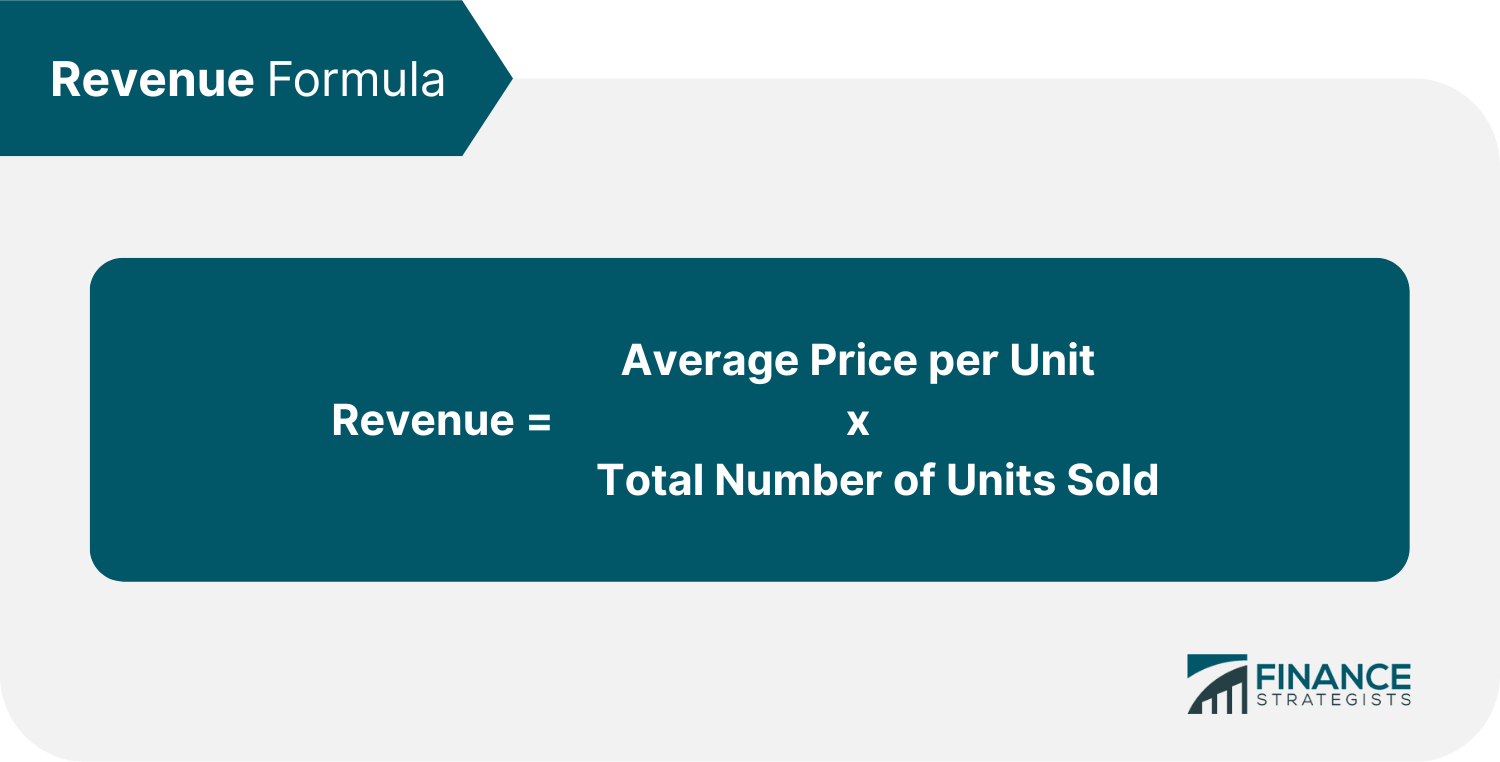

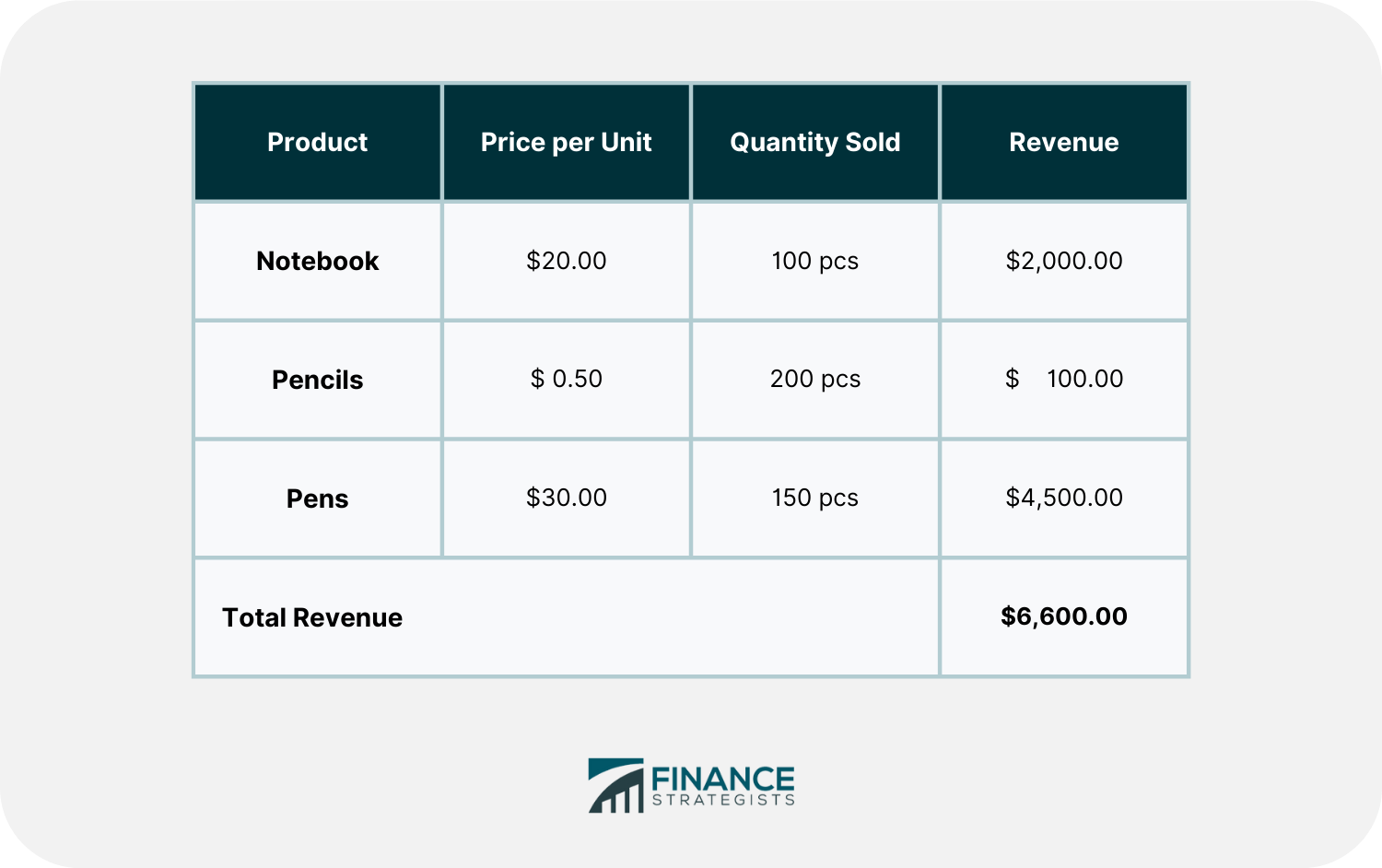

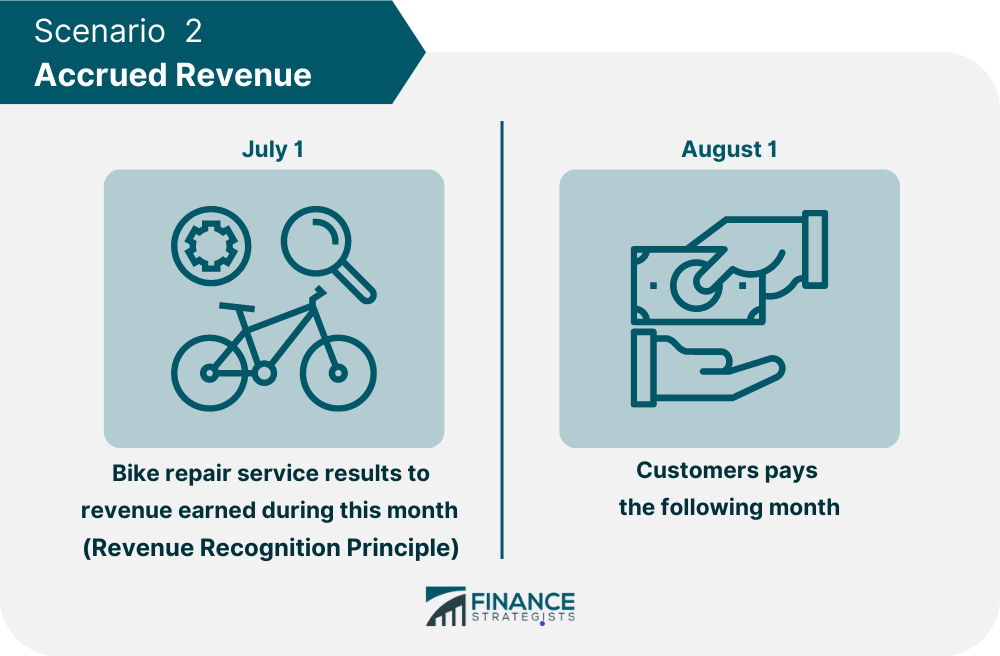

Revenue is the amount of money a company receives from its primary business activities, such as sales of products and services. A company's revenue does not take any expenses into account. After subtracting expenses from the revenue figure, what is left is profits or income. A company's revenue is an essential component of many financial metrics used to assess whether a company is a good investment. For example, when a company releases its financials for each quarter, the financial media reports whether revenue and earnings per share (EPS) are above or below expectations. If the numbers are higher than expected, it is termed a "beat" and often leads to a jump in the stock price. When the numbers are lower, it is called a "miss" and often causes the stock price to drop. However, revenue growth can be even more important than the revenue number itself. When revenue is growing year-over-year, it implies that the company is expanding by gaining market share, increasing its offerings, or improving its operations. Companies get revenue in many different ways, but the easiest one to understand is the sales of products or services. For companies generating revenue from product sales, revenue is calculated by multiplying the average price for each unit by the total number of units sold. For instance, if a company sells 100 lipsticks at a price of $50 each, the total revenue would be $5,000. Revenue = $50 x 100 = $5,000 Companies that may have diverse products or services and different prices for each should calculate their revenue for each product or service and then add everything together to have the total revenue. For instance, a school supply shop sells different products like notebooks, pencils, and pens at different prices. They sell 100 notebooks at $20 each, 200 pencils at $0.50 each, and 150 pens at $30 each. The total revenue of the supply shop is $6,600, after adding the revenue on each of the products sold. It is possible for a company to have a lot of revenue but still not make any profits if expenses exceed its revenue. That is why it is essential to take a company's expenses into account when analyzing its financials. Although there are many different types of revenue, in general, it can be classified into two main types: operating revenue and non-operating revenue. Operating revenue is earned through the main operations of a business. Activities that generate operating revenue are directly related to the primary line of the business. For