A life insurance policy is fundamentally a contract between an individual, often referred to as the policyholder, and an insurance company. This contractual agreement requires the policyholder to make regular payments, known as premiums. In return, the insurance company must pay the nominated beneficiaries a predetermined sum of money, commonly called a death benefit, upon the policyholder's death. The principal purpose of life insurance is to provide a financial cushion for the insured person's beneficiaries after their passing. This policy can be designed to cover various expenses such as funeral costs, mortgage payments, and debts and even provide a continued source of income. It can ensure the insured person's children have sufficient funds for their education. In essence, life insurance serves as a financial safeguard for beneficiaries. Yes, it is possible to cancel a life insurance policy. However, the procedure and repercussions of canceling a policy may depend on its specific type and the timing of the cancellation. A policyholder can cancel their life insurance policy at their discretion. The decision to cancel may be triggered by several reasons, such as a change in the policyholder's financial situation, a requirement for a different kind of life insurance, or the desire to secure a more affordable premium from a different provider. Before you proceed with the cancellation process, it's essential to clearly understand your reasons for wanting to cancel. Perhaps you've found a policy that offers better coverage at a lower premium, or your financial circumstances have changed, making the premiums unaffordable. For instance, you may no longer need life insurance if your dependents are now financially independent. Identifying and understanding your motivations will guide your next steps and highlight alternatives to outright cancellation. Life insurance policies differ widely, and so do their cancellation terms. With some policies, especially term life insurance, the cancellation process is relatively straightforward - you can typically stop paying the premiums, and the policy will lapse. However, with permanent life insurance policies like whole or universal life, you may need to complete a policy surrender form. You could incur surrender charges if you're in the policy's early years. Reviewing and understanding your policy's cancellation terms is a crucial part of the process. Canceling a life insurance policy can have significant implications. If your policy has a cash value, like a whole life policy, you might lose this value upon cancellation, especially if you're still within the surrender period. If you cancel a term life policy, you won't get any money back as these policies have no cash value. Another key consequence to consider is the loss of coverage. Once you cancel your policy, the insurance company is no longer obligated to pay out any death benefits. Canceling your policy means your beneficiaries may lose the financial protection the policy was meant to provide. Once you've carefully considered your reasons for cancellation, understood the terms, and evaluated the consequences, you can proceed with the cancellation. You can start this process for many policies by contacting your insurance company or broker. They can guide you through the procedure and the necessary paperwork. If you have a term life policy, cancellation could be as simple as stopping your premium payments. For whole or universal life policies, you may need to complete a surrender form or write a formal cancellation letter. After canceling your policy, you might need to implement other plans. If you still need life insurance coverage, you should secure a new policy before canceling your current one to avoid a coverage gap. Remember, as you age or if your health deteriorates, life insurance can become more expensive and harder to qualify for. You should review your budget or financial plan if you've canceled due to unaffordable premiums. Keep any paperwork related to your cancellation; it could be useful for future insurance dealings or your personal records. Term life insurance is characterized by a set coverage period, usually between 10 and 30 years. If you decide to cancel this type of policy, the process is often straightforward. You can typically stop making premium payments, which will result in your policy lapsing and subsequently getting canceled. Unlike permanent policies, term life insurance doesn't accrue cash value over time, so there's no surrender fee or cash value to retrieve when you cancel. However, once you stop paying premiums, your coverage will end, and you won't receive any money back from the premiums you've already paid. Whole life insurance, a type of permanent life insurance, provides lifetime coverage and also has a cash value component that grows over time. Canceling a whole life insurance policy often involves more than just stopping premium payments. To cancel, you must usually fill out a policy surrender form provided by your insurer. If you're canceling the policy in its early years, you might have to pay surrender charges. These charges are often a percentage of your policy's cash value and decrease the longer you hold the policy. You might also face tax implications if the cash value exceeds the total