Capital Gains Tax for Non-US Residents refers to the tax imposed on profits made by foreign individuals or entities from the sale of assets in the United States. Non-resident aliens are subject to this tax if they meet certain conditions, including the substantial presence test or holding a U.S. green card. The tax applies to gains from various assets such as stocks, real estate, and bonds, but exemptions exist under specific circumstances, like tax treaties and non-effectively connected income. Short-term capital gains are usually taxed at a flat rate, while long-term gains may be exempt unless associated with a U.S. trade or business. Proper tax planning, timing of sales, and understanding tax treaties can help minimize the impact of Capital Gains Tax for Non-US Residents and ensure compliance with U.S. tax laws. The Green Card test is one method the IRS uses to determine a person's tax residency. Under this test, an individual is considered a U.S. resident for tax purposes if they are a lawful permanent resident of the United States at any time during the calendar year. The Substantial Presence Test is another method used by the IRS. It calculates the number of days an individual was present in the U.S. during a three-year period, considering 100% of the days in the current year, 1/3 of the days in the first preceding year, and 1/6 of the days in the second preceding year. If the sum equals or exceeds 183 days, the individual is a U.S. tax resident. The U.S. has tax treaties with many countries, providing benefits like reduced tax rates or exemptions for residents of these countries. These treaties aim to avoid double taxation and promote economic cooperation. FIRPTA subjects foreign persons to U.S. income tax on the disposition of U.S. real property interests. While it might sound burdensome, certain exemptions can minimize or even eliminate the tax. Non-U.S. residents are typically only taxed on U.S. source income that is "effectively connected" with a U.S. trade or business. This income is taxed at the same graduated rates applicable to U.S. residents. Short-Term Capital Gains: These are calculated similarly to U.S. residents. They are taxed as ordinary income, and the rate depends on the taxpayer's income bracket. Long-Term Capital Gains: These are profits on assets held for more than a year. For non-US residents, these gains are typically subject to a flat 30% tax unless a tax treaty specifies a lower rate. Tax Rates for Non-US Residents: Tax rates applicable to non-US residents vary, often depending on tax treaties. Generally, a 30% rate is applied to U.S.-sourced income unless a lower treaty rate applies. Filing US Tax Returns: Non-US residents with U.S. source income must generally file a U.S. tax return. Form 1040NR or 1040NR-EZ is used, depending on the taxpayer's circumstances. Use of Individual Taxpayer Identification Number (ITIN): An ITIN is required for non-U.S. residents who do not qualify for a social security number but have tax filing obligations in the U.S. A non-resident alien spouse may choose to be treated as a U.S. resident for tax purposes, which can lead to a lower combined tax liability. Dual status aliens are taxed differently for the portion of the year they are considered residents and the portion they are considered non-residents. This can add complexity to their U.S. tax filing. Non-resident aliens engaged in a U.S. trade or business are subject to U.S. tax on income that is effectively connected with that trade or business. Non-U.S. residents may be subject to U.S. estate and gift tax on certain U.S. situated assets, which requires careful tax planning. Totalization Agreements aim to avoid double taxation of income with respect to social security taxes. These agreements can impact how and where non-US residents are taxed. Tax treaties may provide avenues for non-US residents to minimize their U.S. tax liability, including Capital Gains Tax. Taxpayers should explore these options when planning their investments. The timing of an asset sale can significantly impact the capital gains tax liability. Long-term gains are typically taxed at a lower rate than short-term gains, so holding assets for at least one year can provide tax benefits. Whether income is effectively connected with a U.S. trade or business can affect tax rates. Non-US residents should consider this in their tax planning. Tax rules can vary significantly based on the taxpayer's individual circumstances and the country of their tax residence. Non-US residents should not assume the tax rules that apply to one person will apply to them. Some non-US residents might believe they're exempt from U.S. capital gains tax, which is incorrect. Non-US residents are often subject to U.S. taxes on U.S. sourced income, including capital gains. Many non-US residents misinterpret tax treaty benefits, assuming they provide complete tax exemption. While treaties may reduce tax rates or provide certain benefits, they do not typically eliminate all U.S. tax liability. Capital Gains Tax for Non-US Residents is a crucial aspect of taxation for foreign individuals and entities engaging in asset sales within the United States. Non-resident aliens are subject to this tax if they meet certain criteria, including the substantial presence test or holding a U.S. green card. The tax applies to gains from various assets, such as stocks, real estate, and bonds, but exemptions exist under specific circumstances, including tax treaties and non-effectively connected income. Short-term capital gains are typically taxed at a flat rate, while long-term gains may be exempt unless associated with a U.S. trade or business. Proper tax planning, strategic timing of sales, and a thorough understanding of tax treaties can help minimize the impact of Capital Gains Tax for Non-US Residents and ensure compliance with U.S. tax laws. Overall, seeking professional advice and planning ahead is essential for optimizing tax outcomes in this complex area of taxation.Capital Gains Tax for Non-US Residents Overview