example, a manufacturing company earns revenue from selling its products, or a consulting firm earns revenue from the professional fees it charges for its services. From the example we had above, operating revenue is the income derived from the sales of lipsticks and school supplies. Operating revenue is critical in any business as it is the main source of income for a business. It is a valuable figure to stakeholders because it indicates the health and potential growth of a company. Non-operating revenue is generated from outside the main operations of a business. These activities are often incidental or peripheral to the primary business operations. They are derived from other sources, such as interest on investments, gains from foreign exchange, write-down of assets, and gains on the sale of assets. For instance, a company may earn interest from its cash holdings or rent from leasing out its spare office space. Non-operating revenue can also come from one-time events, such as the sale of assets or litigation settlements. The sources for non-operating revenue are often unpredictable and nonrecurring. As such, they should not be relied on to generate sustained income for a business. Let us consider a real-world example of revenue from Tesla, Inc during Q2 2022. Tesla had $16,861,000 revenue from its sales, regulatory credits, and leasing while $1,279,000 from its services. Altogether, the company has generated $18,140,000 from their automotive and services segments. Two types of revenue need to be recognized in the financial statements: accrued and deferred revenue. Accrued revenue is the type of revenue that has been earned but not yet received. This means that the product or service has been provided but the customer has not yet paid for it. Accountants often label this revenue as accounts receivable on a financial statement before the cash payment is received. An example of accrued revenue would be if a company provided a service to a customer on credit. The company would have earned the revenue from providing the service, but would not have received payment yet. The revenue would still be recorded because the company had completed its obligations. Since no payment has been received yet, the company would record it as accounts receivable rather than cash. Deferred revenue is when a company receives cash payments upfront for products or services sold but has not yet provided the customer with what they paid for. Since deferred revenue will not be considered a revenue until it is earned, it has to be recorded in the balance sheet as a liability until the