Capital gains refers to the appreciation in the value of an asset over its acquisition cost, resulting in a profit when the asset is sold. In the context of "gifted property," it pertains to real estate that has been transferred from one individual to another without any financial exchange or compensation. The purpose of understanding capital gains on such properties is to determine potential tax implications. When the recipient of the gifted property sells it, they may incur capital gains tax based on the property's appreciated value from the original donor's purchase price. This tax implication arises because the receiver often inherits the donor's original cost basis, unlike inherited properties that typically assume a stepped-up basis. Grasping these nuances ensures compliance with tax regulations and aids in informed financial decision-making. Upon receiving a gifted property, it's crucial to understand its basis. The basis determines the amount of capital gains when the property is eventually sold. Typically, the receiver of the gift inherits the donor's original cost basis. This is opposed to an inherited property, where the basis often aligns with the Fair Market Value at the time of the original owner's passing. When you receive a gifted property and decide to sell it later, you might incur a capital gains tax based on the property's appreciated value. This potential tax liability hinges on the difference between the property's selling price and its original or adjusted basis. The carryover basis is a tax provision that allows the recipient of a gift to adopt the donor's original cost basis. This can be both beneficial or disadvantageous depending on the original purchase price and the current market value. Apart from the original cost, any gift tax paid on the property also affects the adjusted basis. For instance, if the donor paid a gift tax during the transfer, this amount could increase the property's adjusted basis, potentially reducing future capital gains when the property is sold. To determine the capital gains on a gifted property, subtract the adjusted basis (original cost plus any adjustments like improvements or gift taxes paid) from the sale price. The resulting amount represents your capital gains. The duration you hold onto a gifted property before selling it plays a significant role in tax implications. If the combined holding period (considering both the donor's and donee's ownership duration) is less than a year, it's termed as short-term. Conversely, if held for more than a year, it's considered long-term, often leading to favorable tax rates. Short-term capital gains are typically taxed at the individual's ordinary income tax rate. These rates can be significantly higher than long-term capital gains rates, making short-term sales less tax-efficient. For many taxpayers, long-term capital gains benefit from lower tax rates. Depending on your taxable income, these rates can be significantly reduced, offering incentives to hold onto assets for extended periods. The holding period directly influences whether gains are classified as short or long-term. Longer holding periods often translate to reduced tax liabilities due to the preferential rates for long-term gains. Certain situations, such as selling your primary residence, may allow you to exclude a portion of the capital gains from taxes. Familiarizing oneself with available deductions and exclusions can significantly reduce tax obligations. If a gifted property's market value at the time of gifting is less than the donor's original cost basis, special rules apply. In such scenarios, for the purpose of determining a loss, the recipient's basis is the property's fair market value at the time of the gift. Gifting a property with an existing mortgage can lead to unanticipated tax consequences. The remaining mortgage value might be considered taxable income, leading to potential gift tax implications. Generally, gifts between spouses are exempt from gift taxes. This means that properties gifted between spouses often carry over the original basis without immediate tax consequences. While similar in nature, gifted properties and inherited properties have distinct tax implications. Unlike gifted properties, inherited ones typically take on a stepped-up basis, equating to the property's fair market value at the time of the donor's death. If a gifted property becomes your primary residence and you live in it for at least two of the five years before selling, you might qualify for a sizable exclusion on capital gains. While gifting can be a generous gesture, it might not always be the most tax-efficient. Comparing the tax consequences of gifting versus leaving a property as an inheritance can guide optimal decision-making. Timing, the sale of a gifted property can influence the tax consequences. By considering market conditions, personal financial situations, and potential tax law changes, you can strategize the best time to sell. Maintaining thorough records of the gifted property, including the original purchase agreement, any improvements made, and gift tax returns, is vital. These documents provide the necessary evidence to validate your tax claims. Receipts of property-related expenses, documentation of gift tax payments, and any other relevant financial documents can support your claims on the property's adjusted basis. During the property's sale, it's crucial to retain all transaction-related records, including the sale agreement, property advertisements, and related correspondence. This documentation can be invaluable during potential tax audits. Understanding capital gains on a gifted property is crucial for making informed financial decisions and ensuring tax compliance. Unlike inherited properties, which often assume a stepped-up basis, gifted properties typically carry the donor's original cost basis. This distinction can significantly impact potential capital gains tax when the property is sold. Key factors to consider include the original and adjusted basis, holding period, and the nuanced tax rates associated with short-term versus long-term capital gains. Additionally, strategic planning, such as utilizing the primary residence exclusion or comparing gifting versus inheritance, can offer tax efficiencies. Thorough documentation is essential, not just for calculating potential gains but also for safeguarding against future tax queries. Knowledge of these facets provides individuals with a roadmap to navigate the complex terrain of gifted property transactions.Overview of Capital Gains on a Gifted Property