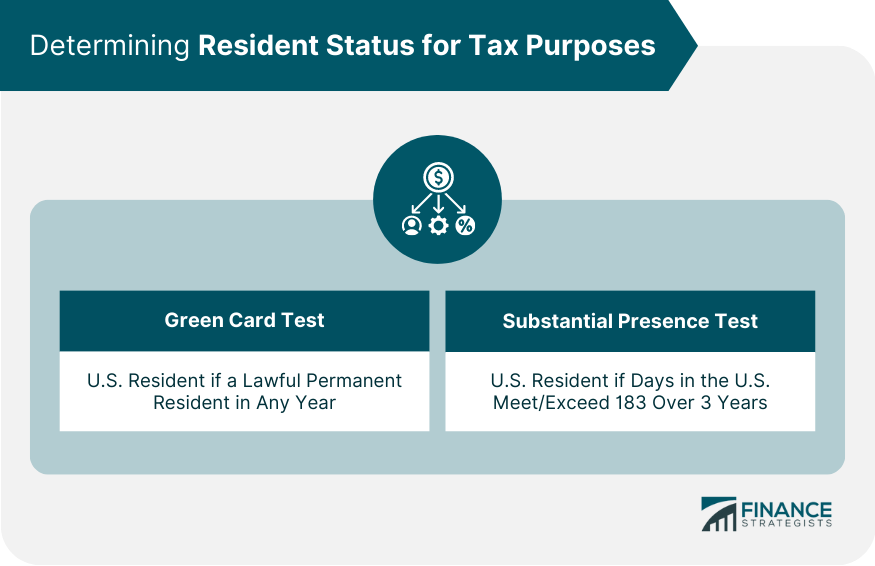

Determining Resident Status for Tax Purposes

Green Card Test

Substantial Presence Test

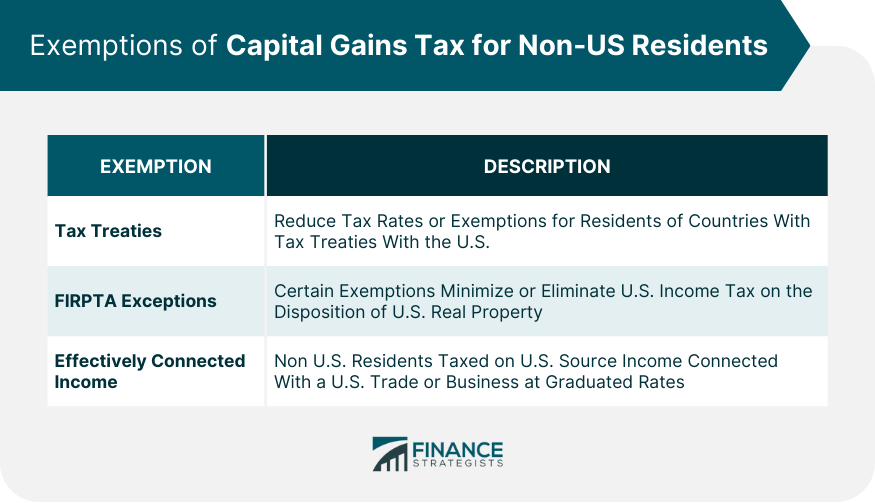

Exemptions of Capital Gains Tax for Non-US Residents

Tax Treaties

Foreign Investment in Real Property Tax Act (FIRPTA)