company renders the product or service. An example of deferred revenue would be if a customer buys gym membership for 12 months and pays upfront for all 12 months. The company would not recognize the full amount of revenue until the customer has used the program for 12 months. Revenue accounting is simple when a product is sold and the revenue is immediately recognized upon customer payment. Revenue can become complicated to account for, though, when a company's production process takes an extended period of time. The revenue recognition principle refers to the accounting principle that requires revenue to be recognized when it is earned, not necessarily when cash is received. Let us take, for example, these two scenarios. Scenario 1: A customer orders furniture from a shop and pays $500 in advance on May 1. The customer received the furniture on June 1. Based on the revenue recognition principle, the shop recognized its revenue not in May but in June. It is because the revenue is recognized when it is earned or when the furniture is delivered to the customer. This type of revenue is what we refer to as deferred revenue because the payment is given beforehand for goods to be delivered in the future. The company will record the $500 as a liability on the balance sheet until the furniture is delivered and the revenue is recognized. Scenario 2: A customer gets his bike repaired on July 1. The customer paid $50 for the service the following month, on August 1. Based on the revenue recognition principle, the revenue is recognized on July 1 because that is when the service was provided - when the bike repair took place. This type of revenue is what we call the accrued revenue because the service was provided in advance of the payment. The company will record the $50 as an asset, that is accounts receivable, on the balance sheet until it is received from the customer in August. It is important to note that accrued and deferred revenue does not exist under the cash basis accounting. It is because, under the cash basis accounting, revenue is only recognized once cash changes hands. Accrued and deferred revenues only exist in the accrual basis accounting. The Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) jointly issued the Accounting Standards Codification (ASC) 606 on May 28, 2014. It aims to establish guidelines around contracts and provide some standardization on the whole revenue recognition process by modifying different industry and transaction-specific guidelines with a five-step framework that is more transparent and industry-neutral. The following is the