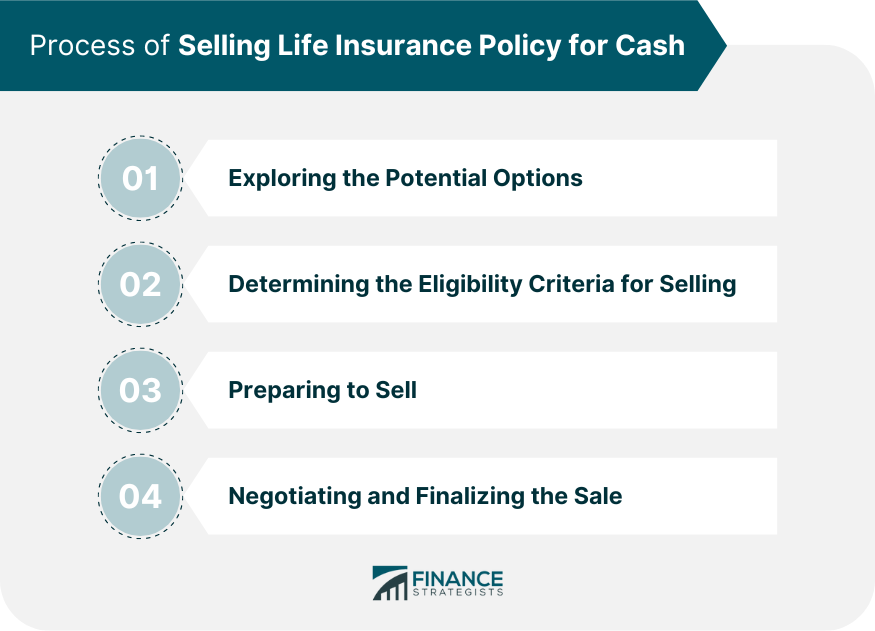

A life insurance policy is a contract between an individual and an insurance company, where the individual pays regular premiums in exchange for a death benefit to be paid out to their beneficiaries upon their passing. While life insurance policies are typically held until the insured person's death, there are situations where selling the policy for cash becomes an attractive option. Selling a life insurance policy involves transferring ownership and beneficiary rights to a buyer or provider in exchange for an immediate cash payment. The buyer assumes responsibility for future premium payments and receives the death benefit when the insured person passes away. The process of selling life insurance policy for cash involves (1) exploring the potential options, (2) determining the eligibility criteria for selling, (3) preparing the documents, policy valuation and tax implications, and (4) negotiating and finalizing the sale. Surrendering a life insurance policy involves terminating the contract and receiving the policy's cash surrender value from the insurance company. The process typically requires submitting a formal request to the insurer. Considerations when choosing this option include potential tax consequences, loss of future death benefits, and the possibility of the surrender value being less than the potential value in the secondary market. Immediate Access to Cash: Surrendering the policy provides policyholders with an immediate lump sum payment. No Further Premium Payments: Policyholders are relieved of future premium obligations once the policy is surrendered. Loss of Coverage: Surrendering the policy means giving up the death benefit that would have been paid to beneficiaries. Potential Tax Consequences: Surrendering a policy may result in taxable income if the cash surrender value exceeds the premiums paid. Surrender Value May Be Lower: The cash surrender value might be less than the potential value in the secondary market, reducing the overall financial benefit. Life settlement providers act as intermediaries between policyholders and institutional investors. They evaluate the policy's value and connect sellers with potential buyers. The process typically involves obtaining offers based on the policy's value and the insured person's life expectancy. Viatical settlements are specific types of life settlements designed for individuals with a terminal illness or chronic condition. In a viatical settlement, the policyholder sells their life insurance policy to a buyer, typically at a percentage of the death benefit. The policyholder receives a lump sum payment, which can be used to cover medical expenses or improve their quality of life. Potentially Higher Payout: Selling a policy in the secondary market can often yield a higher payout compared to surrendering the policy. Access to Immediate Cash: Policyholders receive a lump sum payment, providing financial flexibility. Commissions and Fees: Selling in the secondary market may involve paying fees and commissions to brokers or settlement providers. Loss of Ownership and Control: Once the policy is sold, the policyholder no longer has ownership or control over the policy. Some life insurance policies offer accelerated death benefits, which allow policyholders to access a portion of the death benefit while still alive if they have a qualifying terminal illness or need long-term care. The accelerated death benefit can be used to cover medical expenses and long-term care costs. Access to Funds for Long-Term Care: Converting the policy into a long-term care benefit provides a source of funding to cover healthcare expenses. Retaining Some Death Benefit: Policyholders may retain a reduced death benefit to provide financial protection for their beneficiaries. Reduction in the Overall Death Benefit: Converting the policy may result in a reduced death benefit for beneficiaries. Policy Modifications and Restrictions: Converting the policy may involve making changes to the policy terms and could limit flexibility in the future While some buyers have no minimum age requirement, others may set a minimum age, typically around 65 years old. Additionally, certain providers may have maximum age limits, after which it becomes more challenging to sell a policy. Generally, policies that are eligible for sale include term life insurance, whole life insurance, and universal life insurance policies. The coverage amount and the number of years remaining on the policy can also influence its marketability. The cash surrender value of a life insurance policy is the amount the insurance company will pay if the policy is voluntarily terminated. This value depends on factors such as the policy's duration, premiums paid, and any accrued cash value or dividends. Potential buyers or providers may evaluate the insured person's current health condition, medical history, and life expectancy to determine the policy's value. Policies with insured individuals in good health are generally more desirable in the secondary market. Some life insurance policies, such as whole life and universal life insurance, may have investment components. These policies accumulate cash value over time, which can enhance their marketability. Assessing the policy's investment potential involves understanding