Immediate Impact of Receiving a Gifted Property

Basis of the Gifted Property

Implications for the Receiver

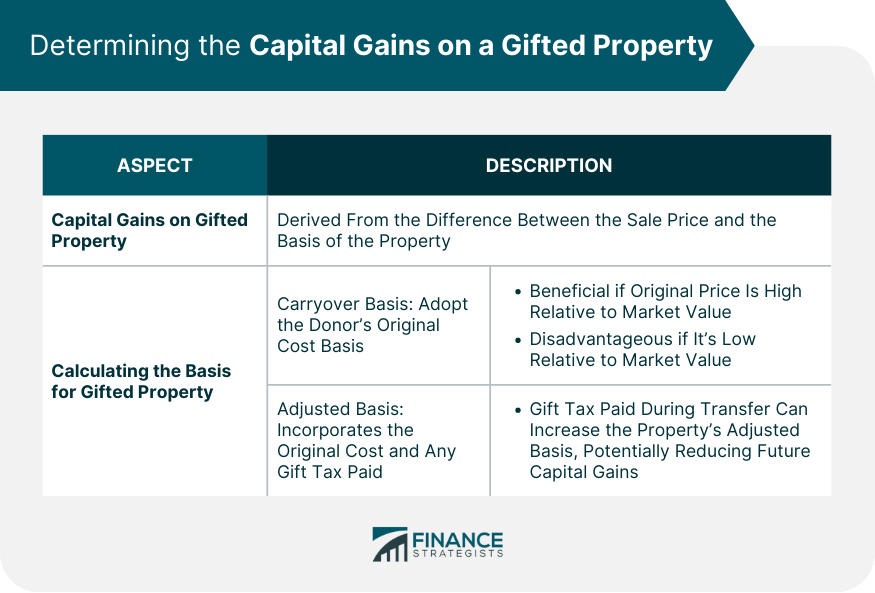

Determining the Capital Gains on a Gifted Property

Calculating the Basis for Gifted Property

Carryover Basis: When the Donor’s Basis Becomes the Donee’s

Adjusted Basis: Consideration of Any Gift Tax Paid

Sale of Gifted Property

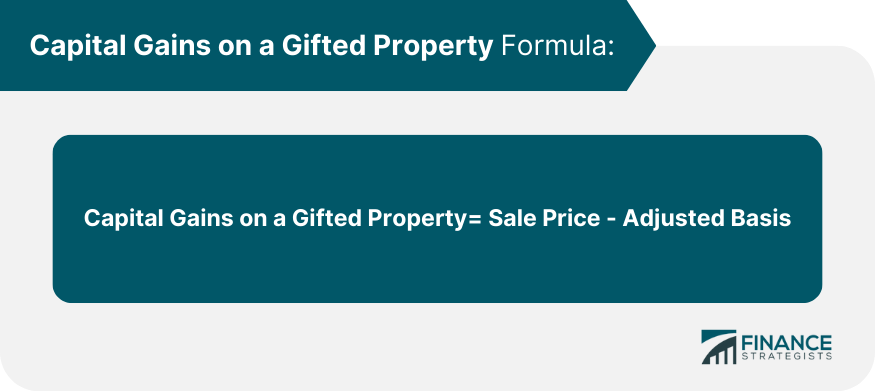

Calculating Capital Gains

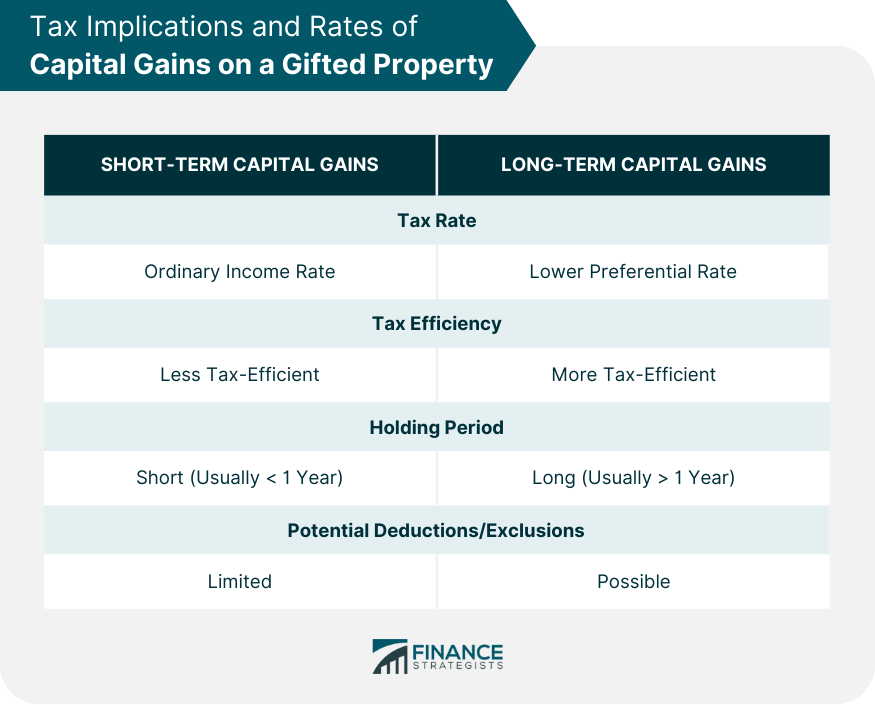

Determining Holding Period

Tax Implications and Rates of Capital Gains on a Gifted Property

Tax Rates for Short-Term Capital Gains

Tax Rates for Long-Term Capital Gains

Effect of the Holding Period on Tax Rates

Potential Deductions and Exclusions

Special Considerations and Exceptions of Capital Gains on a Gifted Property

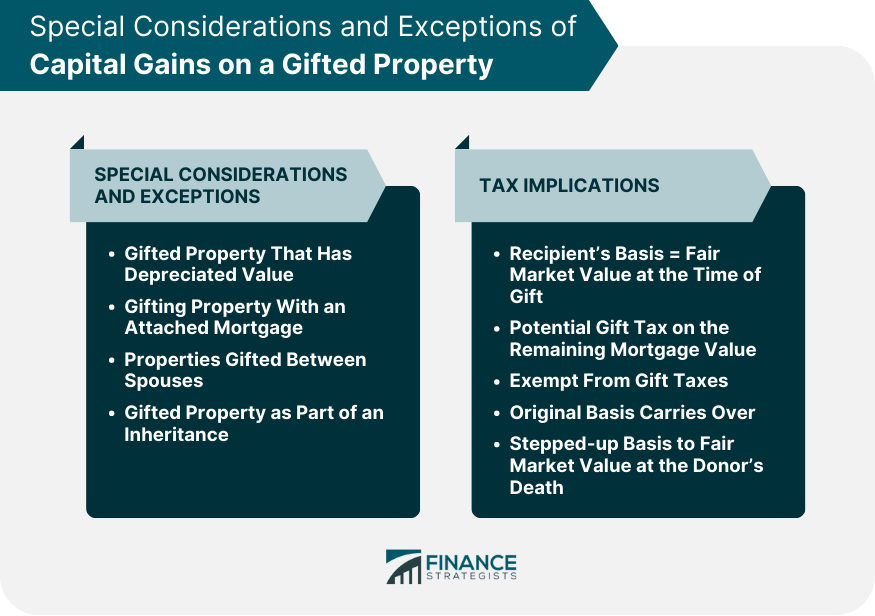

Gifted Property That Has Depreciated in Value

Impact of Gifting a Property With an Attached Mortgage

Implications for Properties Gifted Between Spouses

Gifted Property as Part of an Inheritance

Planning and Strategies to Minimize Capital Gains Tax

Utilizing the Primary Residence Exclusion

Tax Implications of Gifting vs Inheriting

Strategic Timing of the Sale

Documentation and Record-Keeping of Capital Gains on a Gifted Property

Importance of Keeping Records Related to the Gifted Property

Documents That Can Substantiate the Original and Adjusted Basis

Importance of Documentation During the Sale Process

Conclusion

Capital Gains on a Gifted Property FAQs

The basis of a gifted property is typically the donor's original cost basis, known as the carryover basis. In contrast, an inherited property's basis is often its Fair Market Value at the time of the original owner's passing, termed the stepped-up basis.

The classification hinges on the combined holding period, considering both the donor's and the donee's ownership durations. If the property is held for less than a year before selling, it's short-term. If held for more than a year, it's long-term.

Yes, generally, gifts between spouses are exempt from gift taxes. This means the receiver often inherits the original basis of the property without immediate tax implications.

It's crucial to maintain documents like the original purchase agreement, records of any property improvements, gift tax returns, and any other relevant financial documents. This documentation is essential for calculating capital gains and for potential tax audits.

Potentially, yes. If the gifted property becomes your primary residence and you've lived in it for at least two of the five years preceding its sale, you might qualify for an exclusion on capital gains.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.