five-step framework of revenue recognition: Revenue and income are often confused because they are both financial terms that refer to money coming into a company. Revenue is the total amount of money produced from the sale of goods or services before expenses are deducted. Income, also known as profit, is the net amount of revenue after all expenses have been deducted. Types of revenue include sales revenue, service revenue, interest revenue, and rental revenue. Income can be either: Typically, income refers to net income or the bottom line. Revenue, on the other hand, is the top line. Here is a consolidated statement of income of Coca-Cola for 2021. Coca-Cola reported a top-line revenue figure of $38,655,000 for 2021 and $10,042,000 in net income for the same period. The net income of Coca-Cola is lesser than its total revenue because the company also has expenses that are incurred to bring about that revenue. These expenses include the cost of goods sold, operating expenses, interest expenses, and taxes. There were also other sources of revenue that were added to the operating revenue such as interest income, net gains on derivatives, and net change in pension and other postretirement benefit liabilities. Income and revenue may increase when a company sells more products or services, but it is important to remember that a company still has to make a profit (or net income) in order for the business to be successful in the long run. Both income and revenue could grow in various ways, including price increases of goods or services, increased sales volume, or improved efficiencies in production, leading to lower costs. Revenue is the amount of money a company receives from its primary business activities, such as sales of products and services. It is often used to measure a company's financial performance and is considered the "top line" because it sits at the very top of the income statement. There are different types of revenue, such as operating revenue and non-operating revenue. Revenue is also different from income, which is the amount of money that a company has left after expenses have been deducted. Revenue is recognized when it is earned, not when cash is received, according to the Revenue Recognition Principle and the Accounting Standards Codification (ASC) 6066. Revenue is an important metric to watch for any business as it is a good indicator of the company's financial health and performance. By understanding the different types of revenue and how to calculate them, businesses can make informed decisions about their operations and finances.What Is Revenue?