the policy's growth potential, interest rates, and any surrender charges or penalties. This involves gathering necessary documentation, valuing the policy accurately, and assessing potential tax implications. By following these steps, policyholders can ensure a smooth and informed process when selling their life insurance policy for cash. Collect all relevant policy documents, including the original policy contract, any amendments or riders, and any correspondence with the insurance company. These documents provide important details about the policy, such as coverage amount, policy type, and any additional benefits or features. Obtain comprehensive medical records that outline the insured person's health history. This includes recent medical exams, diagnoses, treatments, and medications. Compile a record of premium payments made throughout the life of the policy. This includes receipts or bank statements showing proof of premium payments. Engage the services of a reputable life settlement broker who specializes in facilitating the sale of life insurance policies. A broker can evaluate the policy's characteristics, assess its market value, and provide guidance throughout the selling process. Seek multiple appraisals from different life settlement providers or brokers to ensure an accurate valuation of the policy. This allows policyholders to compare offers and determine the best possible sale price. Appraisals take into account factors such as the insured person's age, health status, policy type, coverage amount, and the policy's remaining duration. Selling a life insurance policy can have tax implications, and it is essential to understand these potential consequences. The cash proceeds received from the sale may be subject to income tax if the amount exceeds the policy's tax basis (the total premiums paid). Additionally, any gain from the sale may be subject to capital gains tax. Policyholders should familiarize themselves with the tax laws in their jurisdiction and consult with a tax professional for personalized advice. It is highly recommended to consult with a tax professional who specializes in life insurance and financial transactions. They can provide guidance on the specific tax implications of selling a life insurance policy, considering factors such as the policyholder's tax bracket, state regulations, and any available exemptions or deductions. It is crucial to evaluate the reputation and experience of potential buyers or providers before entering into any negotiations. Research the track record of the buyer or provider, including their financial stability and customer reviews. Look for established companies with a history of successful transactions and satisfied clients. Obtain offers from multiple buyers or providers to compare the terms and conditions they offer. Consider factors such as the purchase price, any fees or commissions involved, and the provider's reputation for timely payments. Thoroughly review the terms of each offer to ensure they align with the policyholder's financial goals and requirements. Understand the steps involved, including the review of policy documents, the assessment of the insured person's health status, and the valuation of the policy. Clarify any questions or concerns with the buyer or provider to ensure a transparent and efficient negotiation process. Be prepared to engage in negotiations with the buyer or provider. Consider counteroffers and modifications to the initial offer if they align better with your expectations. Negotiations may involve discussing the purchase price, payment terms, or any additional provisions or requirements. This typically involves signing a purchase agreement or contract provided by the buyer or provider. Carefully review the document and ensure that all terms and conditions are accurately reflected. Work closely with the buyer or provider to facilitate the transfer of ownership and beneficiary information. The buyer or provider will guide you through the required steps to transfer the policy and update beneficiary designations. The payment may be provided as a lump sum or in installments, depending on the negotiated terms. Verify the receipt of the payment and confirm that it aligns with the agreed-upon amount. Selling a life insurance policy for cash is an option for those needing immediate funds or finding their current coverage unnecessary or burdensome. This process necessitates examining possibilities including policy surrender, sale in the secondary market, or conversion into a long-term care benefit. A thorough understanding of the pros and cons of these options leads to informed decision-making. Eligibility criteria such as age, policy type, cash surrender value, insured's health status, and the policy's investment potential should be assessed. The selling preparation includes compiling key documentation, accurate policy valuation, and comprehending potential tax implications, key steps for a seamless sale process. The transaction concludes with the selection of a reliable buyer or provider, offer comparison, effective negotiation, and transaction completion. This process requires careful planning and execution, allowing policyholders to harness their life insurance policy as a significant financial resource.Overview of Selling a Life Insurance Policy for Cash

