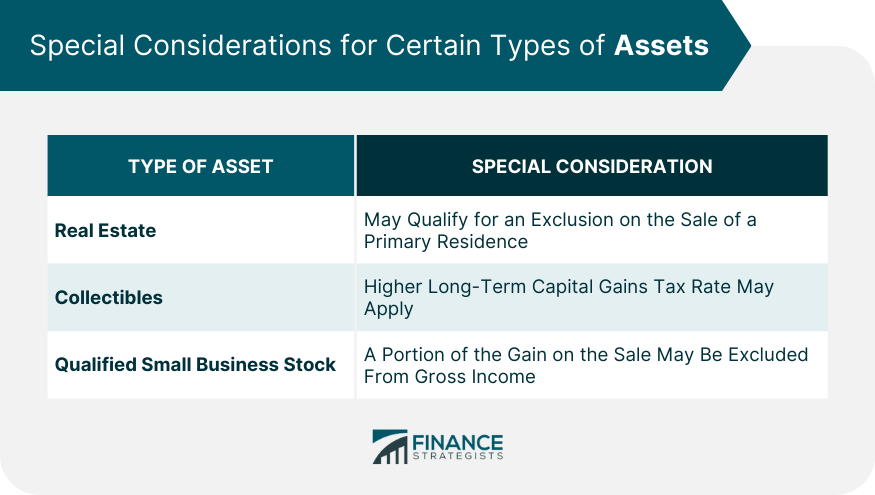

Special Considerations

Exploring Capital Loss Deduction

Calculating Capital Losses

Limits on Capital Loss Deductions

Carrying Forward and Backward Capital Losses

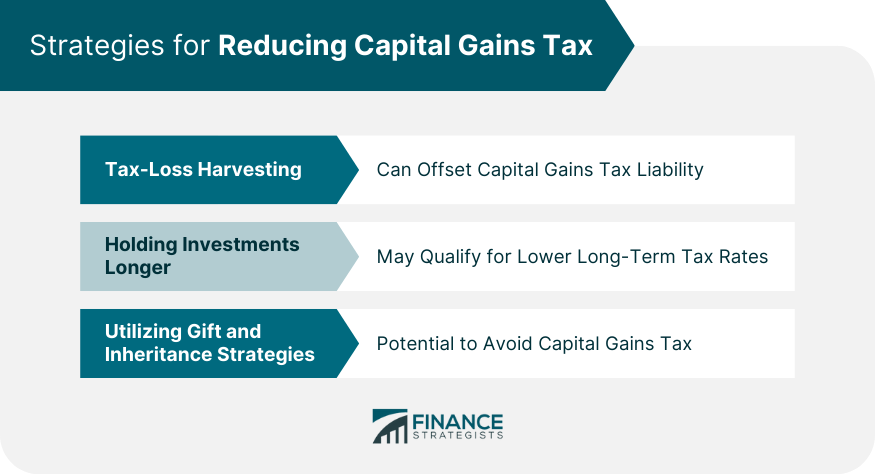

Strategies for Reducing Capital Gains Tax

Tax-Loss Harvesting

Holding Investments Longer

Utilizing Gift and Inheritance Strategies

Final Thoughts

Capital Gains and Losses FAQs

Capital gains are profits from selling assets like stocks or real estate for more than their purchase price. Capital losses occur when assets sell for less than their cost.

Capital gains are taxed based on how long the asset was held before selling. Short-term gains (assets held for a year or less) are taxed as ordinary income, while long-term gains (assets held over a year) are generally taxed at lower rates.

Capital losses can offset capital gains, reducing your taxable income. If your losses exceed your gains, you can deduct the excess from other income or carry it forward to future years.

Strategies include tax-loss harvesting, holding investments for over a year to qualify for lower long-term tax rates, and using gift and inheritance rules to avoid capital gains tax.

Yes, special rules apply for real estate, collectibles, and qualified small business stock. These rules can affect the calculation of capital gains and the applicable tax rates.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.