Formula and Sample Calculation of Revenue

Types of Revenue

Operating Revenue

Non-Operating Revenue

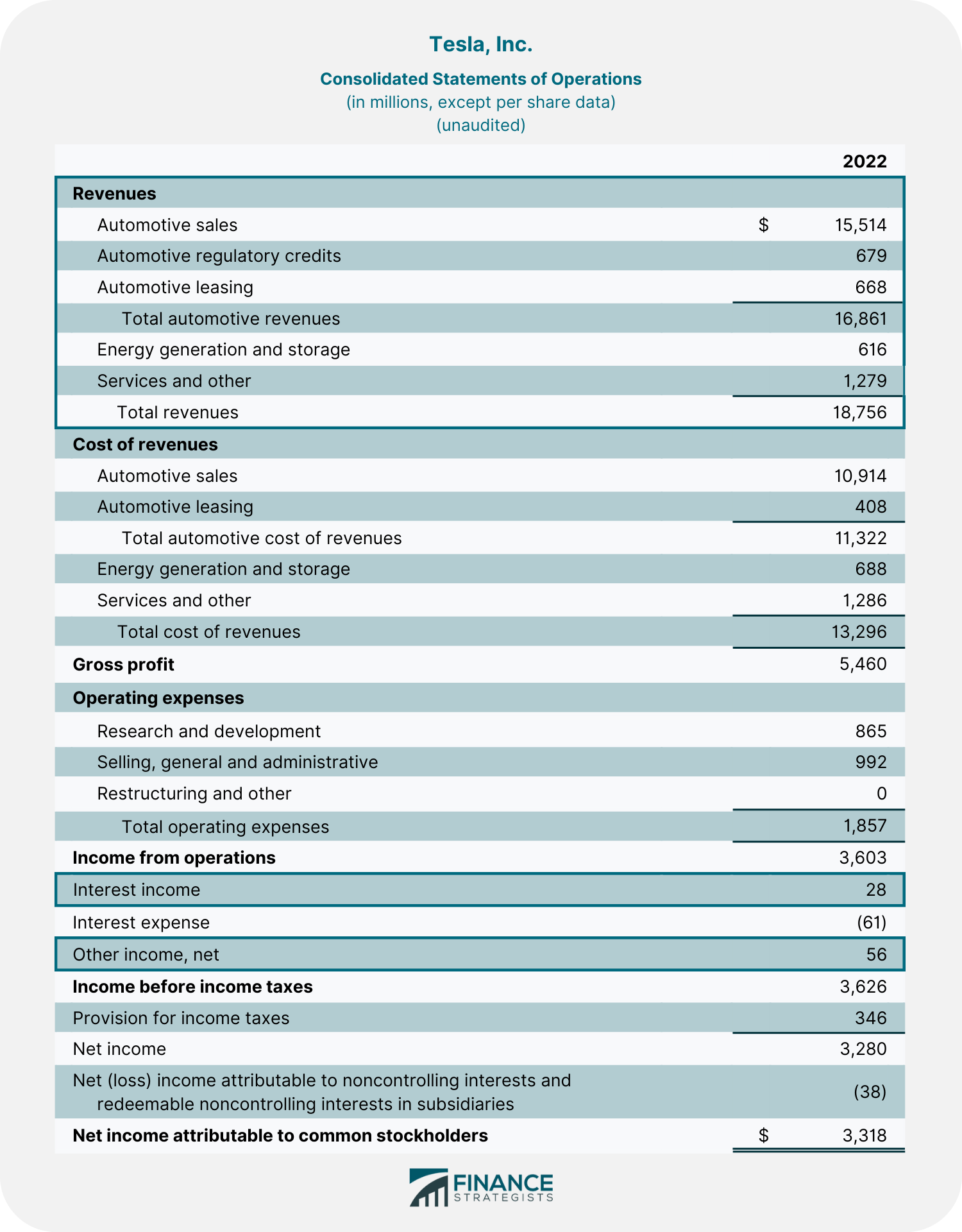

Example of Revenue

Its energy generation and storage segments also produced $616,000.