amount of premiums you've paid. Universal life insurance is another type of permanent life insurance that builds cash value and provides lifelong coverage. The cancellation process for universal life insurance is similar to whole life insurance. You may need to complete a surrender form, and if you're within the surrender period, you may face surrender charges. The policy's cash value can be subject to taxation upon surrender, especially if it exceeds the total amount of premiums you've paid into the policy. Always consider consulting with a financial advisor or tax professional to understand these implications fully. Canceling a life insurance policy prematurely can lead to significant repercussions, such as leaving you unprotected and possibly causing a financial loss. This risk is especially high if you have a whole life or universal life policy. Life insurance policies sometimes come with the feature of conversion. This allows the policyholder to switch from one type of policy to another - usually from term to permanent coverage. The advantage of conversion is that it does not require any new underwriting, thereby preserving insurability. With conversion, you can maintain your life insurance coverage but adjust the terms to make them more suitable or affordable for your current circumstances. In certain circumstances, selling your life insurance policy, known as a life settlement, can be an alternative to cancellation. This arrangement allows you to sell your policy to a third-party investor for a lump sum. The amount you receive is generally more than the policy's cash surrender value but less than its death benefit. Life settlements can be complex transactions and may have tax implications, so it's advisable to seek professional advice before proceeding with such a decision. Reducing the death benefit, or the sum of money that your beneficiaries receive upon your death, can be another alternative to canceling a policy. If your premium payments have become too burdensome, reducing the death benefit could result in lower premiums. However, this also means that your beneficiaries would receive less money. This alternative is worth considering if you want to maintain insurance coverage while making your premium payments more manageable. If you have a permanent life insurance policy such as whole or universal life, your policy may have a cash value component. In such cases, an alternative to cancellation could be borrowing against this cash value. This loan can provide immediate funds while preserving your insurance coverage. It's important to understand that the loan accrues interest and will reduce the death benefit if not repaid. This alternative should be considered with a clear understanding of these potential consequences. Canceling a life insurance policy may come with numerous financial implications that you must navigate. If you had a cash value policy, you might receive the cash surrender value upon cancellation, minus any surrender fees, and possibly subject to taxation. It's important to remember that if you had borrowed against the policy, your cash value might be significantly reduced or even depleted. Also, the money spent on premiums for a term life insurance policy will not be recovered. Considering these factors will help you understand your financial position and plan accordingly. When you cancel a life insurance policy, you lose its coverage. If you still need life insurance, you must arrange for new coverage. Remember that your age, health, and lifestyle factors can impact the cost and availability of new life insurance. It's generally a good idea to secure a new policy before canceling the old one to avoid a coverage gap. If your circumstances have changed and you no longer need life insurance, consider maintaining a smaller policy for final expenses or as a financial legacy. Certain legal considerations might also arise when you cancel a life insurance policy. For instance, if you have been mandated by a court order to maintain life insurance, such as part of a divorce settlement, canceling your policy could have legal repercussions. Also, if you are a business owner with a policy as part of a buy-sell agreement, you may need to arrange a replacement policy to maintain the agreement. Consulting with an attorney or legal advisor can help ensure you meet any legal obligations related to your life insurance. Canceling a life insurance policy is possible, but the decision should be made carefully. The cancellation process and implications can vary depending on the type of policy and the time of cancellation. Understanding potential penalties, exploring alternatives to cancellation, and evaluating post-cancellation requirements are all crucial steps. While canceling a policy might seem like the right decision in certain situations, it's not always the best or only solution. Understanding your reasons for cancellation, the financial implications, and the various alternatives can help guide your decision. It's often beneficial to consult with a financial advisor or insurance broker before canceling a life insurance policy. They can provide expert advice based on your personal circumstances and help you understand all the implications of canceling a life insurance policy.What Is a Life Insurance Policy?

