A life insurance policy is a contract between an individual and an insurance company that provides financial protection to the policyholder's beneficiaries in the event of their death. It is designed to offer a lump sum payment, known as a death benefit, to the designated beneficiaries upon the policyholder's demise. The purpose of life insurance is to provide a safety net for loved ones, ensuring that they are financially supported and able to maintain their standard of living in the absence of the policyholder. Life insurance policies come in various forms, including term life, whole life, and universal life, each with its own features and benefits. Some life insurance policies, often called permanent or cash-value policies, provide a death benefit and accumulate cash value over time. Policyholders can borrow against this cash value while they're alive, with the loan amount typically depending on the policy's cash value. The policyholder isn't required to repay the loan, but any outstanding loan balance (including interest) is deducted from the death benefit when the policyholder dies. Borrowing from a life insurance policy can provide financial flexibility, as these loans typically don't require credit checks or loan applications. However, there are risks. If the loan isn't repaid, the death benefit will be reduced, potentially leaving beneficiaries with less financial support. If the outstanding loan balance ever exceeds the policy's cash value, the policy could lapse, potentially creating a significant tax liability. Before borrowing from your life insurance policy, evaluating your financial needs and the current situation is crucial. Consider whether the loan is necessary, if other options are available, and how the loan will impact your finances and your beneficiaries' finances in the future. Because of the potential risks and complexities involved, consulting with a financial advisor or an insurance broker is often beneficial before borrowing from a life insurance policy. Policyholders should fully understand their policy details, including the policy's cash value, the loan's interest rate, how the interest is compounded, and the potential consequences of not repaying the loan. Whole life insurance is a type of permanent life insurance that provides a guaranteed death benefit and a cash value component that grows over time. Policyholders can typically borrow against the policy's cash value, with the loan being secured by the death benefit. Universal life insurance is another type of permanent insurance that combines a death benefit with a cash value component, which can earn interest. Policyholders can usually borrow against the cash value, but unlike whole life insurance, universal life insurance offers more flexibility in terms of premiums and death benefits. Other types of cash-value life insurance policies may allow policyholders to borrow against the cash value. These include variable life insurance, indexed universal life insurance, and variable universal life insurance. Each policy has different features and investment options, but they all typically allow for loans against the policy's cash value. To borrow from a life insurance policy, you need to ascertain your policy's cash value. Review your policy documents or contact your insurance company for this information. Generally, your policy's cash value limits how much you can borrow. With your policy's cash value in hand, you're ready to apply for a loan. Contact your insurance company to start this process. They'll provide a form to complete and return; typically, you can do this swiftly without a credit check or loan approval. Upon receiving the loan, you can decide to repay it whenever you want or choose not to repay it at all. Remember that any unpaid loan balance, including interest, will be deducted from the death benefit upon the policyholder's death. If the unpaid loan balance surpasses the policy's cash value, the policy could lapse. Life insurance policy loans often have lower interest rates than traditional personal loans or credit cards, making them an attractive option in certain circumstances. These loans typically do not require a credit check or approval process, making them more accessible for those who may not qualify for traditional lending options. Unlike traditional loans, there are no set repayment terms. Policyholders can choose to repay the loan on their own timeline or not at all, although not repaying can have serious consequences. Suppose the policyholder passes away before the loan is fully repaid. In that case, the outstanding balance (including any accrued interest) is deducted from the death benefit, which could leave beneficiaries with less than expected. If the loan plus interest ever exceeds the policy's cash value, the policy could lapse. If the policy lapses, you lose your life insurance coverage, and the IRS could also consider the cash value as income, potentially leading to a significant tax bill. When you take out a loan, you're reducing your policy's cash value, which in turn can slow the rate at which the cash value accumulates. This could leave you with less cash value to borrow against in the future. Personal loans can be an effective alternative, particularly for individuals with good credit who can secure low-interest rates. Personal loans have a fixed repayment schedule, meaning you must repay the loan within a set timeframe. Personal loans do not require collateral, making them less risky than secured loans. Home equity loans or lines of credit present another viable alternative for homeowners. Based on the equity you've built in your home, these loans generally offer lower interest rates. However, they use your home as collateral. Therefore, there's a risk of foreclosure if payments become unmanageable or aren't made on time, so this option should be considered carefully. Credit cards offer quick access to funds, functioning as short-term loans. While they can be convenient, they usually have high-interest rates, particularly for cash advances. This can lead to a cycle of increasing debt if not managed carefully. Responsible usage and timely repayment are crucial when using credit cards as a loan alternative. Some retirement accounts, such as 401(k)s, allow for loans. However, this option should be cautiously approached as it can potentially jeopardize your long-term retirement savings. These loans may trigger taxes and penalties if not repaid according to the plan rules. Always consult with a financial advisor before borrowing from your retirement account to understand the implications fully. Borrowing from a life insurance policy is an option for permanent or cash-value life insurance policyholders. This option allows the policyholder to take out a loan against the policy's cash value, providing financial flexibility in certain situations. While life insurance loans offer benefits like low-interest rates, no credit checks, and flexible repayment, they also have potential downsides, including a reduction in the death benefit, the possibility of policy lapse, and a negative impact on cash value accumulation. Alternatives such as personal, home equity, credit card, and retirement account loans should also be considered. When managed effectively, borrowing from a life insurance policy can be a viable financial strategy. However, given the potential implications on the policy’s cash value, death benefit, and tax implications if the policy lapses, it's crucial to fully understand the terms and conditions of your policy before borrowing against it. Consulting with a financial advisor or an insurance broker can provide additional insights and personalized advice tailored to your specific situation and financial goals.What Is a Life Insurance Policy?