Effectively Connected Income

Calculation of Capital Gains Tax for Non-US Residents

Reporting and Paying Capital Gains Tax

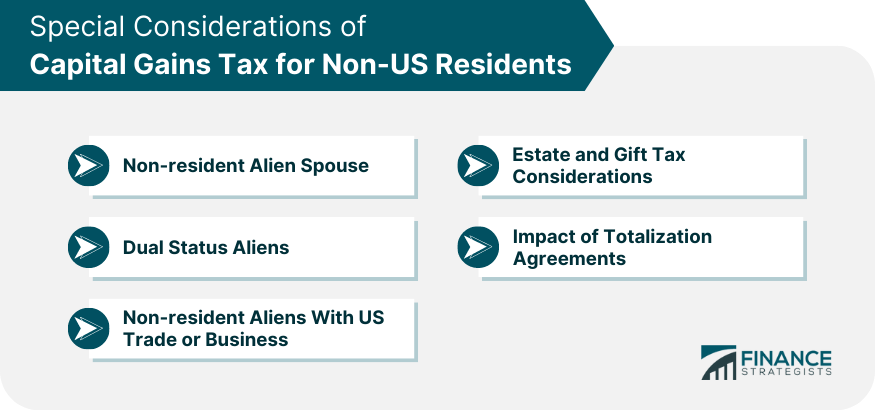

Special Considerations of Capital Gains Tax for Non-US Residents

Non-resident Alien Spouse

Dual Status Aliens

Non-resident Aliens With US Trade or Business

Estate and Gift Tax Considerations

Impact of Totalization Agreements

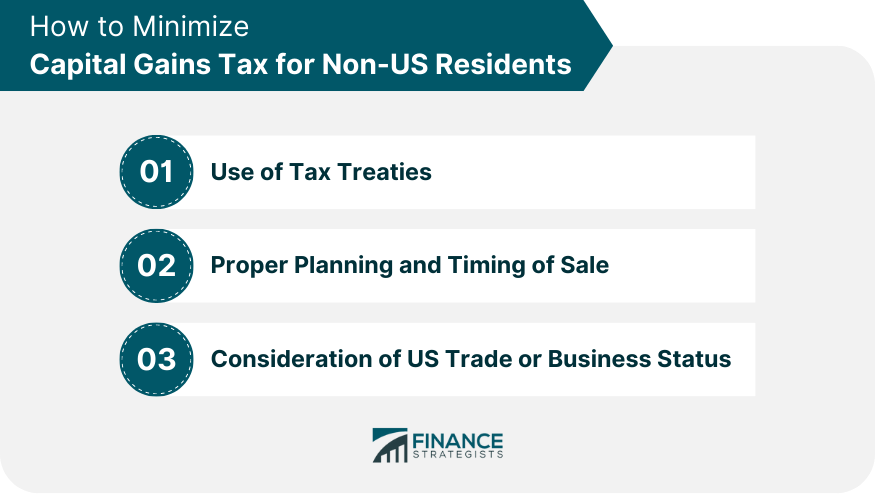

How to Minimize Capital Gains Tax for Non-US Residents

Use of Tax Treaties

Proper Planning and Timing of Sale

Consideration of US Trade or Business Status

Common Misconceptions About Capital Gains Tax for Non-US Residents

All Non-US Residents Are Taxed the Same

Non-US Residents Are Not Subject to Capital Gains Tax

Misinterpretation of Tax Treaty Benefits

Conclusion

Capital Gains Tax for Non-US Residents FAQs

Capital Gains Tax (CGT) is a levy paid on the profit realized from the sale of assets like stocks, bonds, or property. The "capital gain" is the difference between the purchase price and the selling price of an asset.

Non-US residents are generally subject to U.S. Capital Gains Tax on U.S. sourced income, such as from the sale of U.S. real estate or, in some cases, U.S. stocks and securities. The tax rates can vary based on various factors, including tax treaties between the U.S. and the resident's home country.

Short-term capital gains are from assets held for one year or less and are taxed as ordinary income. Long-term capital gains are from assets held for more than one year and are generally taxed at a lower rate.

Tax treaties are agreements between two countries to avoid double taxation and promote economic cooperation. For non-US residents, these treaties can provide benefits like reduced tax rates or exemptions on certain types of income, including capital gains.

FIRPTA, the Foreign Investment in Real Property Tax Act, subjects foreign persons to U.S. income tax on the sale of U.S. real property interests. While it may initially seem burdensome, certain exceptions and provisions can help minimize or even eliminate the tax liability under FIRPTA.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.