Can You Cancel a Life Insurance Policy?

Process of Cancelling a Life Insurance Policy

Understanding the Need for Cancellation

Analyzing the Policy Cancellation Terms

Considering the Potential Consequences

Implementing the Cancellation

Evaluating Post-Cancellation Steps

Different Policy Types and Their Cancellation Processes

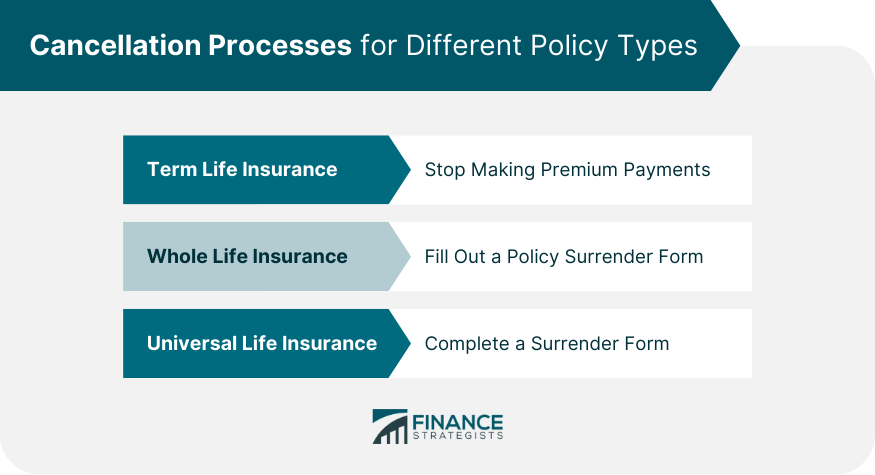

Term Life Insurance

Whole Life Insurance

Universal Life Insurance

Alternatives to Cancelling a Life Insurance Policy

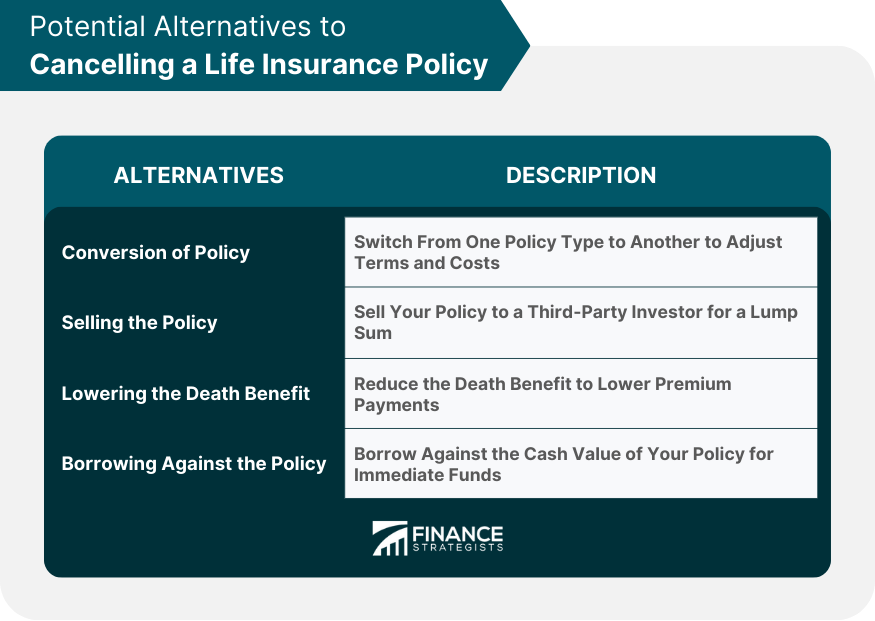

Conversion of Life Insurance Policy

Selling Life Insurance Policy

Lowering the Death Benefit

Borrowing Against Your Policy

Things to Consider After Canceling Life Insurance Policy

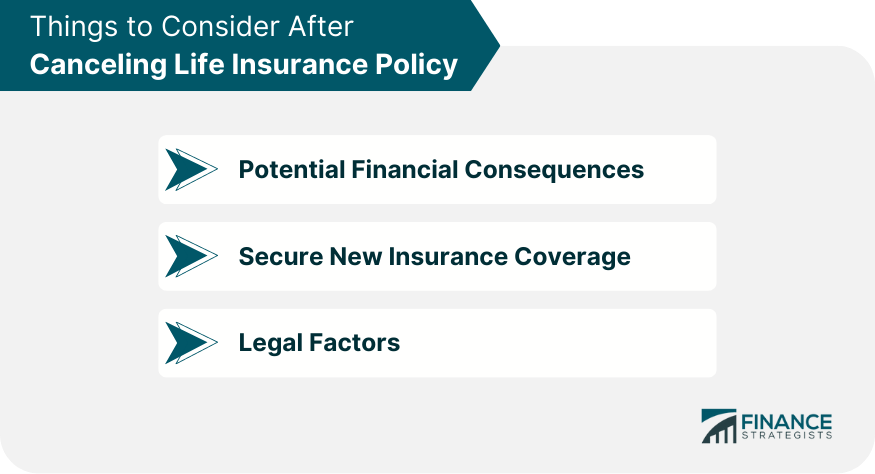

Potential Financial Consequences

Securing New Insurance Coverage

Legal Factors

Final Thoughts

Can You Cancel a Life Insurance Policy? FAQs

Yes, the policyholder can generally cancel a life insurance policy at any time. However, the financial implications and process can vary depending on the type of policy you hold and how long you've held it.

If you have a term life insurance policy, you typically won't get money back after cancellation. If you have a whole or universal life policy, you might receive the cash surrender value, but it could be subject to surrender fees and taxes.

Canceling a policy prematurely can lead to financial loss, especially with whole and universal life policies. You also risk being unprotected, which could have significant implications if you have dependents.

It depends on the type of policy. Term life insurance policies can generally be canceled without penalties, but whole and universal life policies may impose surrender charges, especially if the policy is canceled in the early years.

Before deciding to cancel, consider your reasons for cancellation, explore alternatives, and understand the potential penalties, fees, and financial implications of cancellation. It's also advisable to consult with a financial advisor or insurance broker.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.