Borrowing From a Life Insurance Policy

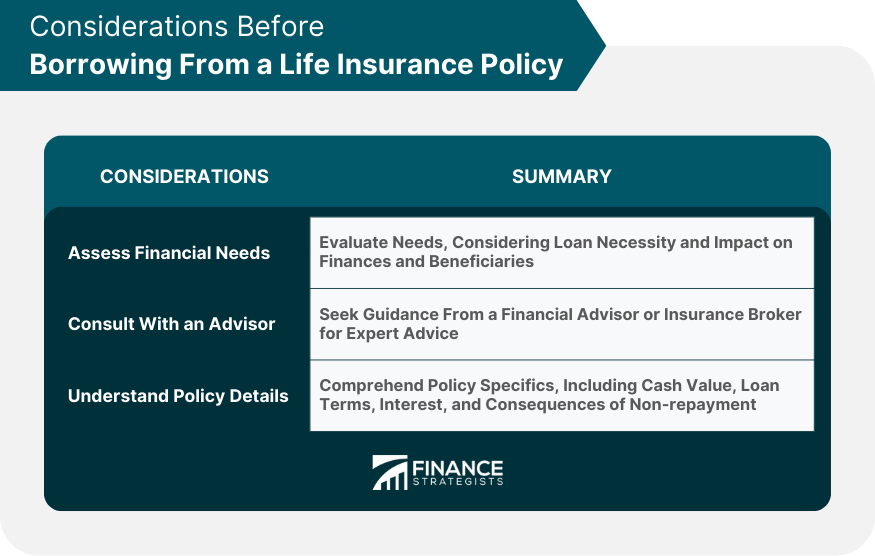

Key Considerations Before Borrowing From a Life Insurance Policy

Assessing Financial Needs and Situation

Consultation With a Financial Advisor

Understanding Policy Details and Loan Terms

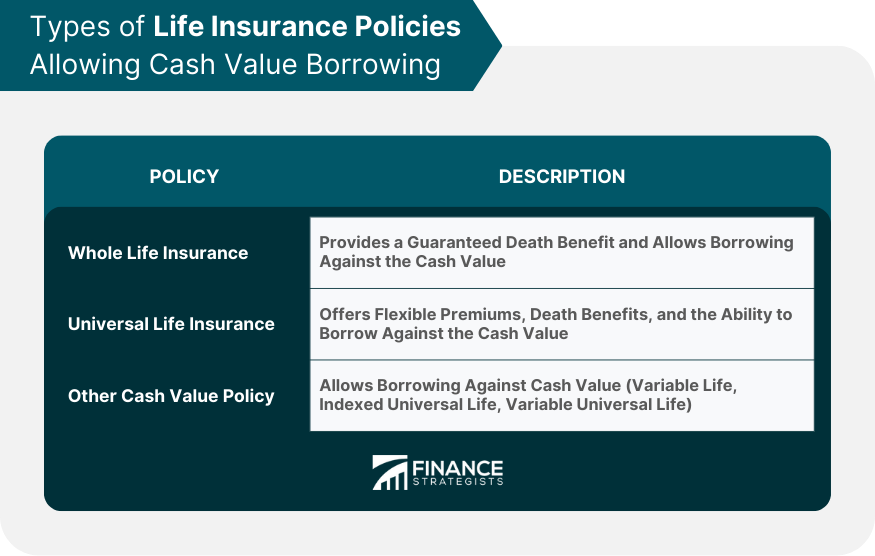

Types of Life Insurance Policies That Allow Borrowing

Whole Life Insurance

Universal Life Insurance

Other Cash-Value Life Insurance Policies

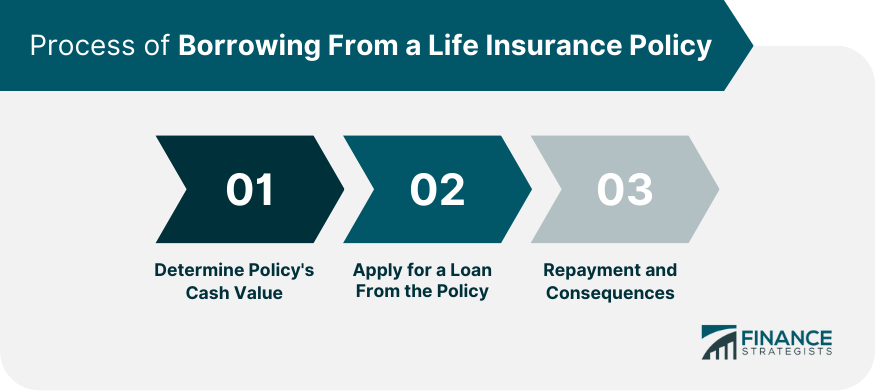

Process of Borrowing From a Life Insurance Policy

Determine Policy's Cash Value

Apply for a Loan From the Policy

Understand Repayment of the Loan and Consequences of Non-repayment

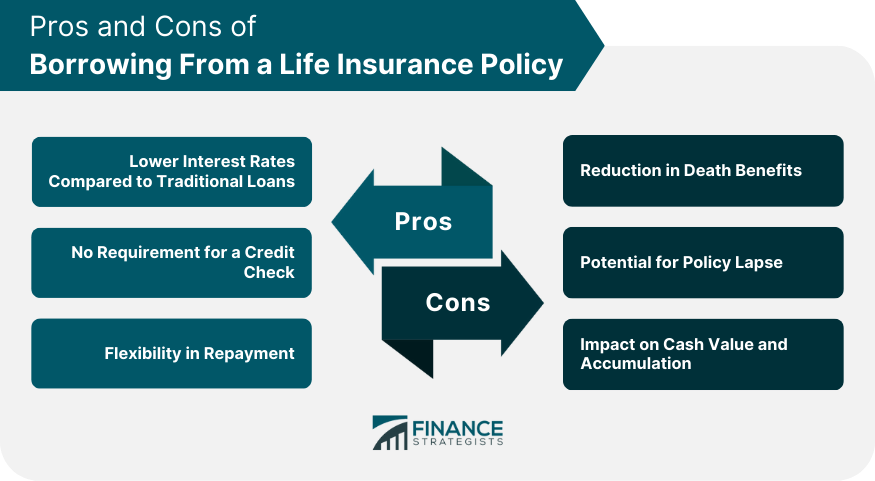

Pros and Cons of Borrowing From a Life Insurance Policy

Pros

Interest Rates Compared to Traditional Loans

No Requirement for a Credit Check

Flexibility in Repayment

Cons

Reduction in Death Benefits

Potential for Policy Lapse

Impact on Cash Value and Accumulation

Alternatives to Borrowing From a Life Insurance Policy

Personal Loans

Home Equity Loans

Credit Card Loans

Retirement Account Loans

Conclusion

Borrowing From a Life Insurance Policy FAQs

Borrowing from a life insurance policy refers to the process of taking out a loan against the cash value of your permanent life insurance policy.

When you borrow from a life insurance policy, the insurer uses your policy's cash value as collateral for the loan. You can typically borrow up to the amount of cash value you have accumulated, and the loan accrues interest.

The borrowed funds from a life insurance policy can be used for various purposes, such as paying for education expenses, covering medical bills, home renovations, or any other financial needs you may have.

Yes, there are risks involved in borrowing from a life insurance policy. If you cannot repay the loan with interest, it could reduce your policy's death benefit and cash value. Additionally, if the loan remains unpaid at the time of your death, the outstanding balance may be deducted from the death benefit paid to your beneficiaries.

The repayment process for a loan taken from a life insurance policy varies depending on the policy and insurer. Generally, you can repay the loan in regular installments or choose to pay it off in a lump sum. Making timely repayments is important to avoid potential negative consequences on your policy's cash value and death benefit.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.