Lumping all sources of revenue from its main operations, Tesla earned a total operating revenue of $18,756,000.

Additionally, Tesla also earned an interest income of $28,000 and other income of $56,000. As these revenue sources are not from Tesla’s main operations, the total of $84,000 is considered as non-operating revenueAccrued and Deferred Revenue

Accrued Revenue

Deferred Revenue

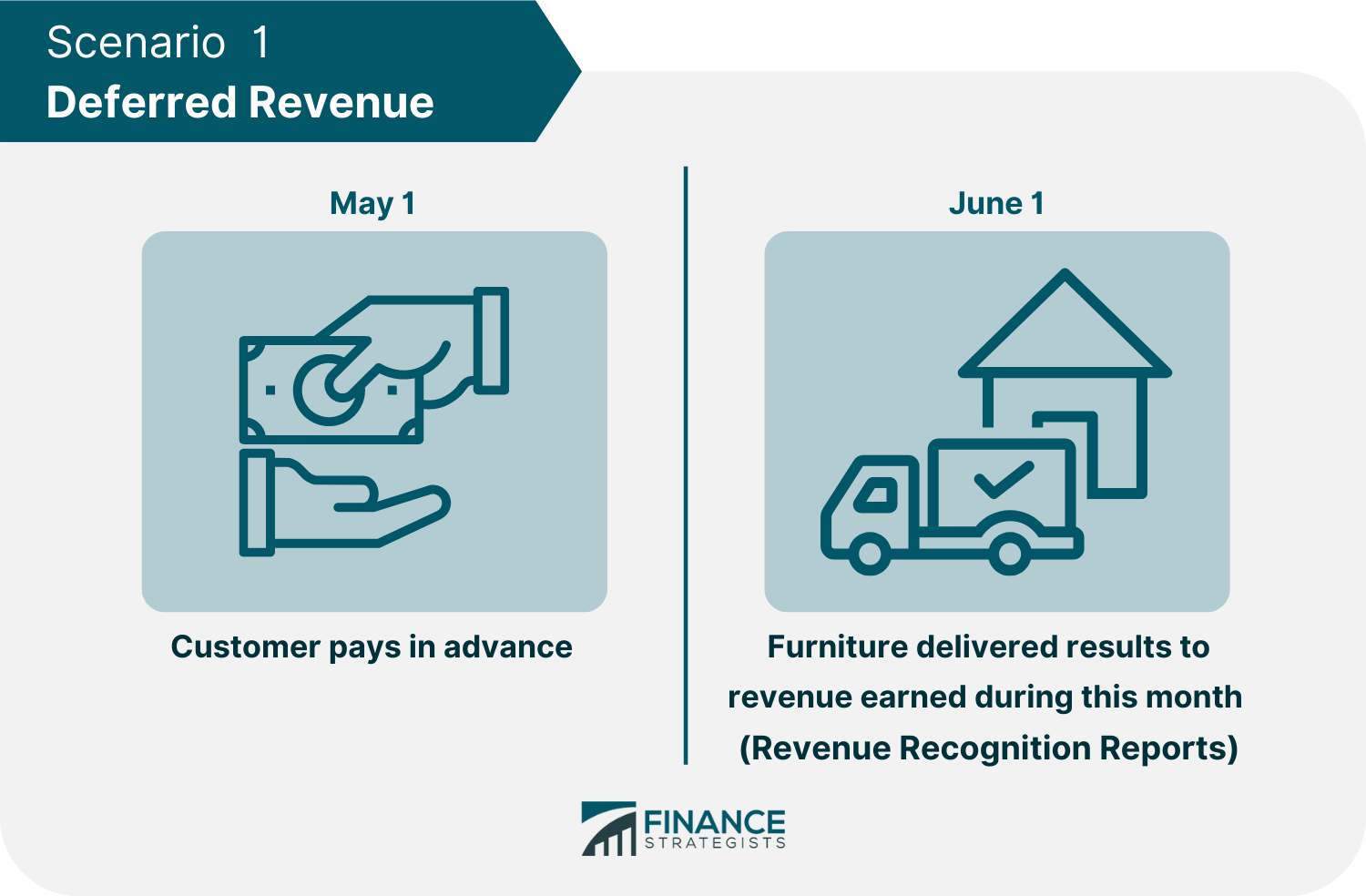

Revenue Recognition Principle

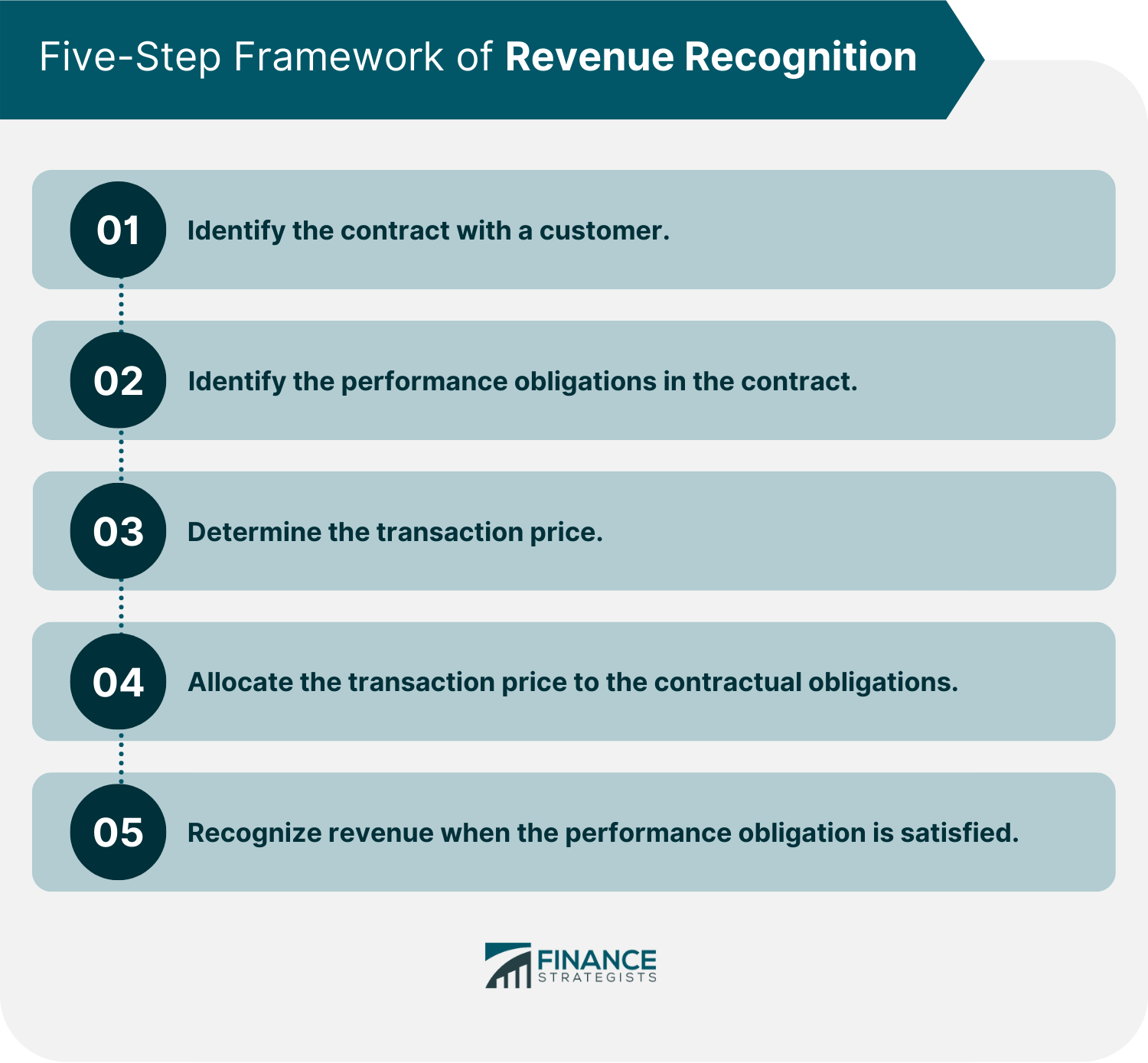