Exploring Potential Options for Selling a Life Insurance Policy

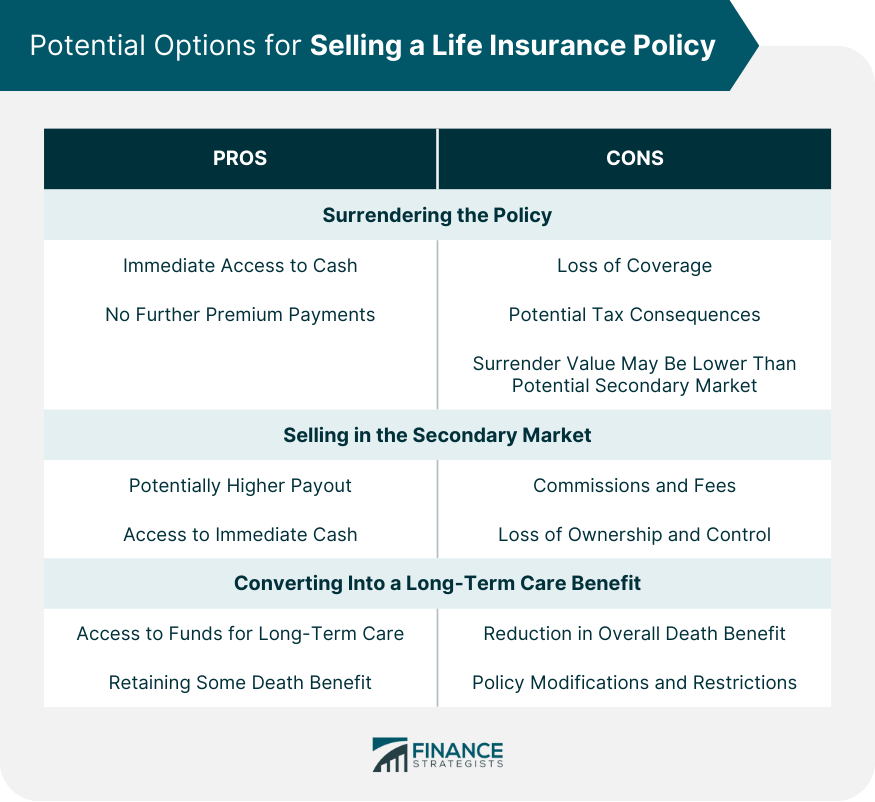

Option 1: Surrendering the Policy to the Insurance Company

Pros of Surrendering the Policy to the Insurance Company

Cons of Surrendering the Policy to the Insurance Company

Option 2: Selling the Policy in the Secondary Market

Working With Life Settlement Providers

Understanding Viatical Settlements

Pros of Selling in the Secondary Market

Cons of Selling in the Secondary Market

Option 3: Converting the Policy Into a Long-Term Care Benefit

Pros of Converting the Policy

Cons of Converting the Policy

Determining Eligibility for Selling a Life Insurance Policy

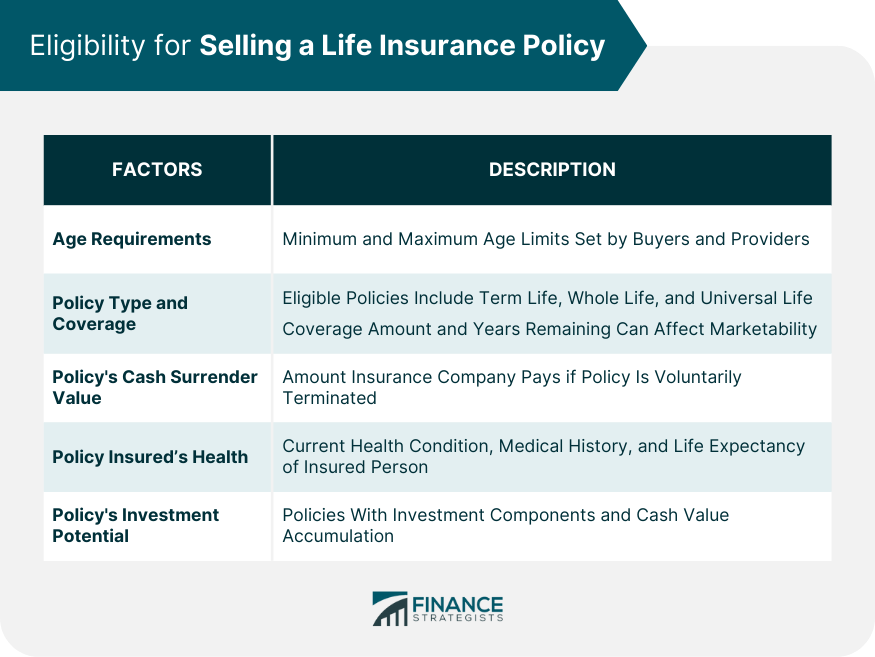

Age Requirements

Policy Type and Coverage

Policy's Cash Surrender Value

Policy Insured’s Current Health Status

Policy's Investment Potential

Preparing to Sell Your Life Insurance Policy

Gathering Necessary Documentation

Policy Documents

Medical Records

Premium Payment History

Valuing the Policy

Consulting With a Life Settlement Broker

Getting Multiple Appraisals

Assessing Tax Implications

Understanding Potential Tax Consequences

Consulting With a Tax Professional

Negotiating and Finalizing the Sale

Choosing a Buyer or Provider

Comparing Offers and Terms

Negotiating the Sale

Finalizing the Sale

Completing Required Paperwork

Transferring Ownership and Beneficiary Information

Receiving the Cash Payment

Conclusion

How to Sell Your Life Insurance Policy for Cash FAQs

To sell your life insurance policy for cash, you can explore options such as surrendering the policy to the insurance company or selling it in the secondary market through a life settlement provider.

The process typically involves researching life settlement providers, gathering necessary documentation, requesting policy appraisals and offers, evaluating offers, negotiating terms, seeking professional advice, completing required paperwork, and coordinating with the buyer and insurance company.

Not all policies may qualify for sale. Eligibility criteria vary, but generally, policies with a face value of $100,000 or more and insured individuals aged 65 or older or with certain health conditions have a higher likelihood of qualifying.

Selling a life insurance policy can provide immediate access to funds, potentially higher payouts compared to surrendering the policy, and relief from premium payments. It can be especially beneficial if you no longer need the coverage or struggle with premium affordability.

Yes, there can be tax consequences. The amount received from the sale may be subject to income tax, and the tax implications vary based on factors such as the policy's cash value, premiums paid, and the type of transaction. It is advisable to consult with a tax professional for guidance specific to your situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.