Accounting Standards Codification (ASC) 606

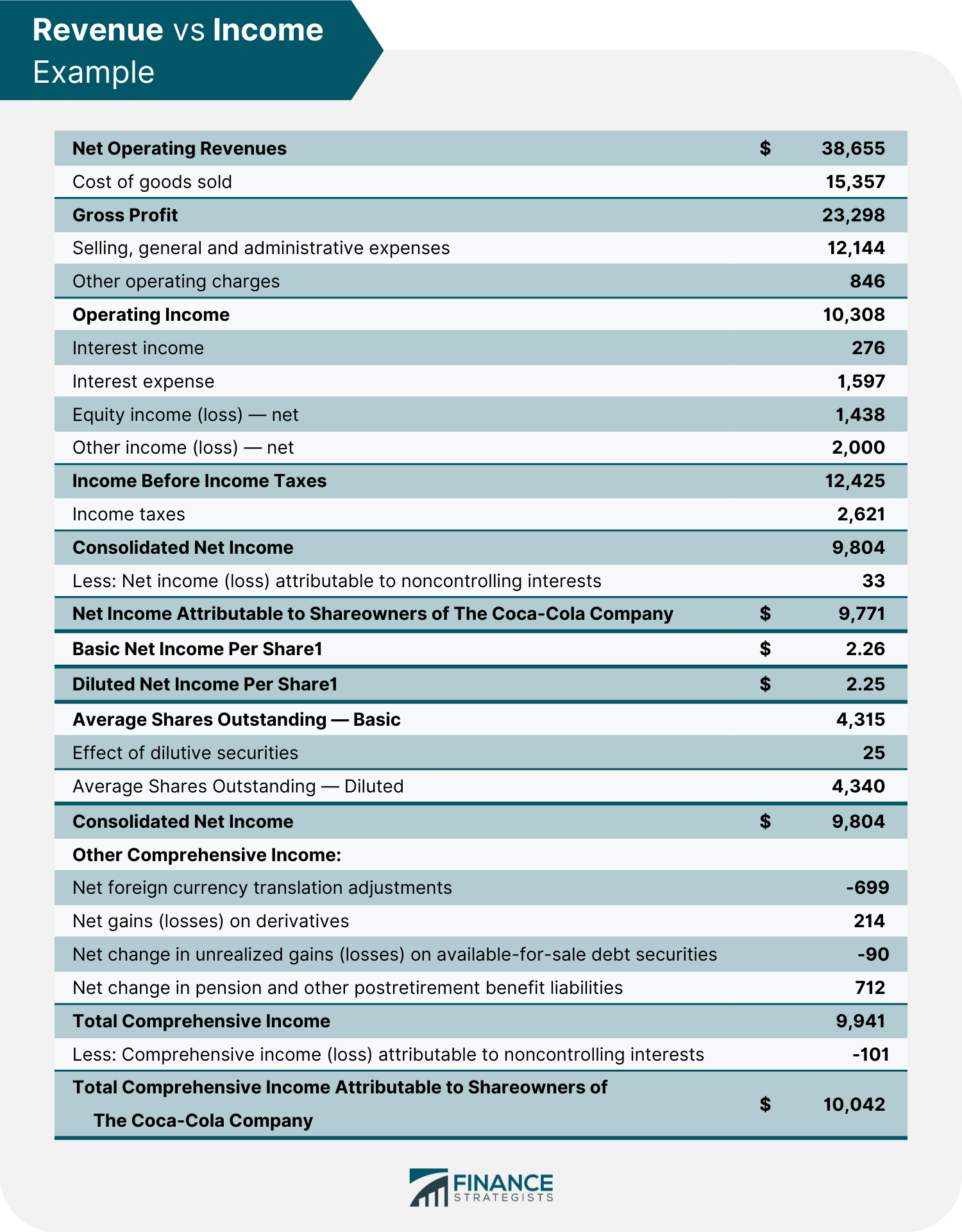

Revenue vs Income

Final Thoughts

Revenue FAQs

Revenue is the total money that a business earns from its normal business activities. It is often referred to as gross sales.

Revenue is the total money that a business earns from its normal business activities. Income is the money that a business has left after all expenses have been paid.

Revenue can be calculated by multiplying the price of goods or services sold by the number of units sold.

Revenue is the total money that a business earns from its normal business activities. Cash flow is the money that is coming in and out of a business.

Depending on the company, revenue and sales can be the same. Revenue is the total income generated by the company from its core business operations prior to subtracting any expenses from the calculation. Sales are the proceeds generated by the company from selling goods or providing services to its customers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.